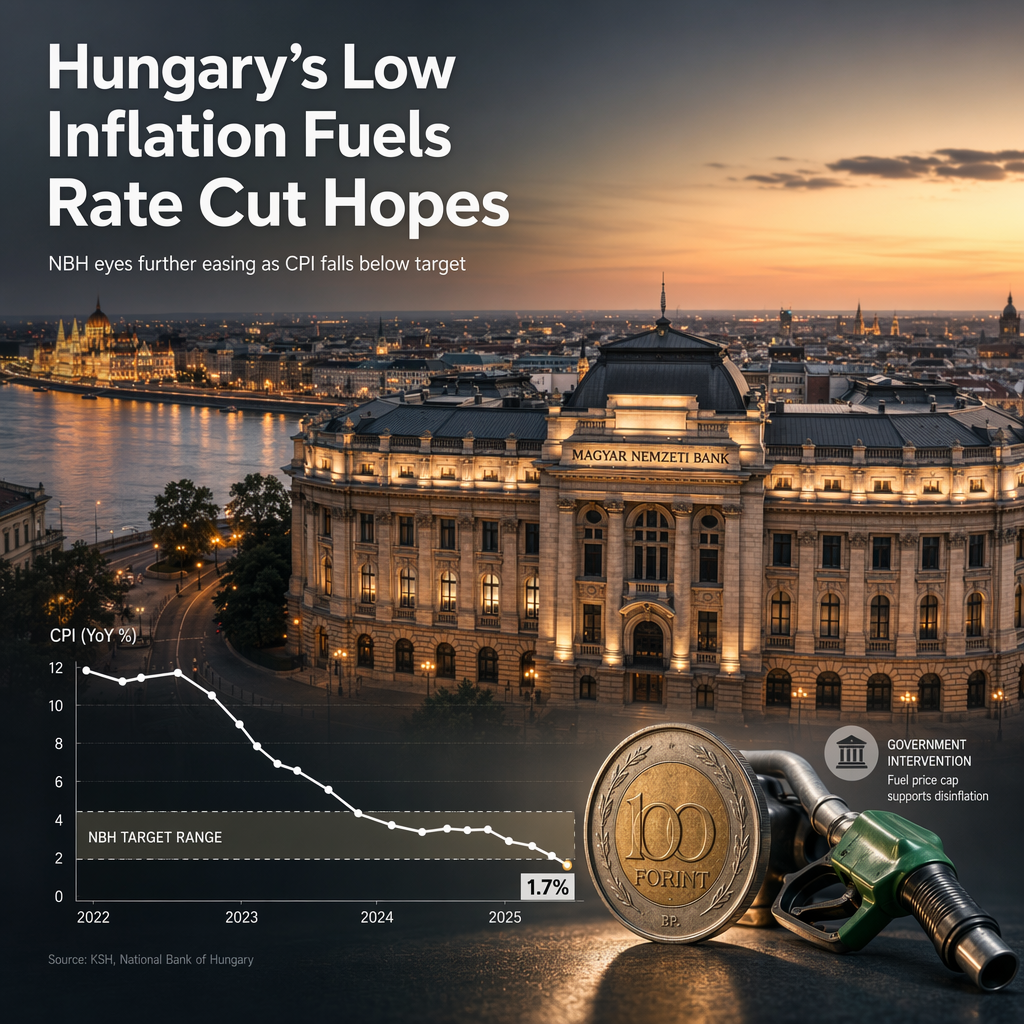

Standard Chartered’s Saabir Salad highlights that Hungary's inflation has remained subdued, with headline Consumer Price Index (CPI) registering at 1.8% year-on-year in May. This figure is below both Standard Chartered's forecast of 2.2% and the lower bound of the National Bank of Hungary’s (NBH) 3% +/-1 percentage point target range [1]. The subdued inflation is attributed to a strong Hungarian Forint (HUF) and government interventions such as fuel price caps [1].

In response to the lower-than-expected inflation, Standard Chartered has revised its CPI forecasts downward, projecting 2.2% for 2026 (previously 3.9%) and 2.5% for 2027 (previously 3.4%). These forecasts remain above the central bank’s own projections [1]. Despite the current low inflation, Salad notes that upside risks persist, particularly due to Hungary’s vulnerability to geopolitical instability. While the NBH views inflation risks as balanced, Standard Chartered maintains that risks are skewed to the upside, which could slow the pace of monetary easing if realized [1].

The overall market implication is that the NBH is likely to maintain a dovish stance and continue with rate cuts, but the trajectory of easing may be tempered if inflationary pressures re-emerge [1].

CONCLUSION

Hungary's lower-than-expected inflation has provided room for the NBH to pursue rate cuts, according to Standard Chartered. However, persistent upside risks mean the pace of monetary easing could slow if inflation rises, keeping markets attentive to future data and geopolitical developments.