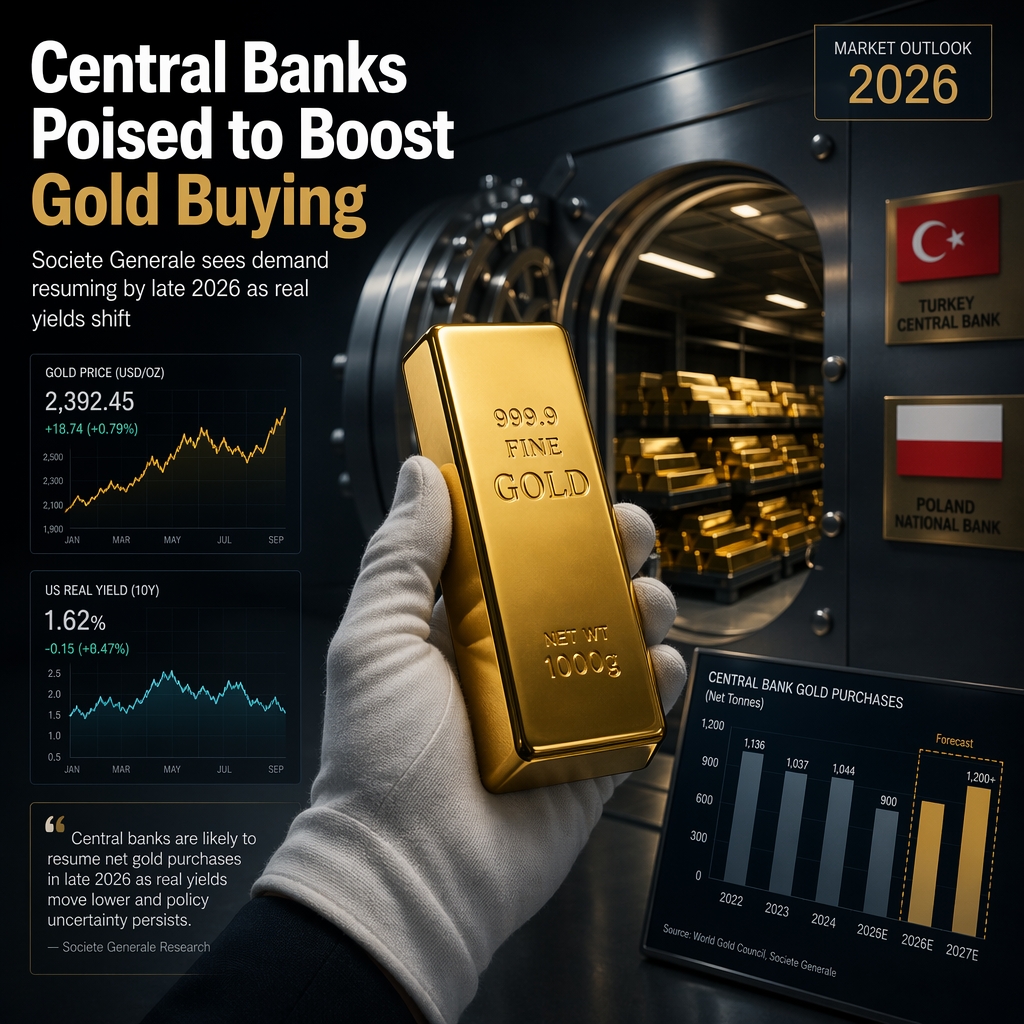

Societe Generale strategists Michael Haigh and Jeremy Sellem analyzed the latest World Gold Council (WGC) central bank survey data and market flows to assess central bank demand for gold. According to their findings, net central bank gold purchases year to date have been modest at +40 tonnes, with Turkey and Poland accounting for two-thirds of this total activity [1]. The strategists highlighted that stated central bank intentions in the WGC survey are more reliable over a six-month post-survey window, rather than a full year, due to the limited visibility central banks have over longer horizons [1].

Applying their regression framework to the 2026 survey responses, Societe Generale estimates additional central bank gold purchases of approximately 100–120 tonnes over the remainder of 2026. This figure is roughly double the volume recorded in the first four months of the year and aligns with their broader expectation for a resumption of visible central bank buying from Q4 2026 [1]. The conviction in this outlook is supported by market signals, including outflows from LBMA vaults and an increase in UK gold exports. Specifically, a 20-tonne increase in vault holdings is associated with a pickup in export activity to around 61 tonnes, which, while slightly below the post-2022 average of 73 tonnes, is above the 53-tonne average since 2015 for this period, indicating a meaningful improvement in underlying central bank demand [1].

Regarding market implications, Societe Generale notes that gold prices remain closely linked to US real yields. Their economists' central scenario projects that 10-year US real yields will stay above 2% through Q3, before gradually declining into year-end and into the first half of 2027. This outlook supports a neutral stance on gold over the summer, with the potential for a more constructive view later in the year as the opportunity cost of holding gold is expected to ease [1].

CONCLUSION

Societe Generale anticipates a significant pickup in central bank gold buying from late 2026, supported by survey data and market flows. While maintaining a neutral near-term outlook due to elevated US real yields, the strategists see scope for a more positive stance on gold as yields decline into 2027. Market participants may look for renewed central bank demand as a key driver for gold prices in the coming quarters.