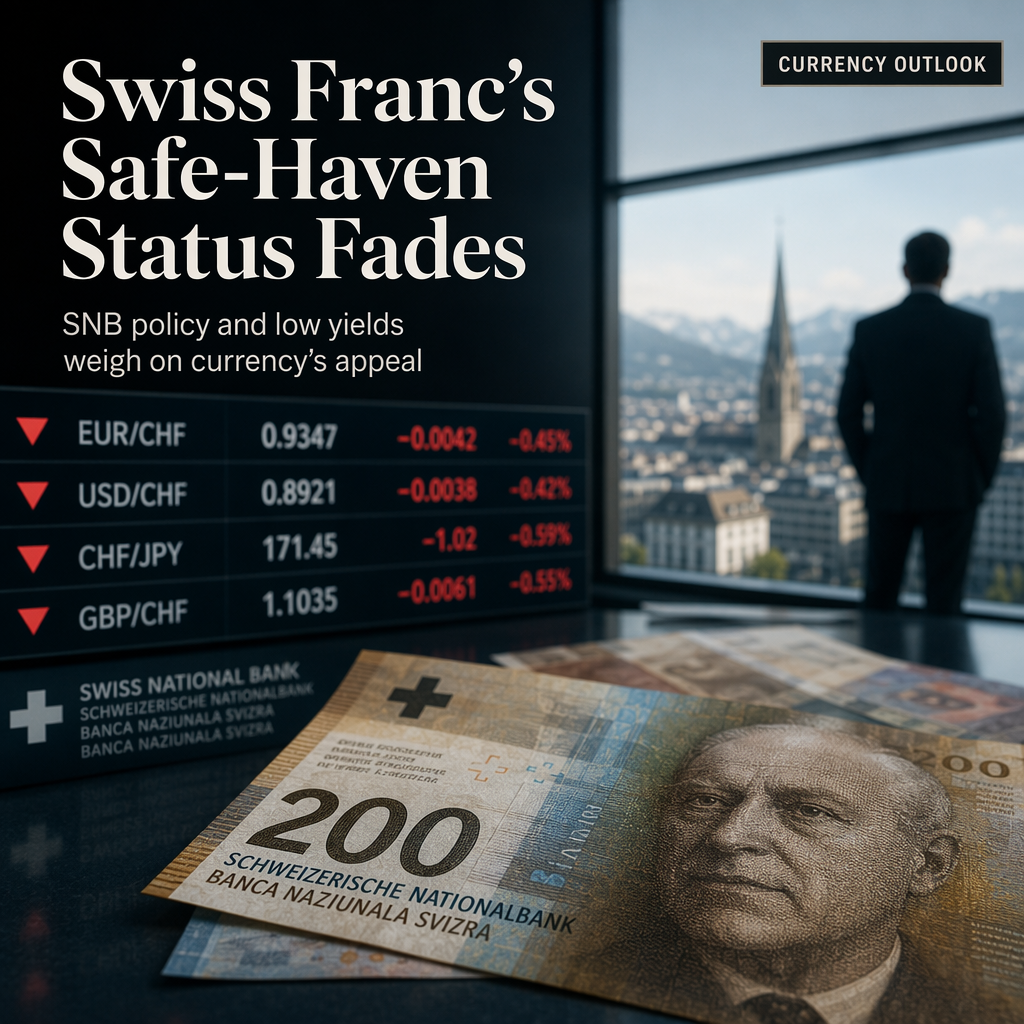

According to OCBC Bank strategists Sim Moh Siong and Christopher Wong, the Swiss Franc (CHF) has lost much of its traditional safe-haven appeal due to the Swiss National Bank's (SNB) willingness to intervene in the foreign exchange market and persistently low yields. The strategists highlight that the CHF has underperformed as these factors continue to weigh on the currency's performance [1].

The SNB, in its summary of the 18 June policy meeting, stated that monetary conditions remain appropriate and indicated no immediate need for further action, despite acknowledging rising upside inflation risks. The SNB's increased readiness to intervene, particularly since the outbreak of the US-Iran conflict, has further reduced the CHF's attractiveness as a safe-haven asset. As a result, the CHF is now being driven more by interest rate dynamics than by risk aversion [1].

Swiss inflation remains below the midpoint of the SNB's 0-2% price stability range, which suggests that policy rates are likely to remain at zero for at least the rest of the year. In the context of rising global yields, this environment is expected to keep the CHF as one of the laggards among G10 currencies, despite Switzerland's sizeable current account surplus [1].

CONCLUSION

The Swiss Franc is expected to remain under pressure due to the SNB's intervention risk and low yields, which have eroded its safe-haven status. With policy rates likely to stay at zero and inflation below target, the CHF is anticipated to lag behind other G10 currencies in the near term.