Crude Oil markets have experienced a significant selloff, with West Texas Intermediate (WTI) prices sliding toward the mid-$70s and Brent crude falling to just under $80. This decline has effectively erased nearly all the premium that was built up since the Strait of Hormuz was restricted in late February, following news of an interim US-Iran ceasefire and the resumption of tanker traffic through the waterway [1]. However, the ceasefire is already showing signs of instability, as the first round of talks has been delayed from Friday to the middle of next week [1].

Despite the market's reaction, the physical oil market does not reflect the optimism priced into futures. The selloff is based on the assumption that cheaper crude will lead to lower prices across the supply chain, but refined products such as diesel, jet fuel, and petrochemical feedstocks remain tight. Margins on middle distillates have reached multi-year highs, and regional jet fuel margins have spiked to levels seen only when supply is critically short [1].

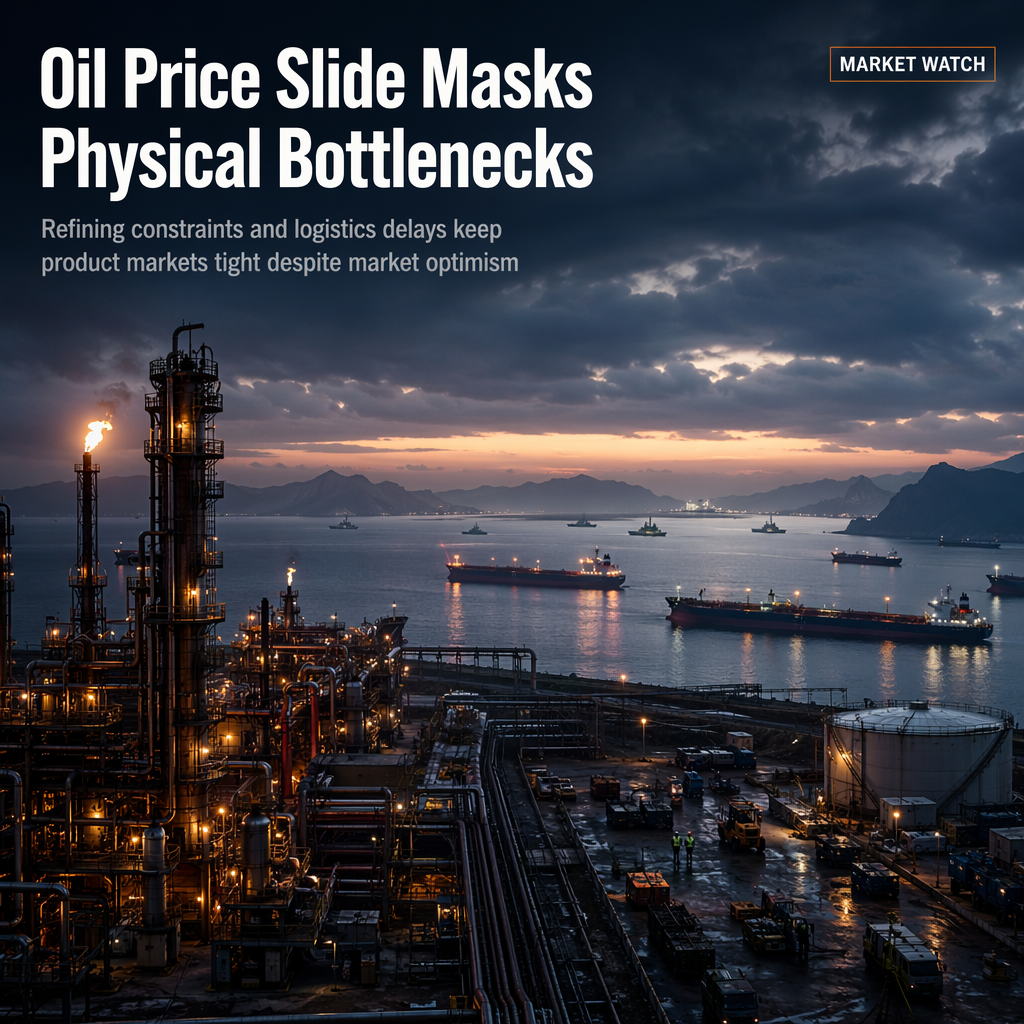

A key constraint is refining capacity, which has been reduced by over a million barrels per day due to permanent plant closures—a situation that cannot be quickly reversed by any peace deal. Additionally, the lighter grades favored by US shale production are less effective at producing the middle-distillate cuts needed for diesel and jet fuel, meaning increased domestic crude supply does little to alleviate the tightness in these products [1].

Upstream, commercial stockpiles at the main US delivery hub have declined for eight consecutive weeks to approximately 20 million barrels, a level considered the operational floor by traders. The broadest measure of US stocks is now at levels last seen in the mid-1980s, driven by record exports as the US became the seller of last resort during the Gulf supply disruption [1]. The reopening of the Strait of Hormuz is not expected to immediately restore flows, as clearing mines and repositioning tankers will take months, and restarting shut-in fields could take even longer due to potential reservoir damage. Consultants have warned that flows may not return to pre-war levels until well into next year, suggesting the market has prematurely priced in a full recovery [1].

CONCLUSION

While crude oil prices have fallen sharply on expectations of a swift supply recovery, underlying physical constraints in refining and logistics suggest that product markets will remain tight. The market may have overestimated the speed of normalization, with analysts warning that a full recovery in flows could take until next year.