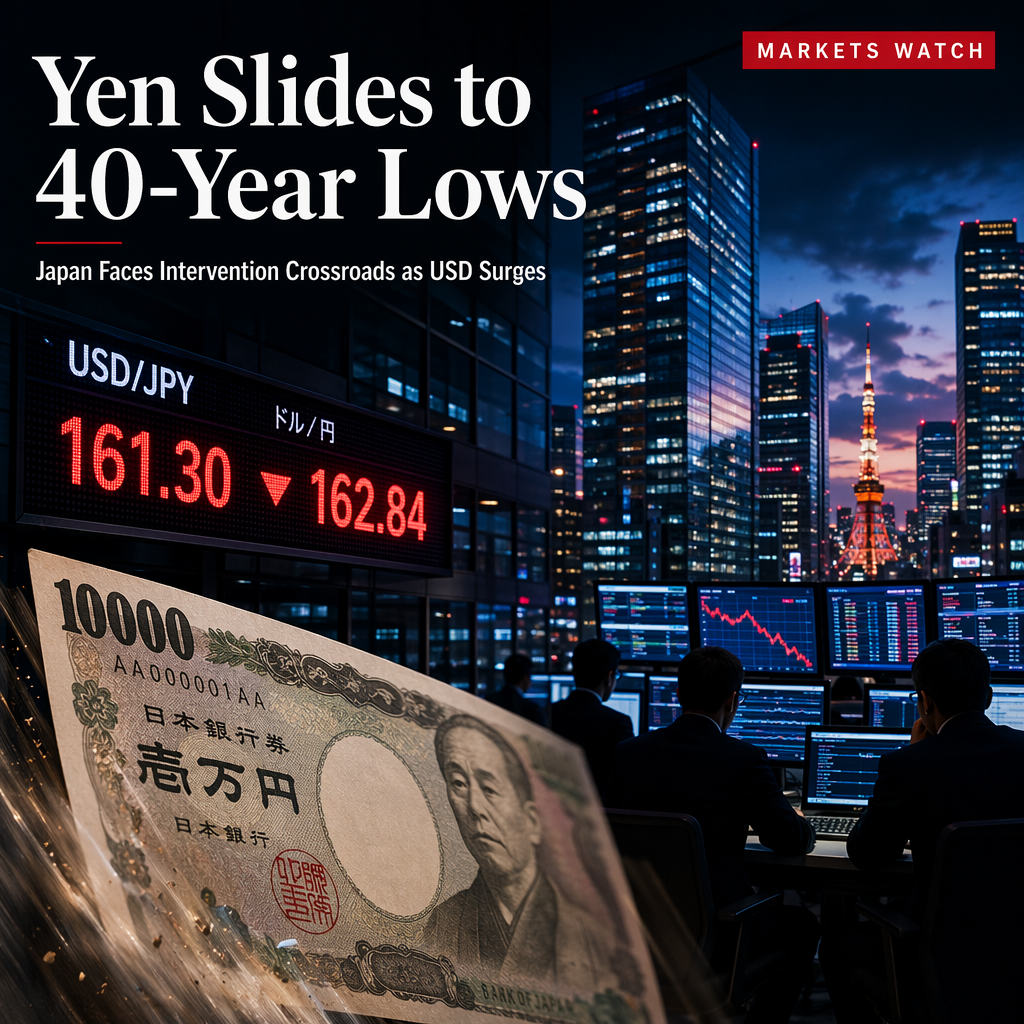

The Japanese Yen (JPY) has resumed its broader downtrend against the US Dollar (USD), with the USD/JPY pair appreciating nearly 0.6% on the day and reaching session highs around 161.30, approaching the 40-year high of 162.84. This decline in the Yen comes amid increasing risks of intervention by Japanese authorities, as the currency trades near historic lows and market participants grow wary of potential action from Tokyo to curb further depreciation [1].

HSBC strategists note that the USD/JPY pair is trading near its highest level in approximately 40 years and may have shifted into a new, higher trading range. They anticipate continued USD strength versus JPY through mid-2027, provided that wide US-Japan rate differentials persist and the Ministry of Finance (MoF) only intervenes selectively to address excessive Yen weakness. HSBC's outlook is based on the expectation that the Bank of Japan (BoJ) will avoid rapid, hawkish rate hikes, which would keep nominal and real US-Japan rate differentials wide. Additionally, fiscal concerns are expected to persist as Japanese authorities use fiscal policy to address cost of living pressures, boost investment, and strengthen defense [2].

Market sources, including Reuters, suggest that Japanese authorities might have opted to intervene without prior warnings to maximize the impact and squeeze speculators, though official communication has been notably muted. This unusual silence has led to speculation about a possible change in intervention tactics [1]. HSBC strategists also highlight that the MoF typically aims to surprise the market, with past intervention waves occurring at incrementally higher levels, as seen in 1998, 2022, and 2024 [2].

Analyst opinions diverge on the effectiveness and likelihood of intervention. MUFG’s Lee Hardman suggests that the market is underpricing the hawkish stance of the BoJ, noting that the ongoing steepening of the Japanese yield curve contrasts with flatter curves in the US, UK, and Germany. This, combined with a weaker Yen and rising long-term Japanese Government Bond (JGB) yields, reflects renewed fiscal concerns and perceptions that the BoJ remains behind the curve in tightening monetary policy [1]. HSBC, meanwhile, sees several reasons for a higher threshold for intervention, including lower oil prices reducing the urgency to curb imported inflation and the unpopularity of a weaker Yen with the Japanese public, which raises the risk of renewed 'triple sell' episodes across JPY, equities, and bonds [2].

CONCLUSION

The Japanese Yen's slide to near 40-year lows against the US Dollar has heightened intervention risks, with both market participants and analysts closely watching Japanese authorities' next moves. While some expect selective intervention and persistent fiscal concerns, others highlight the potential for surprise actions. The market impact remains high as the Yen's trajectory continues to be shaped by policy divergence and intervention speculation.