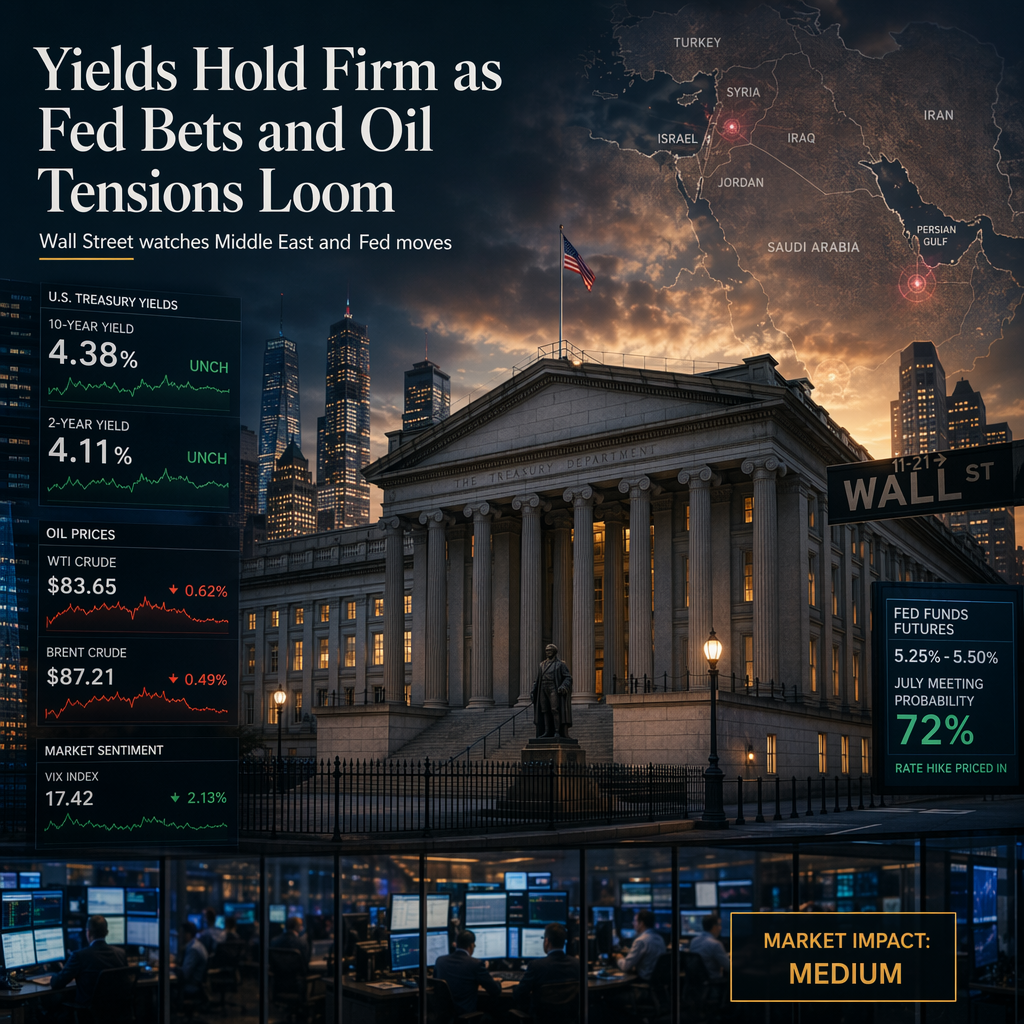

US Treasury yields remained steady during the North American session on Monday, as ongoing tensions in the Middle East halted the decline in crude oil prices and market participants continued to price in Federal Reserve tightening for 2026 [1]. The benchmark US 10-year Treasury note yield rose by 1 basis point to 4.38%, while the 2-year Treasury yield, which is highly sensitive to monetary policy changes, increased nearly 2% to 4.11% [1]. Money markets are currently pricing in at least 34 basis points of Fed tightening towards the end of the year [1].

Negotiations between US and Iranian teams are expected to take place in Doha, according to Reuters, which may influence oil prices and broader market sentiment [1]. Meanwhile, the US Dollar Index (DXY) fell 0.28% to 101.08, as traders shifted towards riskier assets [1]. Inflation expectations, as measured by the 5- and 10-year breakeven rates, are at 2.21% and 2.20%, respectively, down from their mid-April peaks of 2.72% and 2.5% [1].

The US economic calendar is set to be busy, with upcoming events including the appearance of new Fed Chair Kevin Warsh at Sintra in Portugal, as well as key data releases such as JOLTS job openings, ISM Manufacturing PMI, jobless claims, and the US Nonfarm Payrolls for June. These events are expected to provide further insight into the US jobs market and potentially influence future monetary policy decisions [1].

CONCLUSION

US Treasury yields are holding firm as Fed tightening bets and geopolitical tensions in the Middle East impact market sentiment. The upcoming US economic data releases and Fed Chair appearance are likely to provide additional direction for yields and broader financial markets. Overall, the market impact is medium, with investors closely watching both monetary policy signals and geopolitical developments.