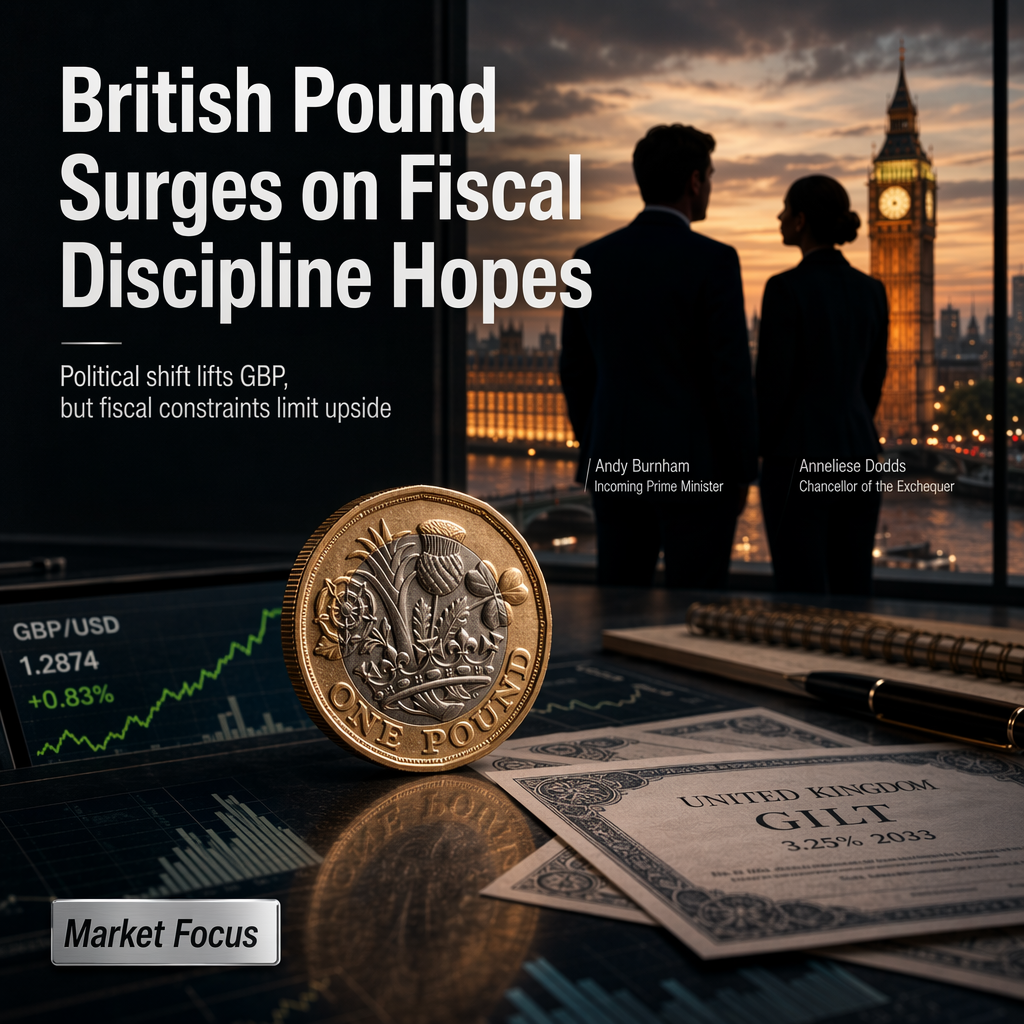

The British Pound (GBP) experienced a notable rally following reports that incoming UK Prime Minister Burnham is likely to appoint Shabana Mahmood as Chancellor, a move perceived as fiscally conservative and market-friendly. This development has supported both GBP and UK government bonds (gilts), with OCBC strategists highlighting that hopes for fiscal discipline under Mahmood have shaped the currency's outlook [1][2]. The Pound strengthened across the board, particularly against the Japanese Yen (JPY), reaching its highest level since December 2007 before easing slightly to trade around 219.00, down 0.25% on the day [2]. The GBP/JPY cross retains an upside bias, supported by easing political uncertainty and expectations of greater fiscal discipline, as well as renewed inflation risks from rising oil prices and potential Bank of England (BoE) rate hikes [2]. However, BoE Deputy Governor Sarah Breeden cautioned that the Iran war shock is less likely to lead to sustained inflationary dynamics, suggesting the BoE is well-positioned to monitor developments [2]. Despite the positive momentum, OCBC strategists and the OECD warn that high public debt, elevated interest costs, and rising healthcare and social care spending pressures significantly constrain fiscal flexibility, limiting further GBP upside [1]. OCBC expects the recent EUR/GBP correction to fade, projecting the cross to recover towards 0.87 in the coming months, consistent with a range-bound view on the Pound [1]. Meanwhile, Japanese authorities remain vigilant, with Finance Minister Satsuki Katayama reiterating readiness to intervene in the currency market if needed, as broad-based Yen weakness persists [2].

CONCLUSION

The British Pound's recent rally is driven by expectations of fiscal discipline under a new Chancellor and easing political uncertainty, but structural fiscal constraints and spending pressures limit further upside. Analysts anticipate a range-bound GBP outlook, with EUR/GBP likely to recover towards 0.87. Market participants remain alert to potential interventions in the Yen and ongoing inflation risks, keeping volatility elevated.