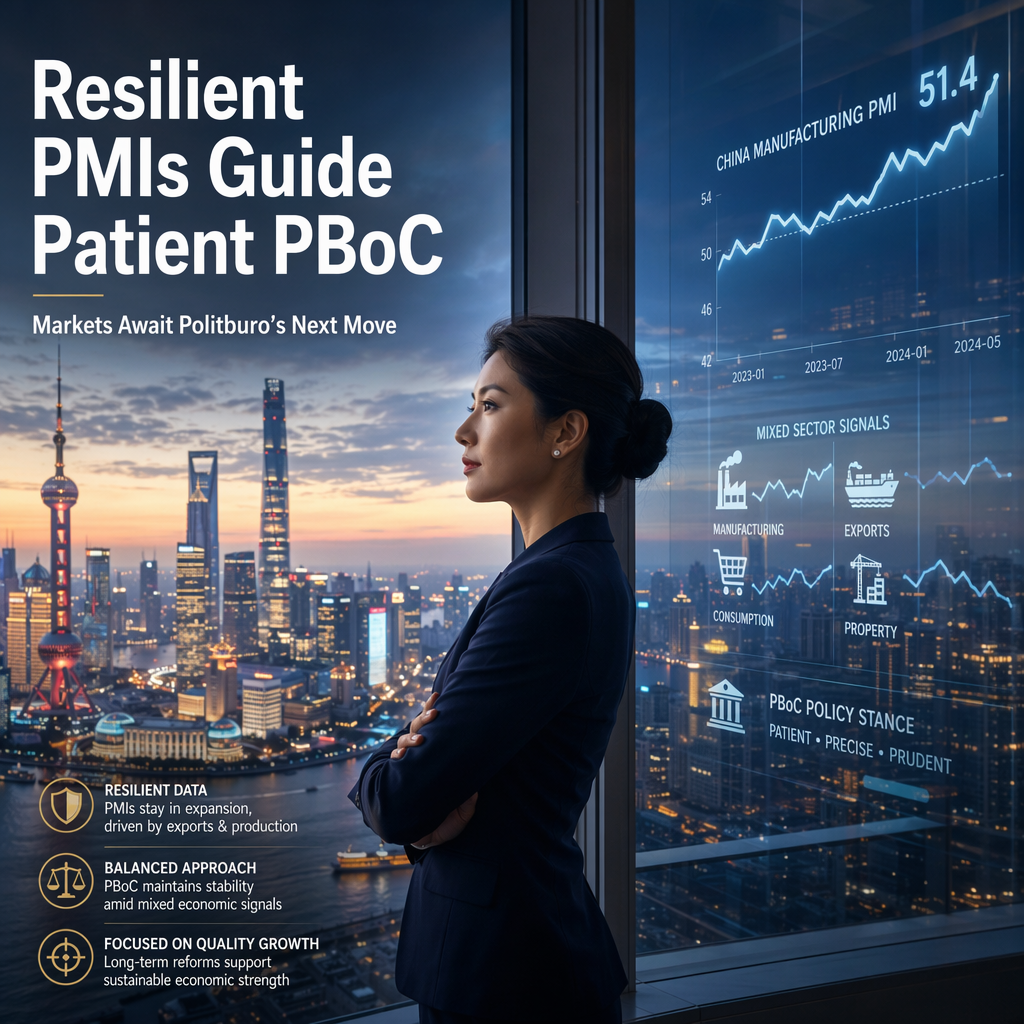

Commerzbank’s Dr. Henry Hao, as cited by FXStreet, highlights that China’s official PMI readings for June 2026 indicate a nuanced economic landscape, with manufacturing and non-manufacturing sectors showing resilience despite ongoing softness in domestic demand indicators such as retail sales and fixed-asset investment [1]. The manufacturing sector, in particular, has been buoyed by a surge in high-tech exports, pushing it further into expansion territory and supporting headline growth [1].

This external strength, however, contrasts with a cooling domestic market, creating a 'two-speed' dynamic that complicates the near-term policy outlook for Chinese authorities [1]. Policymakers are expected to maintain a patient and targeted approach to stimulus, refraining from immediate broad-based easing measures as long as export-led growth remains robust [1]. The current data send mixed signals: while the economy is not weak enough to justify aggressive easing, persistent underlying demand weakness remains a concern [1].

The July Politburo meeting is identified as a critical upcoming event that could provide clearer guidance on whether Beijing will intensify fiscal or monetary support in the second half of the year [1]. Until then, authorities are likely to delay stronger policy actions, opting instead for a cautious and data-dependent approach [1].

CONCLUSION

China’s latest PMI data suggest that policymakers will maintain a patient and targeted policy stance, holding off on broad-based easing for now. The July Politburo meeting is expected to be a key event for future policy direction, with markets watching for signals on potential fiscal or monetary support.