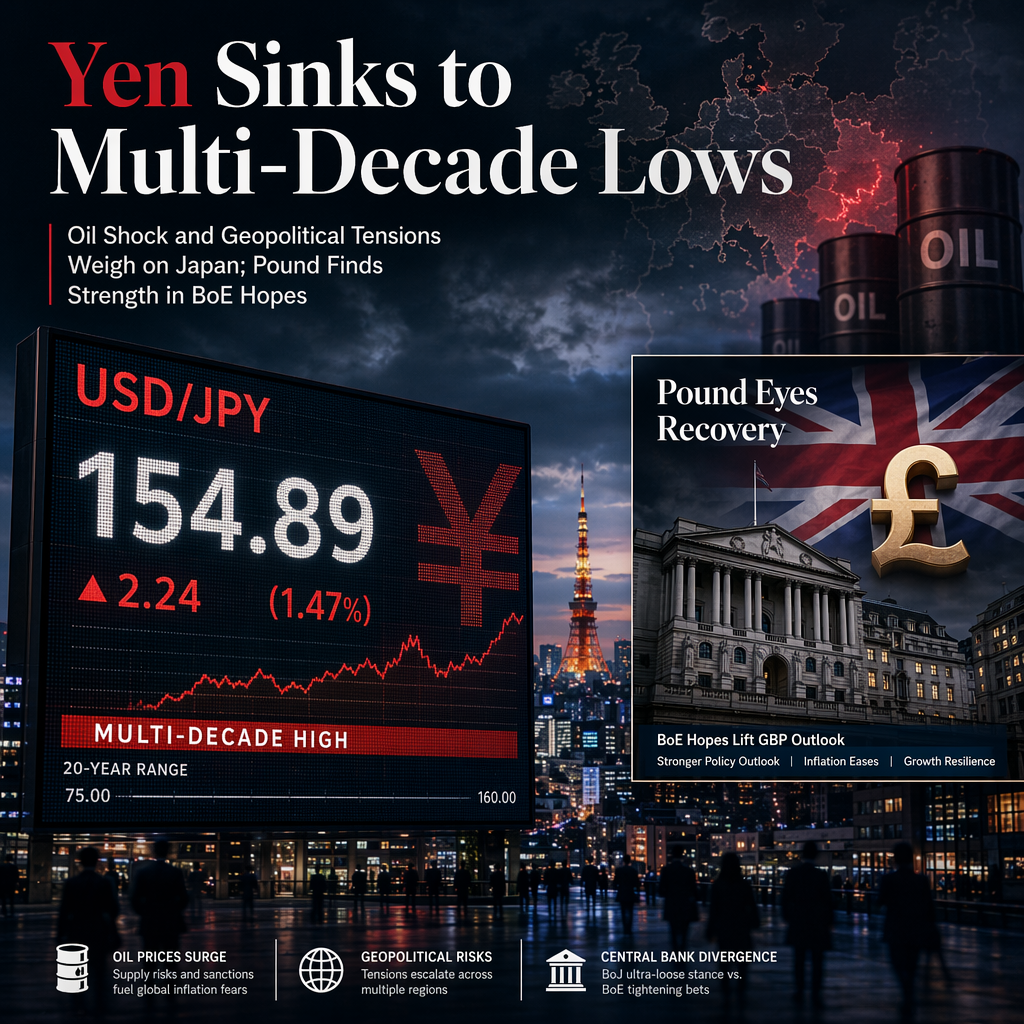

Scotiabank strategists report renewed weakness in the Japanese Yen (JPY), which is underperforming most G10 currencies and is down 0.2% against the US Dollar (USD) as of Wednesday’s North American session. The USD/JPY pair is trading at levels last seen in 1986, threatening to break to fresh multi-decade lows. The strategists attribute this softness to surging oil prices, which are negatively impacting Japan’s terms of trade, and note that the recent resurgence in geopolitical tensions presents a clear downside risk for the yen. The technical outlook offers little clarity, as the recent rally has pushed USD/JPY to uncharted territory with no obvious resistance levels in sight [1].

In contrast, the British Pound (GBP) is described as slightly softer, down 0.1% versus the USD, but is supported by a sharp repricing of Bank of England (BoE) tightening expectations. The recovery in UK-US spreads and positive sentiment around the UK leadership transition are providing fundamental and sentiment-related support to the GBP. Technically, the GBP’s recent recovery from the mid-1.31s in late June has stalled around 1.34, with resistance at the 50 and 200 day moving averages. However, Scotiabank strategists remain bullish, targeting an extension of GBP gains toward 1.36, with a near-term range expected between 1.3300 and 1.3400 [2].

The articles highlight diverging fortunes for the JPY and GBP, with the yen facing significant downside risks from external shocks such as oil prices and geopolitical tensions, while the pound is buoyed by domestic monetary policy expectations and improving spreads. No specific market reactions or analyst opinions beyond those of the Scotiabank strategists are mentioned in the sources [1][2].

CONCLUSION

The Japanese Yen is under significant pressure due to surging oil prices and geopolitical tensions, threatening new multi-decade lows. Meanwhile, the British Pound is supported by BoE tightening expectations and positive sentiment, with strategists targeting further gains. Market participants should monitor these diverging trends as they reflect differing macroeconomic and policy drivers.