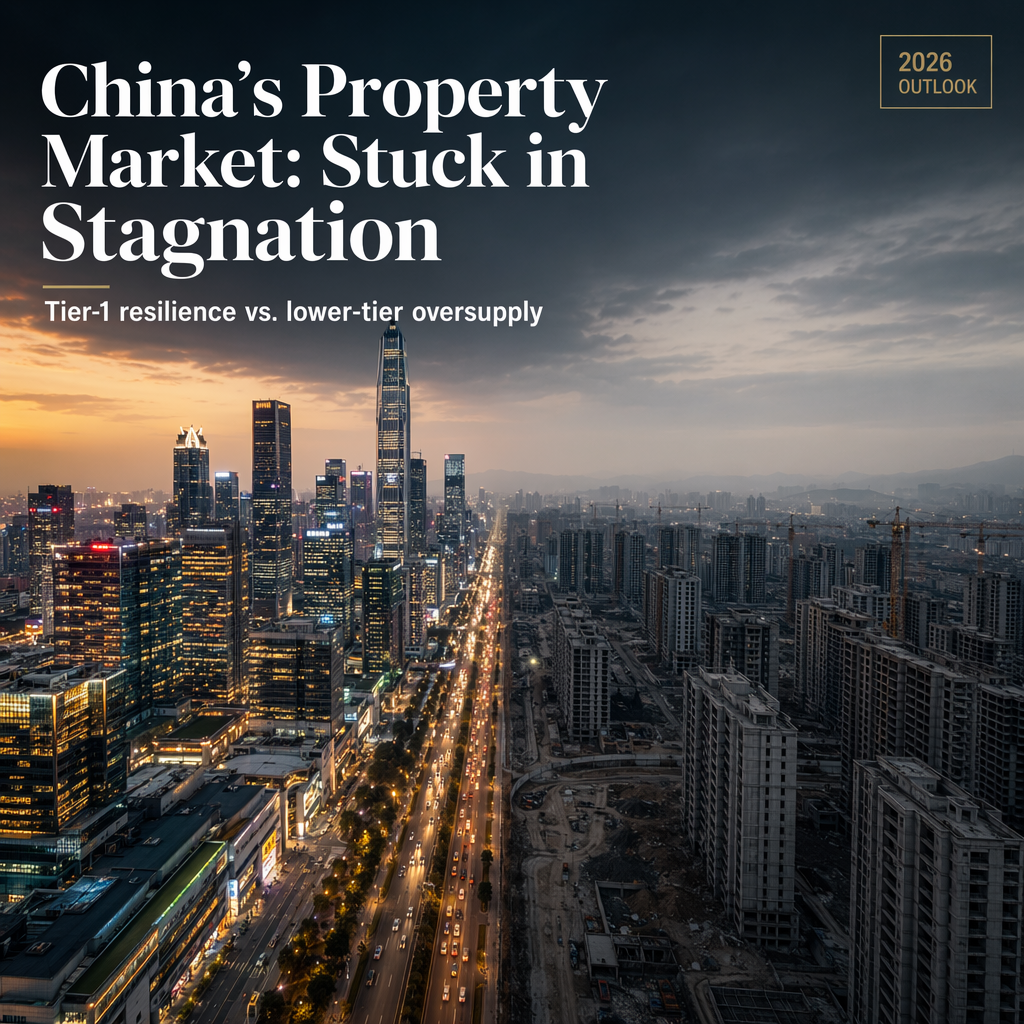

Commerzbank’s Dr. Henry Hao reports that China’s housing downturn, now in its fifth year, is showing no signs of a broad-based recovery and is instead settling into an L-shaped stagnation pattern with a pronounced K-shaped regional divergence [1]. The analysis highlights that while some localized stabilization has occurred in Tier-1 cities, with average absorption periods for excess supply falling to 21 months in Tier-1 and 27 months in Tier-2 cities as of May 2026, lower-tier cities remain heavily burdened by tens of millions of unsold units and an average absorption period of about 84 months, or roughly seven years [1].

Key data points from the first half of 2026 reveal that total funds available to real estate developers contracted by 18% year-on-year, primarily due to a sharp decline in pre-sales and mortgage revenue as buyers retreat from the market [1]. New construction starts have plummeted to just 24% of their July 2021 level, which is described as the most forward-looking indicator of developer sentiment [1].

The report underscores that structural headwinds, including demographic trends and policy constraints, are likely to keep China’s real estate sector as a drag on economic growth for years to come [1]. Despite some analysts interpreting the stabilization in top-tier cities as a sign of recovery, Commerzbank maintains a more pessimistic outlook, emphasizing that the market is settling into a permanent, downsized baseline [1].

No specific market reactions or analyst opinions regarding immediate market impact are mentioned, but the overall tone suggests significant ongoing challenges for the sector and the broader Chinese economy [1].

CONCLUSION

China’s real estate sector is entrenched in a prolonged period of stagnation, with only limited stabilization in top-tier cities and severe oversupply in lower-tier regions. Persistent funding constraints and a collapse in new construction starts point to continued weakness, making the sector a long-term drag on growth. The outlook remains negative, with no clear inflection point in sight.