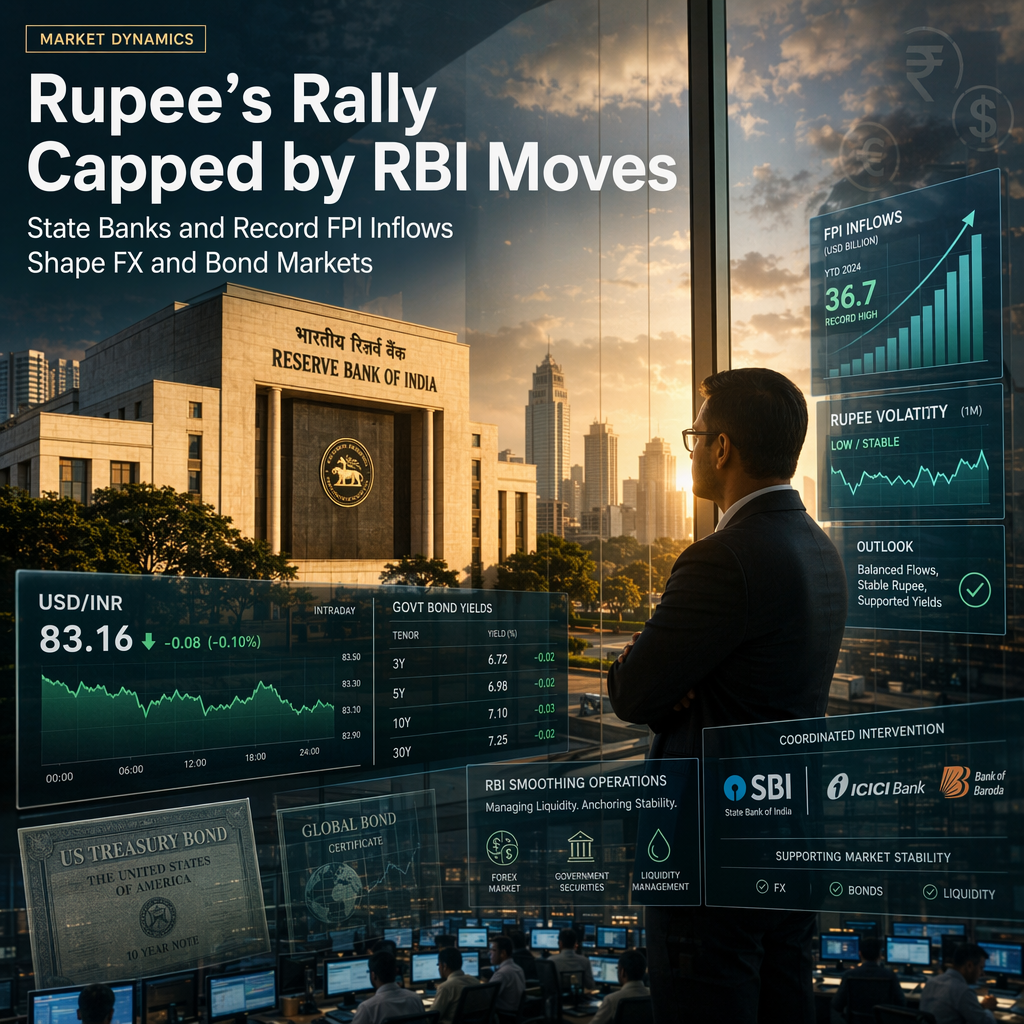

Societe Generale strategists report that the USD/INR currency pair began the third quarter quietly, with the pair marginally bid at 94.70 but remaining capped below its 50-day moving average near 95.02 since mid-June [1]. This restrained price action is attributed to reported US Dollar selling by Indian state banks and expectations of Reserve Bank of India (RBI) smoothing operations, which are seen as containing any significant upside in the pair [1].

In the Indian bond market, the RBI's decision to include ultra-long 40-year and 50-year bonds in the Fully Accessible Route (FAR) segment has significantly increased their attractiveness. As a result, the 40-year bond yield dropped by 32 basis points to 7.38%, and the 50-year bond yield fell by 27 basis points to 7.45% in June [1]. Foreign Portfolio Investors (FPIs) responded strongly, purchasing a record INR418 billion ($4.4 billion) of Indian Government Bonds (IGBs) via the FAR route in June, nearly double the previous monthly record of INR239 billion set in August 2024. This surge is attributed to tax exemption measures and easier access to these securities [1].

Despite a supportive backdrop from softer gold prices (below $4000/oz) and oil prices (below $75/b), these factors have not yet fully translated into support for the Indian Rupee [1]. The combination of state bank flows, RBI intervention expectations, and robust FPI bond inflows is currently shaping the market dynamics for both the currency and bond markets in India [1].

CONCLUSION

The Indian Rupee's upside against the US Dollar remains capped due to state bank dollar selling and anticipated RBI smoothing operations, despite record FPI inflows into Indian bonds. While softer gold and oil prices could further support the Rupee, their effects have yet to be fully realized. Market participants are closely watching for any changes in RBI policy or external flows that could shift the current equilibrium.