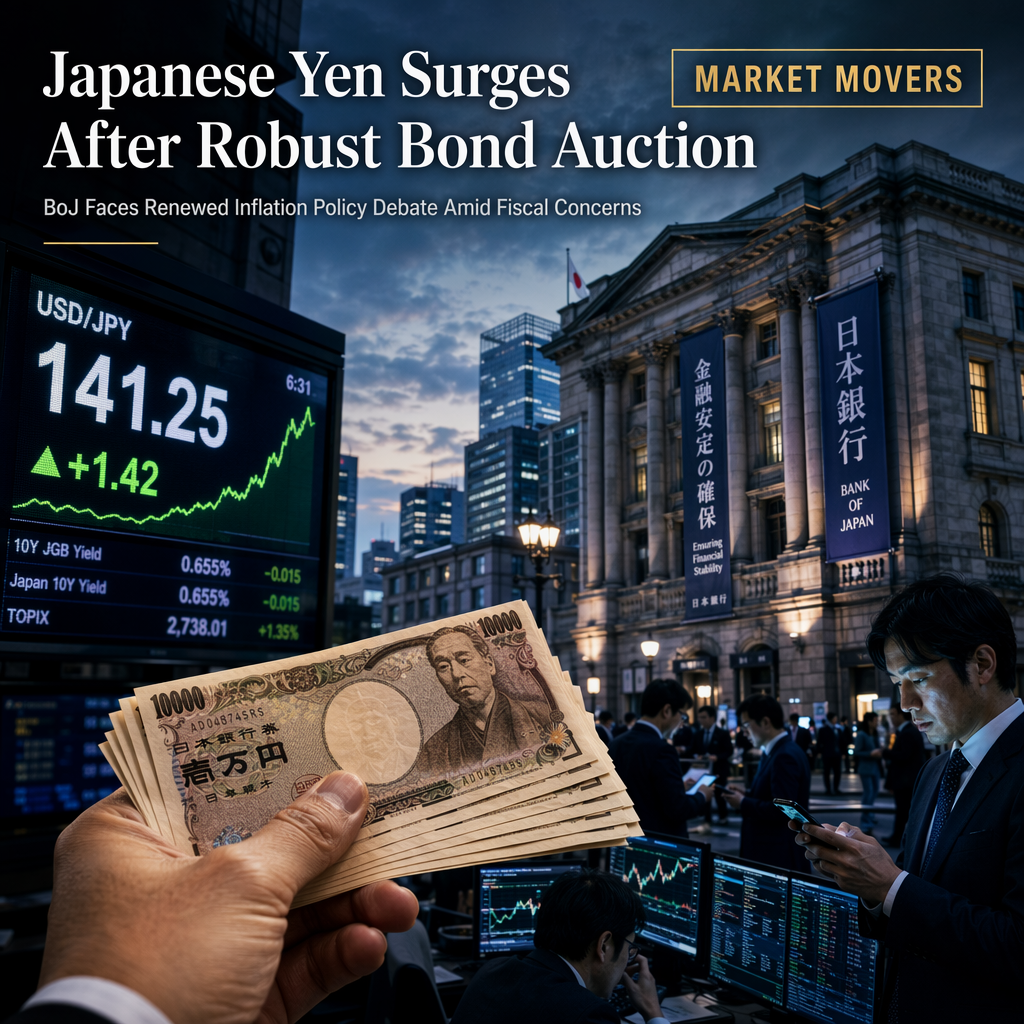

Rabobank’s Senior FX Strategist Jane Foley analyzed the recent performance of the Japanese Yen (JPY), noting that it is currently the best performing G10 currency on a one-day basis, despite being the worst performer over the past 12 months [1]. This shift follows a 30-year Japanese Government Bond (JGB) auction that achieved its highest bid cover ratio since 2019, suggesting that market participants may be less concerned about inflationary or fiscal risks in Japan [1].

Foley referenced comments from US Treasury Secretary Bessent in August of the previous year, who stated that the Bank of Japan (BoJ) was 'behind the curve on inflation' and anticipated rate hikes. Bessent also warned that higher JGB yields could influence yields in other bond markets, including US Treasuries, due to Japanese investors' significant holdings of US debt [1].

Despite the recent JPY strength and robust JGB auction, Foley emphasized that fiscal concerns and the BoJ’s cautious approach to rate hikes continue to limit the potential for a sustained JPY recovery. She highlighted that core-core CPI inflation was at a moderate 1.8% year-on-year in May, with various inflation measures having dropped significantly from last year’s highs. This data suggests that accusations of the BoJ being behind the curve may be overstated [1].

Foley concluded that while a faster pace of BoJ rate hikes would support the JPY, investor concerns about fiscal policy remain. She indicated that more reassuring fiscal messages are needed before the JPY can achieve a convincing turnaround [1].

CONCLUSION

The Japanese Yen has shown notable short-term strength, supported by a strong JGB auction and moderating inflation data. However, ongoing fiscal concerns and the BoJ’s cautious policy stance suggest that a sustained JPY recovery will require further clarity and confidence in Japan’s fiscal outlook.