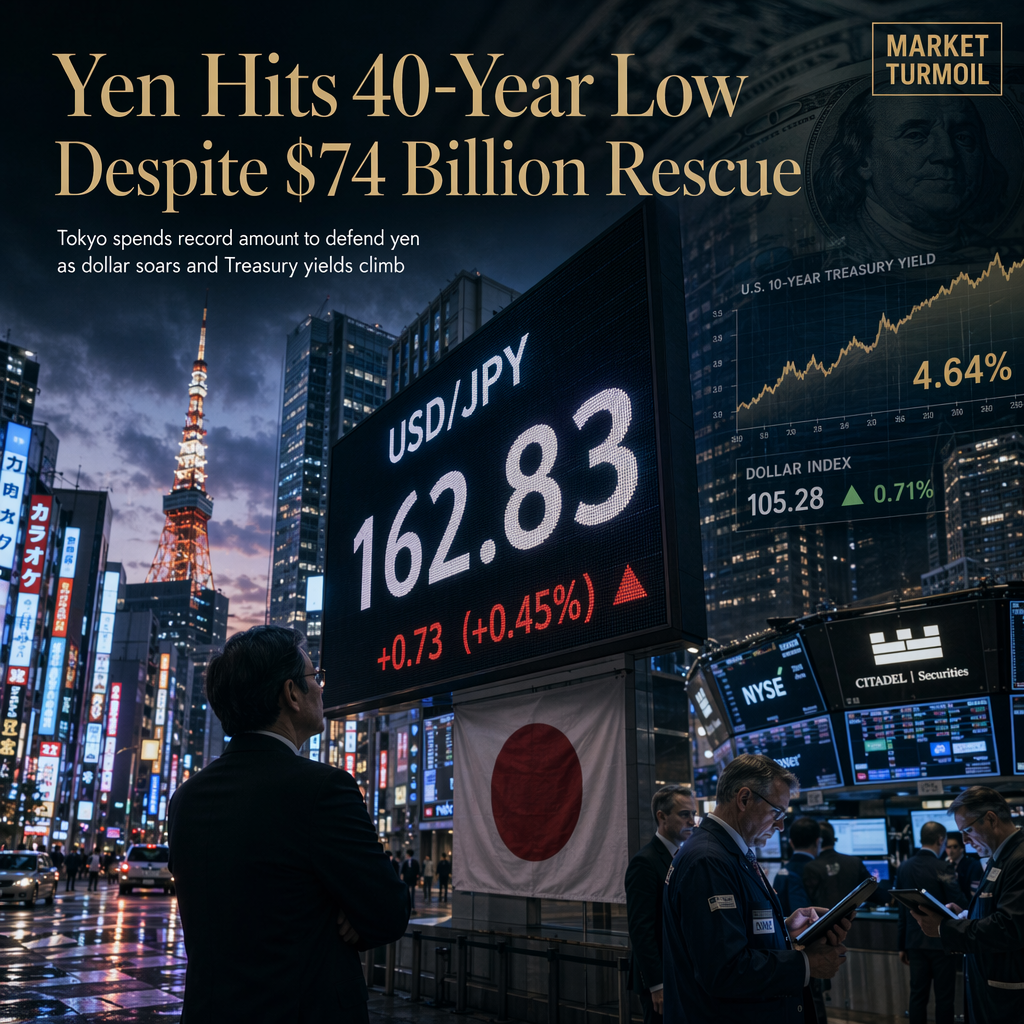

The Japanese yen weakened to 162.83 against the US dollar on Tuesday, marking its lowest level in 40 years, according to LSEG data [4]. This decline comes despite Japan spending a record 11.7 trillion yen ($73.5 billion) in April and May to support its currency through direct intervention [4]. The yen's slide has reignited speculation about further intervention, but investors and strategists cited by CNBC argue that as long as US interest rates remain well above Japan's, intervention alone is unlikely to reverse the trend [4].

The US dollar's strength is being driven by surging US Treasury yields, with the 10-year yield up 0.18% to 4.47% during the European session on Wednesday, extending Tuesday’s gains of over 2% [1][2]. The US Dollar Index (DXY) is up 0.16% to near 101.33, reflecting broad-based dollar strength against major currencies, with the US dollar strongest against the Australian dollar [1][2]. The USD/JPY pair trades 0.1% higher to near 162.73, maintaining a bullish bias and trading well above its 20-day EMA, while the Relative Strength Index (RSI) at 78.45 signals overbought conditions [2].

Market participants attribute the dollar's rally to robust US economic data, including the JOLTS Job Openings for May, which came in at 7.594 million, surpassing both the 7.3 million estimate and the previous reading of 7.585 million [1][2]. Investors are now focused on upcoming US data releases, including the ADP Employment Change, ISM Manufacturing PMI, and the crucial Nonfarm Payrolls (NFP) report, which is expected to show 110,000 new jobs in June versus 172,000 in May, with the unemployment rate seen steady at 4.3% [1]. The CME FedWatch tool indicates an over 82% chance of at least one more Fed rate hike this year [1].

Japanese officials have signaled readiness to intervene further, with Chief Cabinet Secretary Minoru Kihara stating that the administration is always ready to act on forex, though he did not specify any levels [2]. However, analysts cited by CNBC emphasize that the core issue is the widening credibility gap between the Federal Reserve and the Bank of Japan, with the BOJ's latest rate hike to 1% still leaving borrowing costs far below those in the US [4]. The yen has fallen about 3.9% against the dollar this year, compared to a 0.9% decline against the euro, suggesting that the latest pressure is driven by broad dollar strength rather than a loss of confidence in the yen itself [4].

According to Christy Tan of Franklin Templeton Institute, intervention can slow the yen's fall and signal official discomfort, but cannot overcome the fundamental interest rate differential fueling the carry trade [4]. Martin Schulz of Fujitsu adds that the dollar's strength is a key driver, and without a shift in US rates or coordinated action with Washington, any yen rally may be short-lived [4].

CONCLUSION

Despite Japan's record $74 billion intervention, the yen continues to weaken to multi-decade lows as surging US Treasury yields and a strong dollar dominate currency markets. Analysts agree that without a change in US monetary policy or coordinated intervention, Japan's efforts are likely to have only a limited and temporary effect. The market remains focused on upcoming US economic data and Fed policy signals for further direction.