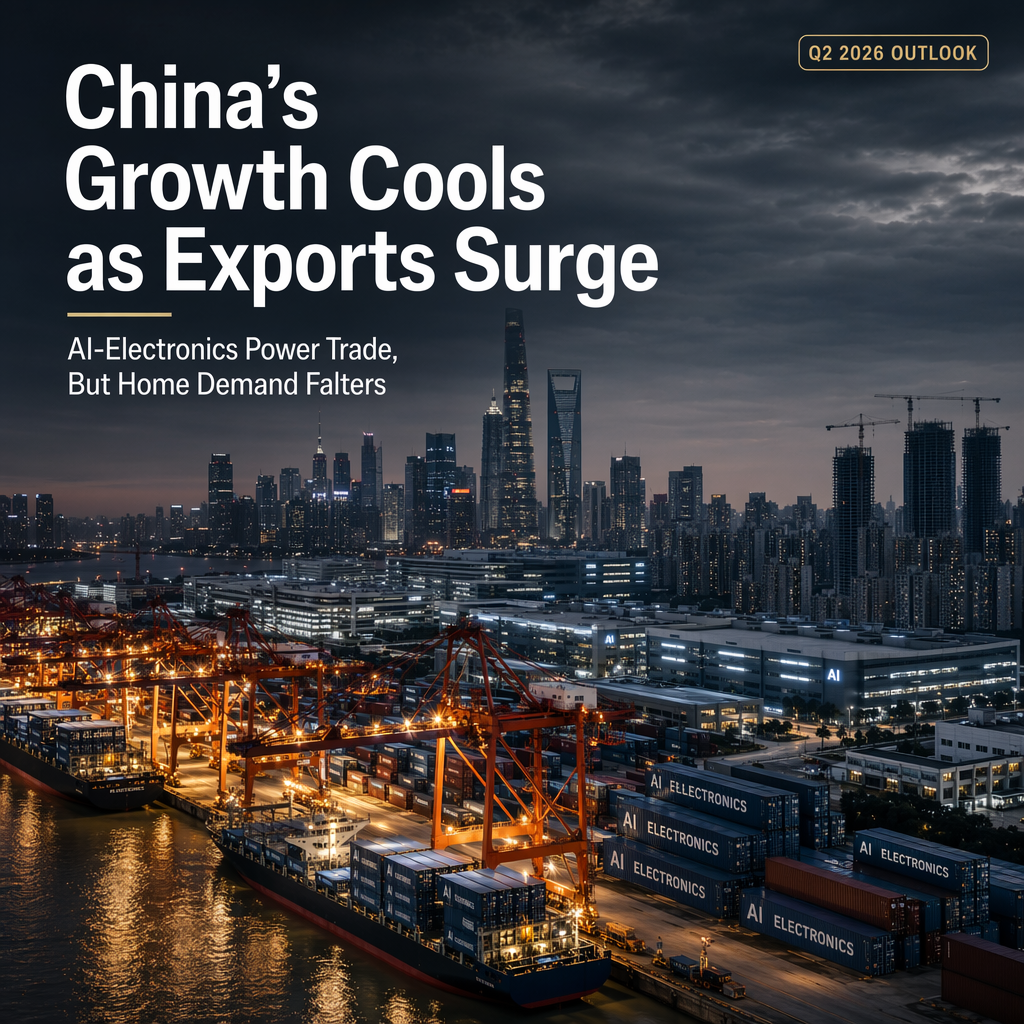

DBS economists Radhika Rao and Mo Ji forecast that China's Gross Domestic Product (GDP) growth will slow from 5.0% year-on-year in the first quarter to 4.8% in the second quarter, citing uneven domestic momentum as a key factor in the deceleration [1]. While industrial production is expected to show a slight improvement, rising from 4.5% in April to 4.6% in June, the economists highlight that this resilience is largely supported by robust external demand [1].

Exports, particularly those related to AI-electronics, are projected to have maintained strong momentum, with export growth reaching 20.4% in June, driven by regional demand for these products [1]. However, the domestic economy faces significant headwinds. Retail sales growth is expected to moderate sharply to 0.5% in June 2026, a slowdown attributed in part to a high base effect from last year's trade-in subsidy programs [1].

The report also points to ongoing challenges in the property sector, with declining property prices continuing to erode household wealth. This trend, combined with subdued household sentiment and falling fixed asset investment, suggests that consumption is likely to remain weak in the near term [1].

Overall, while China's export sector—especially AI-related electronics—remains a bright spot, the broader economic outlook is tempered by persistent weakness in domestic consumption and the property market [1].

CONCLUSION

China's Q2 economic growth is expected to slow, with strong AI-driven exports offsetting weak domestic consumption and ongoing property sector challenges. The market outlook remains cautious, as resilient external demand is counterbalanced by subdued household sentiment and declining property prices.