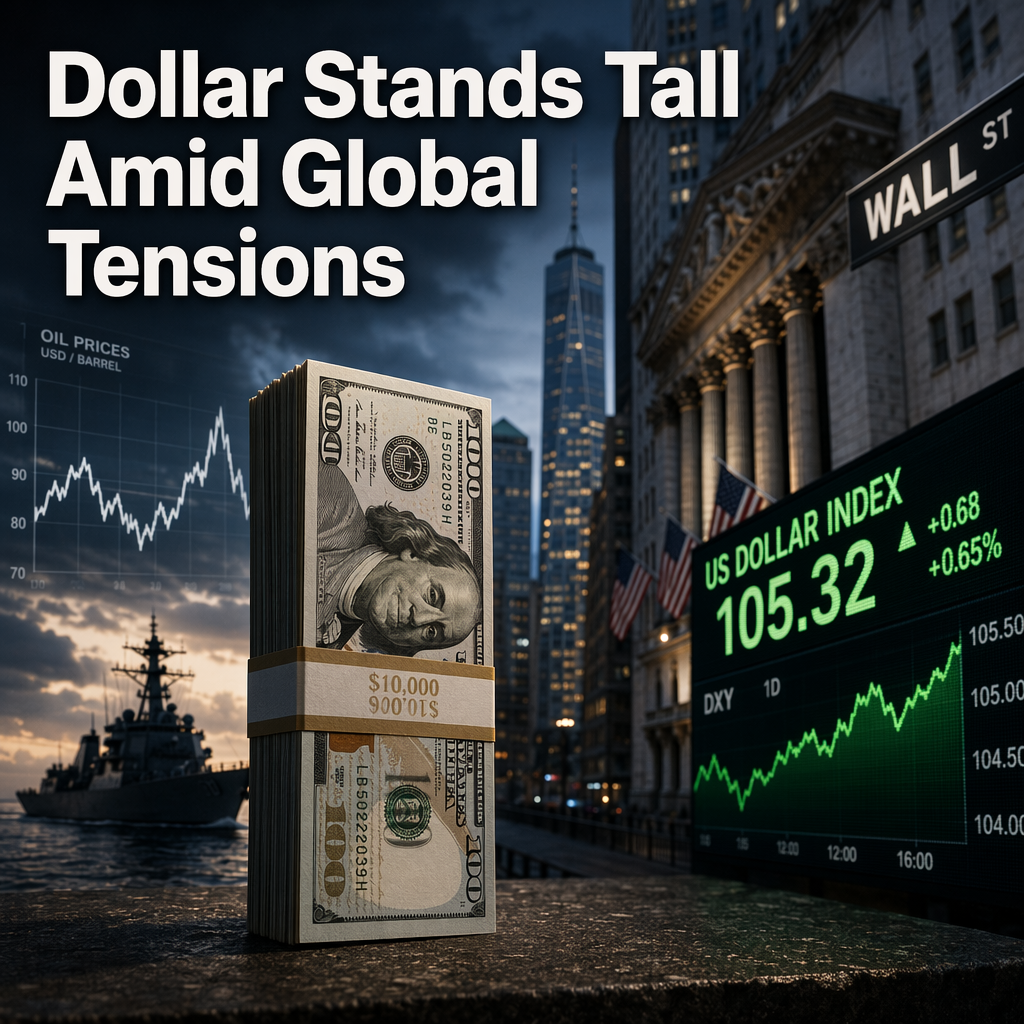

Renewed tensions in the Middle East have led to increased pressure on global stocks and bonds, while simultaneously providing support for the US Dollar (USD) and crude oil prices, according to Brown Brothers Harriman’s (BBH) Elias Haddad [1]. The US Dollar Index (DXY) has edged higher, with US-G6 two-year yield spreads indicating that the DXY is likely to trade slightly above 102.00. This movement is further underpinned by US economic outperformance, which continues to keep rate differentials favorable for the dollar ahead of the release of the FOMC meeting minutes [1].

The US recently conducted a new round of offensive strikes against Iran and revoked a waiver that previously allowed the sale of Iranian oil, actions taken in response to Iran's attacks on commercial vessels in the Strait of Hormuz [1]. These developments have contributed to the surge in crude oil prices and the strengthening of the USD [1].

On the monetary policy front, the FOMC left the target range for the federal funds rate unchanged at 3.50%-3.75% for the fourth consecutive meeting, a decision that was widely anticipated and made without dissent. Notably, the FOMC statement removed its implicit easing bias, signaling a more hawkish stance [1]. The upcoming release of the FOMC June 16-17 meeting minutes is expected to provide further insights into the committee's debate behind this hawkish hold [1].

CONCLUSION

Geopolitical tensions and a firm US rate backdrop are supporting the US Dollar and oil prices, while weighing on stocks and bonds. Market participants are now looking to the FOMC meeting minutes for additional clarity on the Federal Reserve's policy outlook.