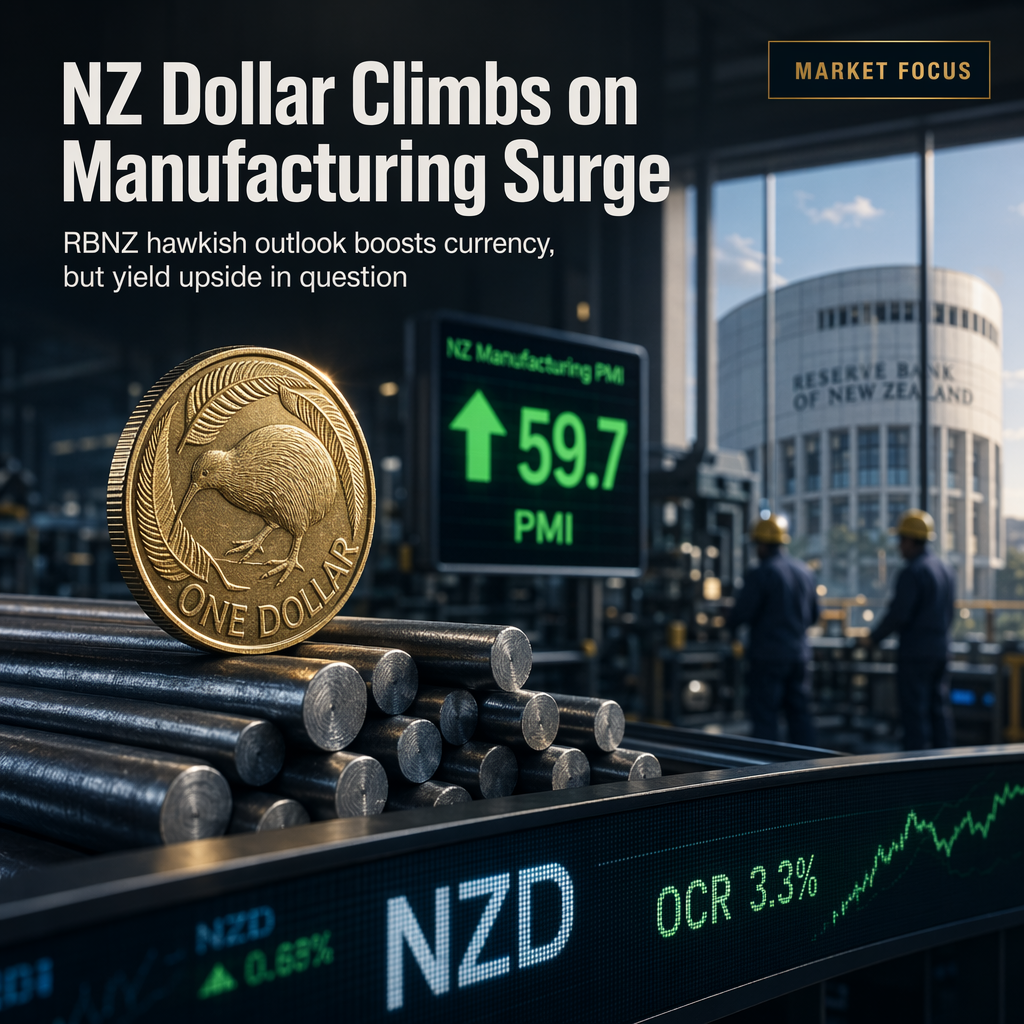

The New Zealand Dollar (NZD) has outperformed following stronger-than-expected manufacturing data and hawkish commentary from the Reserve Bank of New Zealand (RBNZ), according to OCBC strategists Christopher Wong and Sim Moh Siong [1]. New Zealand's manufacturing Purchasing Managers' Index (PMI) rose to 59.7 in June, marking its highest level since July 2021 [1]. This robust data, combined with the RBNZ's stance, has reinforced market expectations for further monetary tightening.

Markets are currently pricing the RBNZ as the most hawkish central bank among the G10, with approximately 80 basis points of additional tightening anticipated by mid-2027. This would bring the Official Cash Rate (OCR) to about 3.3%, which is broadly in line with the RBNZ's estimate of the neutral rate at 3.25% [1].

Despite the constructive outlook for the NZD, OCBC strategists caution that the potential for New Zealand yields to rise significantly in the near term may be limited. They note that clearer evidence of stronger domestic growth and a more supportive energy backdrop would be needed to drive yields higher. As a result, the relative yield support that has been a key driver for the NZD could become less compelling in the short run [1].

Looking ahead, market participants are focused on upcoming data releases, including New Zealand's second quarter 2026 Consumer Price Index (CPI) on 21 July and the second quarter 2026 employment report on 5 August, which could influence the RBNZ's policy trajectory and the NZD's performance [1].

CONCLUSION

The New Zealand Dollar has gained on strong manufacturing data and hawkish RBNZ expectations, but further upside from yields may be capped without additional growth or energy support. Investors are watching upcoming CPI and employment data for further direction.