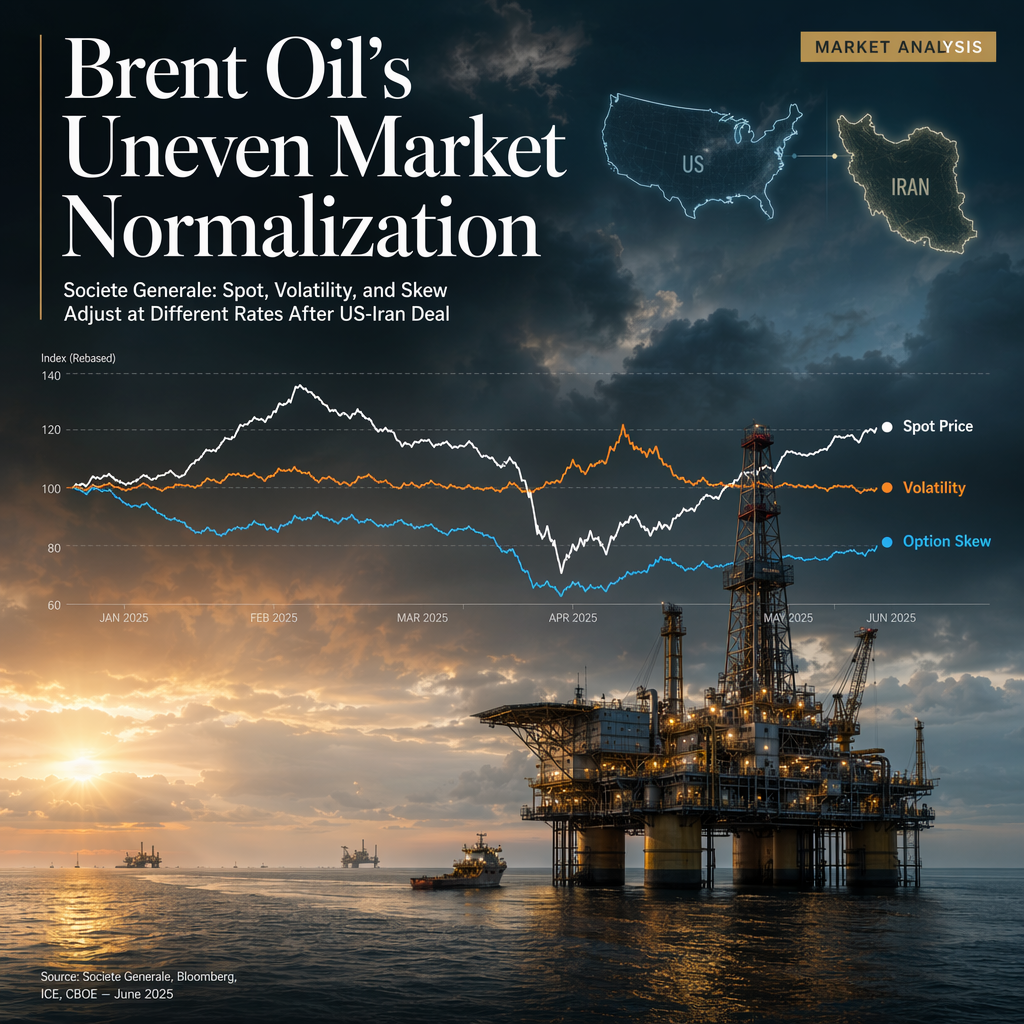

According to Societe Generale analysts Jitesh Kumar and Jeremy Sellem, Brent Oil prices are undergoing a normalization process following the much anticipated US-Iran deal, but the pace and extent of normalization differ across key market parameters such as spot prices, volatility, and option skew [1]. The analysts specifically examine the 4th Brent future for spot price movements, the 3-month implied volatility of Brent futures, and the ratio of 25% delta call option volatility to 25% delta put option volatility to assess market adjustments [1].

The report benchmarks these metrics against early-2026 stress levels, with the starting level at the beginning of 2026 marked as 0% and the highest point during 2026 marked as 100%. This approach allows the analysts to evaluate how much each parameter has retraced from its peak stress point [1]. Notably, they find that the maximum stress levels were reached first in volatility on March 12, 2026 [1].

While Brent spot prices are starting to normalize, the normalization paths for volatility and option skew are described as 'very different,' indicating that not all market segments are adjusting at the same rate or to the same extent following the US-Iran deal [1]. The analysis suggests that market participants are responding unevenly across different risk and pricing metrics as the geopolitical landscape shifts [1].

No specific forward-looking statements or analyst opinions regarding future price direction or market stability are provided in the source [1].

CONCLUSION

Brent oil market metrics are normalizing after the US-Iran deal, but the process is uneven across spot prices, volatility, and option skew. Societe Generale's analysis highlights that volatility peaked first, and each parameter is retracing from its stress levels at a different pace. Market participants should note the differentiated adjustment paths in assessing ongoing oil market risks.