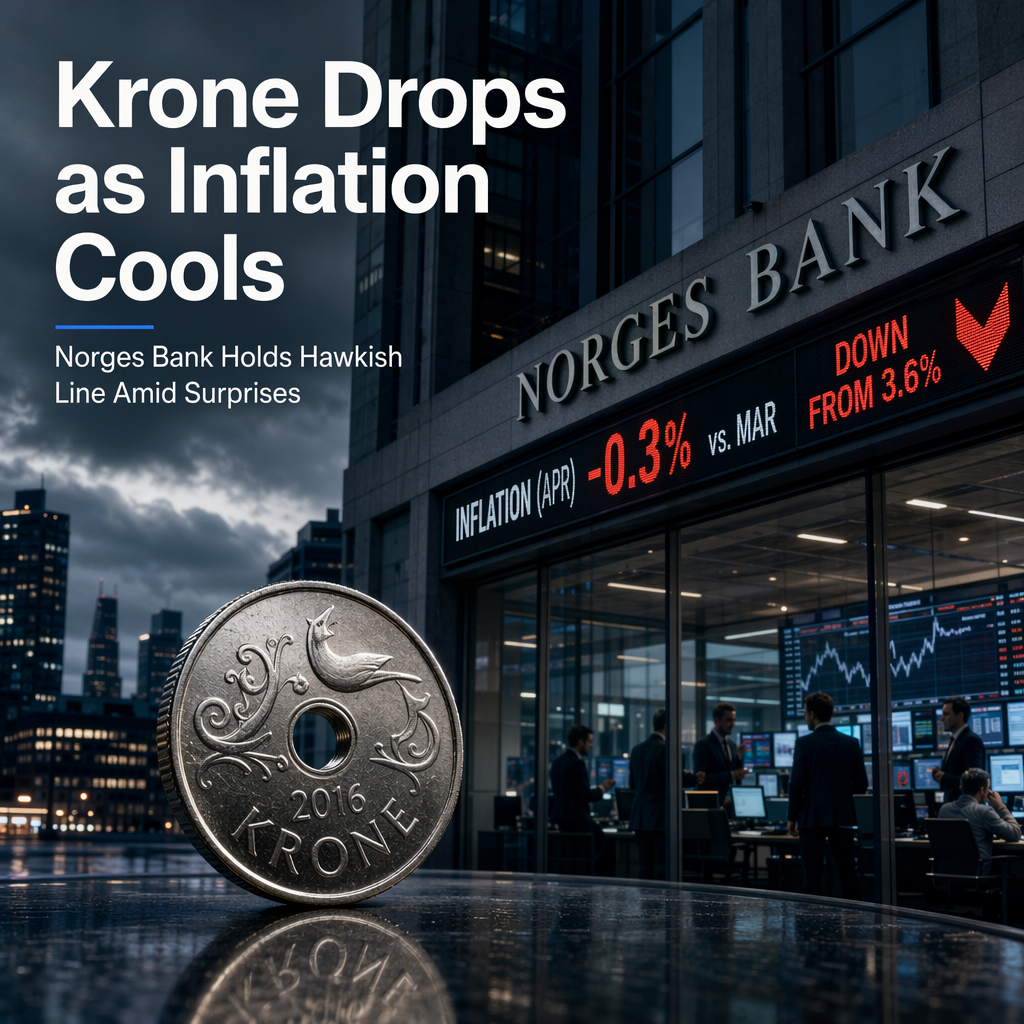

The Norwegian Krone (NOK) experienced broad underperformance following a significant drop in Norway's underlying inflation, which reached an 18-month low. According to Brown Brothers Harriman’s (BBH) Elias Haddad, underlying CPI fell sharply to 2.7% year-over-year in June, down from 3.4% in May. This figure was below both the Norges Bank and consensus projections, which had anticipated 3.3% year-over-year inflation [1].

Despite the softer inflation print, BBH does not expect this single data point to alter the Norges Bank’s hawkish policy stance. Inflation has remained above target for several years, supporting the case for continued tight monetary policy. At its last meeting on June 17, the Norges Bank kept the policy rate unchanged at 4.25% but indicated that a rate hike could occur at one of the upcoming monetary policy meetings. The next policy decision is scheduled for August 13, with markets currently pricing in a 42% probability of a 25 basis point hike and expecting rates to peak at 4.50% by year-end [1].

BBH anticipates one more rate increase before the Norges Bank pauses, noting that the current policy rate is already above the Bank’s neutral rate estimate, which ranges between 2.25% and 3.75%. Additionally, Norway’s output gap is slightly below zero, suggesting limited room for further tightening [1].

The prospect of only one additional rate hike, combined with the policy rate already being above neutral, is viewed as a headwind for the NOK, contributing to its recent underperformance [1].

CONCLUSION

Norway's inflation has cooled more than expected, but the Norges Bank is likely to maintain its hawkish stance, with one more rate hike anticipated by year-end. This outlook, alongside the policy rate already exceeding neutral estimates, is seen as a negative factor for the Norwegian Krone in the near term.