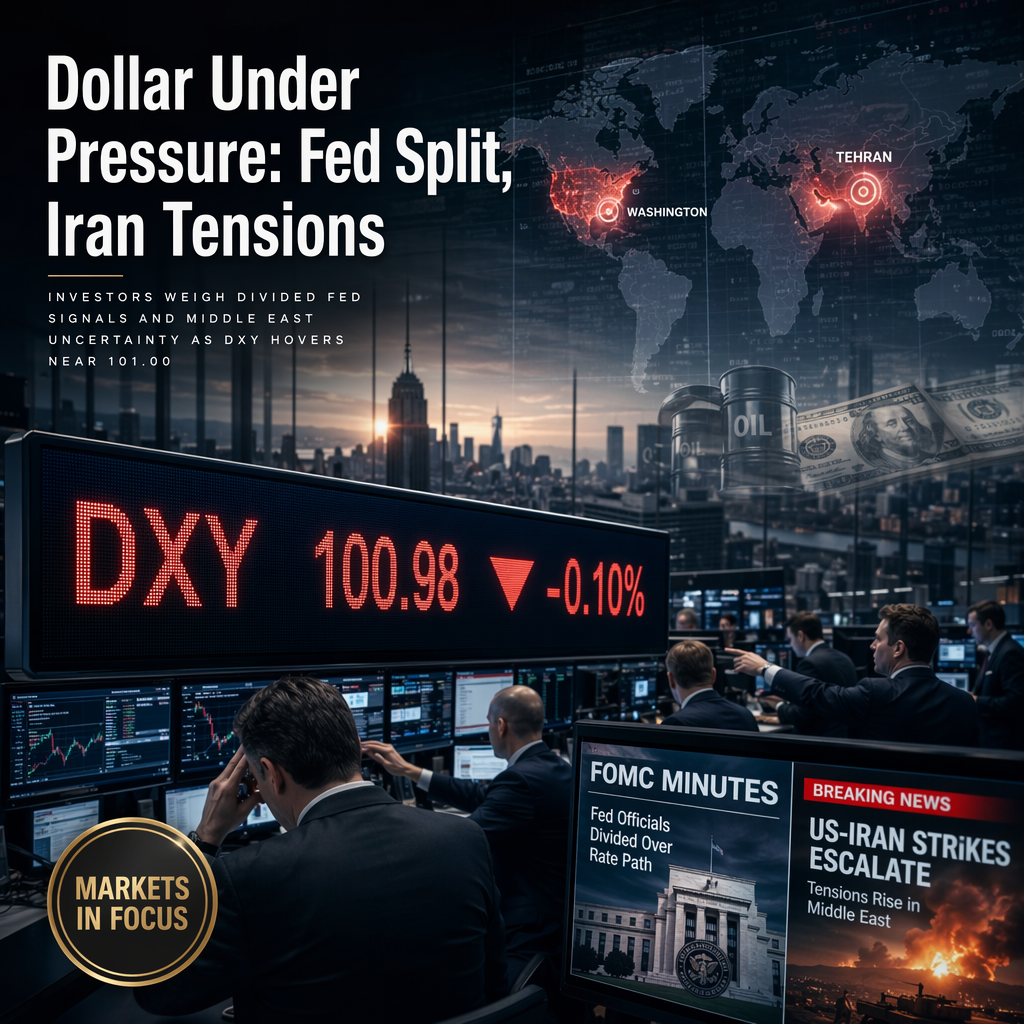

The US Dollar Index (DXY), which measures the Greenback against a basket of major currencies, traded with a negative bias for the second consecutive day, remaining just below the 101.00 mark and down 0.10% for the day as of Thursday's Asian session [1]. The index's movement reflects investor hesitation, attributed to the lack of a notable hawkish shift in the latest FOMC Minutes and ongoing geopolitical risks involving Iran [1].

The FOMC Minutes from the June 16–17 meeting, released on Wednesday, revealed that policymakers were divided on the direction of interest rates. Many participants indicated that the appropriate level of the fed funds rate would be within or slightly below the current target range by the end of the year. However, officials also noted that upside risks to inflation remain elevated, suggesting that some policy tightening may be warranted to return inflation to the 2% target [1].

Market participants are currently pricing in a roughly 70% chance that the Federal Reserve will raise borrowing costs by 25 basis points in September [1]. Geopolitical developments have also influenced market sentiment: a new wave of US military strikes against Iran, in retaliation for attacks on commercial ships in the Strait of Hormuz, led to a sharp rally in oil prices and revived inflation concerns. Iran responded by targeting US military installations and assets in Bahrain and Kuwait. Additionally, US President Donald Trump announced that the memorandum of understanding aimed at ending the Middle East conflict is now over, adding further uncertainty [1].

In terms of currency performance, the US Dollar was the strongest against the Canadian Dollar, with a change of -0.08%, and showed declines against other major currencies such as the Euro (-0.14%), British Pound (-0.14%), Japanese Yen (-0.11%), Australian Dollar (-0.15%), New Zealand Dollar (-0.52%), and Swiss Franc (-0.23%) [1]. Traders are now looking to US Weekly Jobless Claims for further market direction [1].

CONCLUSION

The US Dollar Index remains under pressure near 101.00, weighed by divided Fed policy signals and heightened geopolitical tensions with Iran. While inflation risks and potential Fed tightening provide some support, market sentiment remains cautious as traders await further economic data for direction.