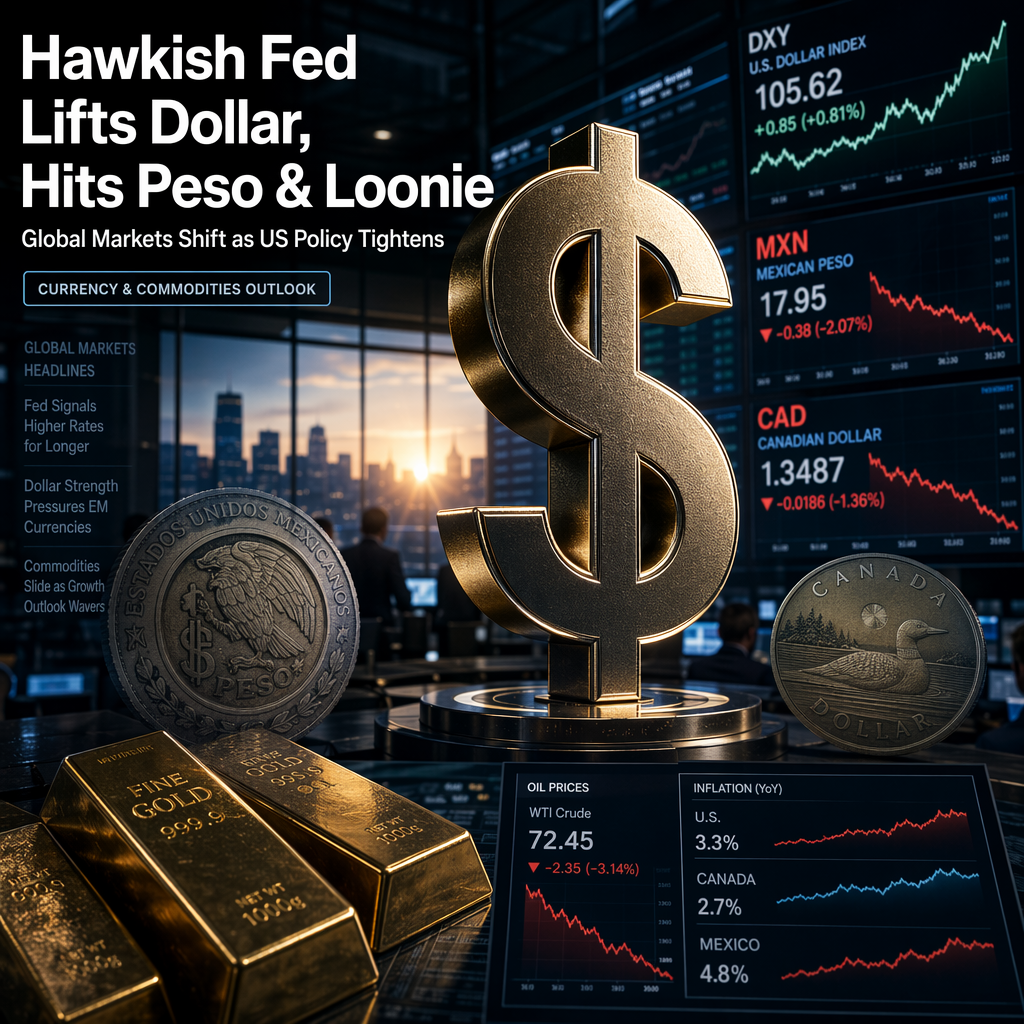

The US Dollar strengthened on Monday, driven by a hawkish tilt from the Federal Reserve, which led to notable currency market movements. The Mexican Peso weakened by 0.34% against the US Dollar, with USD/MXN trading at 17.35 after rebounding from daily lows of 17.29. This move was underpinned by expectations that the interest rate differential between the US and Mexico could narrow in the near term, as nine out of 19 FOMC members anticipate a rate hike this year, while eight favor holding rates steady and one supports a cut. The new Fed Chair, Kevin Warsh, did not express a policy view. The US Dollar Index (DXY) rose 0.22% to 100.98, nearing 12-month highs [1].

In Mexico, the Bank of Mexico (Banxico) is expected to keep rates unchanged at 6.50% at its June 25 meeting, with Deputy Governor Gabriel Cuadra confirming the end of the easing cycle and the need for stable rates due to a complex outlook. Mexican inflation appears steady, with CPI projected at 3.77% YoY and Core CPI expected to ease slightly to 4.14% YoY, according to a Reuters poll [1].

The Canadian Dollar also faced significant pressure, sliding to fresh 14-month lows as USD/CAD reached a session high near 1.4200 before easing to 1.4150. Despite a hot May inflation print—headline CPI accelerated to 3.2% YoY, above the 3.0% consensus and up from 2.8% previously—and a rebound in crude oil prices, the Loonie remained the weakest major currency. The traditional correlation between oil prices and the Canadian Dollar has broken down, as higher energy prices are now seen as a stagflationary tax rather than a benefit. The hawkish Fed stance and ongoing US-Canada trade tensions, including tariffs and unresolved trade pact issues, have left Canadian growth stalling, with output contracting slightly in Q1. This has created a policy dilemma for the Bank of Canada, as hiking rates could risk recession while standing pat may let inflation expectations drift [2].

Meanwhile, gold prices (XAU/USD) posted modest gains of 0.50% to $4,179, buoyed by lower oil prices and reduced inflation expectations following positive US-Iran talks. West Texas Intermediate (WTI) oil fell 2.40% to $73.67. The market is pricing in a nearly 90% chance of a Fed rate hike in December, with some banks forecasting multiple hikes in 2026. Money markets see a 45% chance of a rate hike at the July 29 Fed meeting. Despite the bullish day, gold remains in a broader downtrend, with technical resistance at $4,200 and further upside likely to face selling pressure [3].

Across all sources, the dominant theme is the outsized influence of US monetary policy and geopolitical developments on global currency and commodity markets, with both the Mexican Peso and Canadian Dollar under pressure and gold benefiting from shifting inflation expectations.

CONCLUSION

A hawkish Federal Reserve and shifting global dynamics have strengthened the US Dollar, pressuring both the Mexican Peso and Canadian Dollar despite local economic data. Gold has seen modest gains as oil prices fall and inflation expectations ease. The market remains focused on upcoming US economic releases and central bank decisions, with further volatility likely as policy paths become clearer.