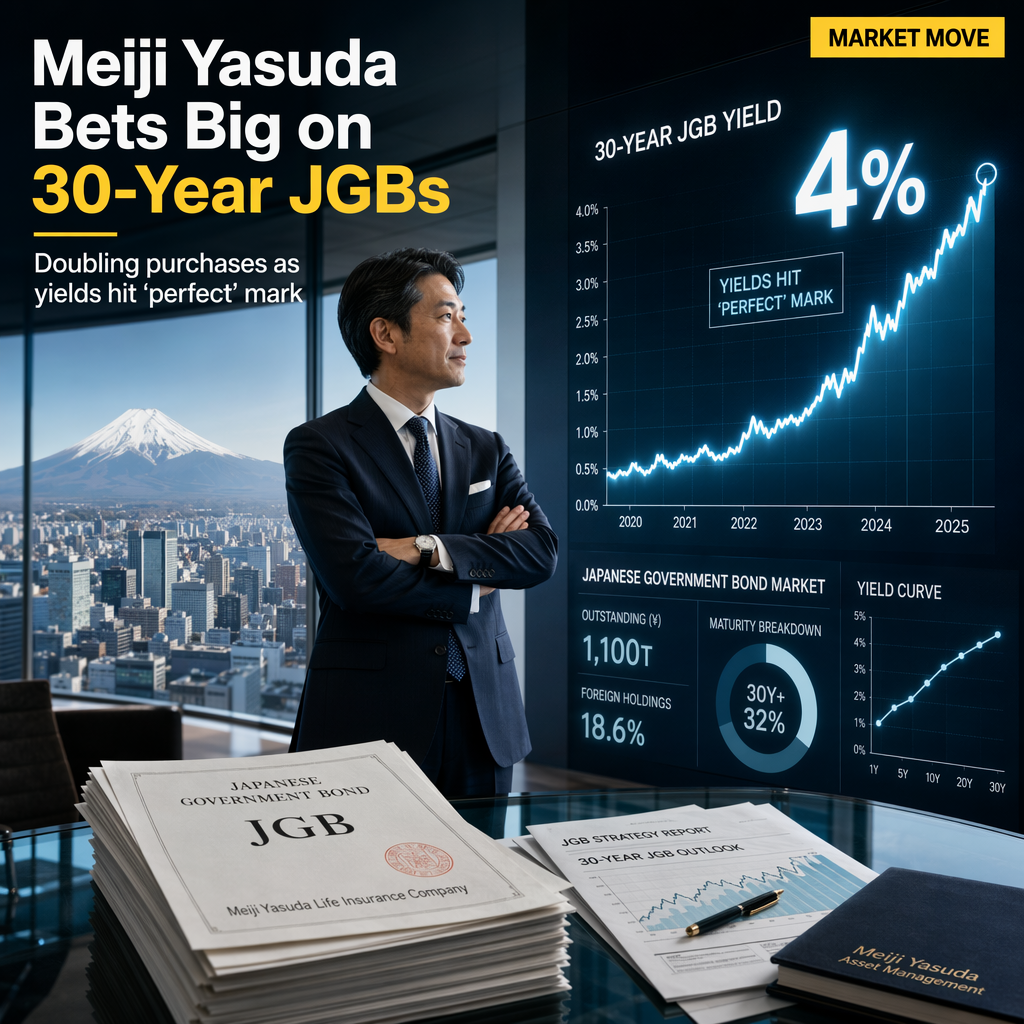

Meiji Yasuda Life Insurance has announced it will double its planned purchases of Japanese government bonds (JGBs) for fiscal 2026, raising its target to more than 2 trillion yen ($12.3 billion) [1]. This strategic move is driven by the insurer's view that current yields of around 4% for 30-year JGBs represent a 'perfect buying opportunity,' according to the head of its asset management business [1].

The company plans to fund these increased purchases by selling off low-yield JGBs acquired in the past, reallocating its portfolio to take advantage of what it considers attractive yields in the ultralong segment [1]. This decision follows several months of volatility in ultralong-bond yields, which Meiji Yasuda now expects to stabilize [1].

The insurer's approach signals a strong vote of confidence in the current JGB market environment, particularly for longer maturities. While many Japanese insurers have recently shown caution due to soaring yields and ongoing policy adjustments by the Bank of Japan, Meiji Yasuda is taking a more aggressive stance, actively rotating from legacy holdings and deploying fresh capital into higher-yielding bonds [1].

The head of asset management emphasized the alignment of this strategy with the company's long-term liabilities, stating, 'With 30-year JGBs yielding around 4%, this is a perfect buying opportunity for us, especially given our long-term liabilities' [1]. The overall market sentiment described in the article is bullish on ultralong JGBs at current yield levels, with expectations that yields have peaked and will stabilize going forward [1].

CONCLUSION

Meiji Yasuda Life's decision to double its JGB purchases underscores a bullish outlook on ultralong Japanese government bonds, setting it apart from more cautious peers. The insurer's move may influence market sentiment and activity in the JGB market, particularly for longer maturities, as it reallocates capital to take advantage of what it sees as attractive yields.