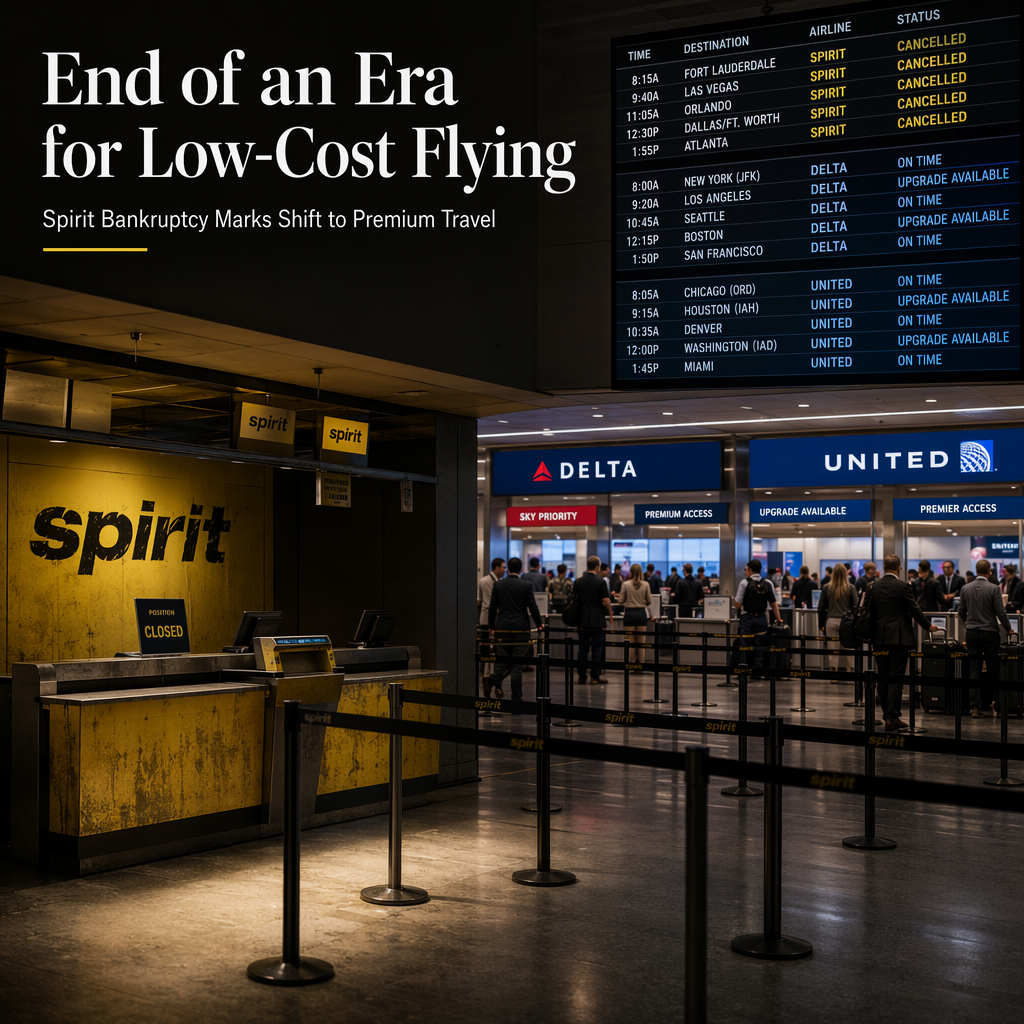

The U.S. budget airline sector is facing significant challenges, highlighted by the recent bankruptcy of Spirit Airlines. While carriers such as Breeze Airways, Frontier, and Avelo may benefit from Spirit's exit, the overall low-cost airline model is under considerable stress in the U.S. market, with factors beyond jet fuel prices contributing to the difficulties [1]. Major airlines like Delta Air Lines and United Airlines have leveraged their scale, loyalty programs, and premium service offerings to outcompete low-cost upstarts, as traveler preferences have shifted from prioritizing low fares to seeking premium cabins and services [1].

Unlike Europe, the U.S. market presents unique challenges for low-cost carriers, including longer routes that make profitability difficult for these airlines [1]. With Spirit Airlines no longer operating, travelers have fewer low-cost options, especially during the busy summer travel season, and this reduction in choice may become a permanent feature of the market [1]. According to Kyle Potter, editor of Thrifty Traveler, Spirit's demise marks the beginning of a new era in U.S. aviation, potentially signaling a return to a 'Golden Age' of travel that may not favor everyday flyers seeking low fares [1].

Recent financial results from leading carriers support this trend. Delta Air Lines reported a record annual revenue of $58.3 billion for 2025, despite selling $1.1 billion less in economy tickets compared to the previous year. The shortfall was offset by increased premium ticket sales, with 60% of Delta's total revenue now derived from higher-margin segments such as premium cabins, loyalty programs, and cargo [1]. Delta CEO Ed Bastian described a bifurcation in the market, with the fastest-growing demand segment being the premium sector, while lower-end consumers are struggling [1]. United Airlines also reported strong results, with $3.5 billion in adjusted net profit for 2025 (up 6%) and an 11% increase in premium seat revenue for the year. Despite geopolitical uncertainties, United noted that demand remains robust, driven by less price-sensitive customers [1].

Overall, the market is witnessing a decisive shift away from the ultra-low-cost carrier model, with major airlines capitalizing on premium offerings and loyalty programs to drive growth, while budget carriers face mounting headwinds [1].

CONCLUSION

The bankruptcy of Spirit Airlines underscores a fundamental shift in the U.S. airline industry, with major carriers focusing on premium services and loyalty programs as traveler preferences evolve. As low-cost options dwindle, the market is likely to see continued dominance by established airlines catering to higher-end demand. This transition may result in fewer affordable choices for price-sensitive travelers.