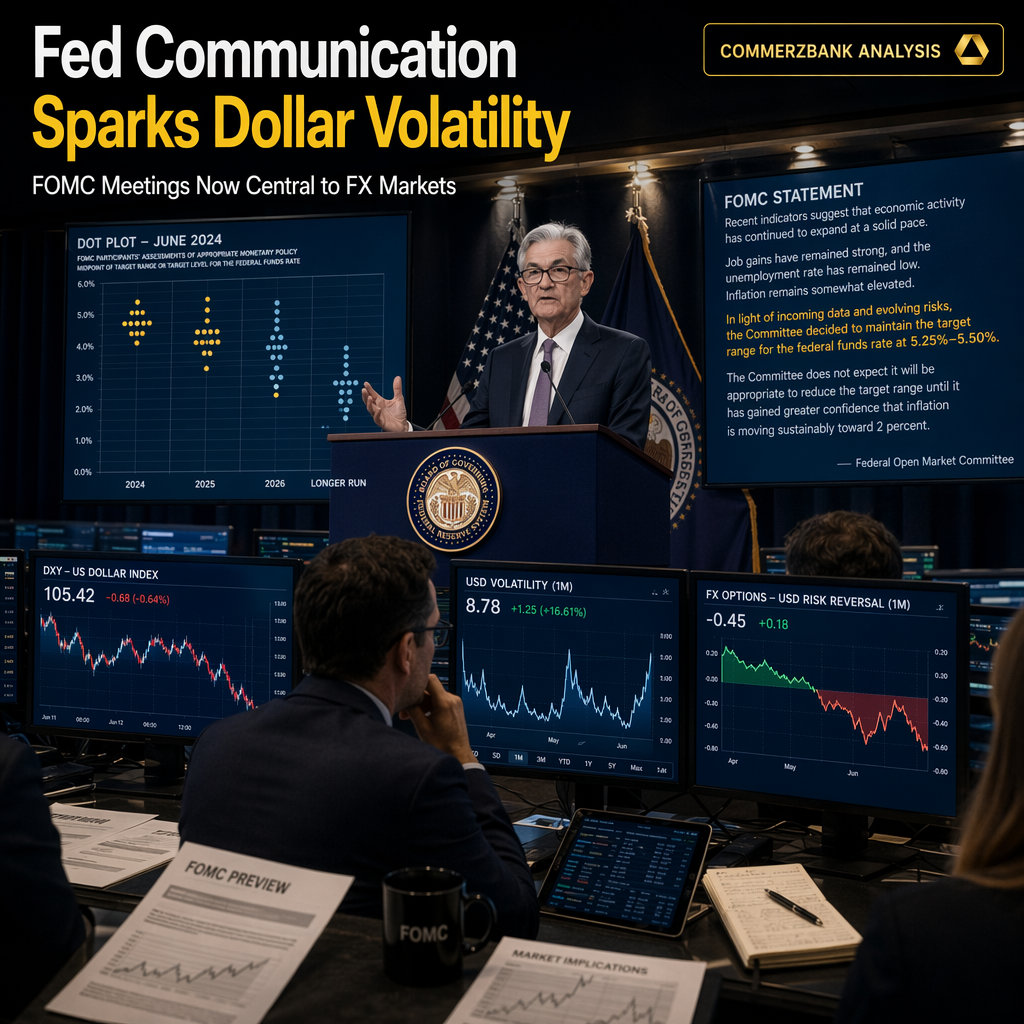

Commerzbank’s Michael Pfister highlights a significant shift in US Dollar volatility patterns due to changes in Federal Reserve communication strategies over the past 30 years, spanning the tenures of Greenspan, Bernanke, Yellen, and Powell [1]. Pfister notes that enhanced Fed communication, including longer statements and the introduction of dot plots, has led to a reduction in average implied volatility for the US Dollar, but has concentrated volatility on FOMC meeting days [1]. Specifically, he quantifies that every additional 100 words in the Fed's statement correlates with a 0.14% increase in volatility on the day of the FOMC decision compared to the preceding ten trading days, though this relationship varies annually [1].

Under Greenspan, FOMC meeting days were no more volatile than other trading days, but since the introduction of dot plots, volatility has become much more focused on meeting days, making these events more significant for foreign exchange markets [1]. Pfister warns that if the Fed were to revert to shorter statements, as advocated by Kevin Warsh, volatility would likely become more evenly distributed throughout the year, rather than disappearing altogether [1]. This redistribution could benefit short-term positioning around FOMC meetings but may increase the need for hedging on non-meeting days [1].

Overall, while the average level of volatility has declined, the distribution has shifted, making FOMC meetings more critical for market participants and potentially altering trading and risk management strategies [1].

CONCLUSION

The evolution of Fed communication has made FOMC meeting days pivotal for US Dollar volatility, concentrating market reactions around these events. While average volatility has decreased, traders may need to adjust strategies if communication styles change, as volatility could become more evenly spread across the year.