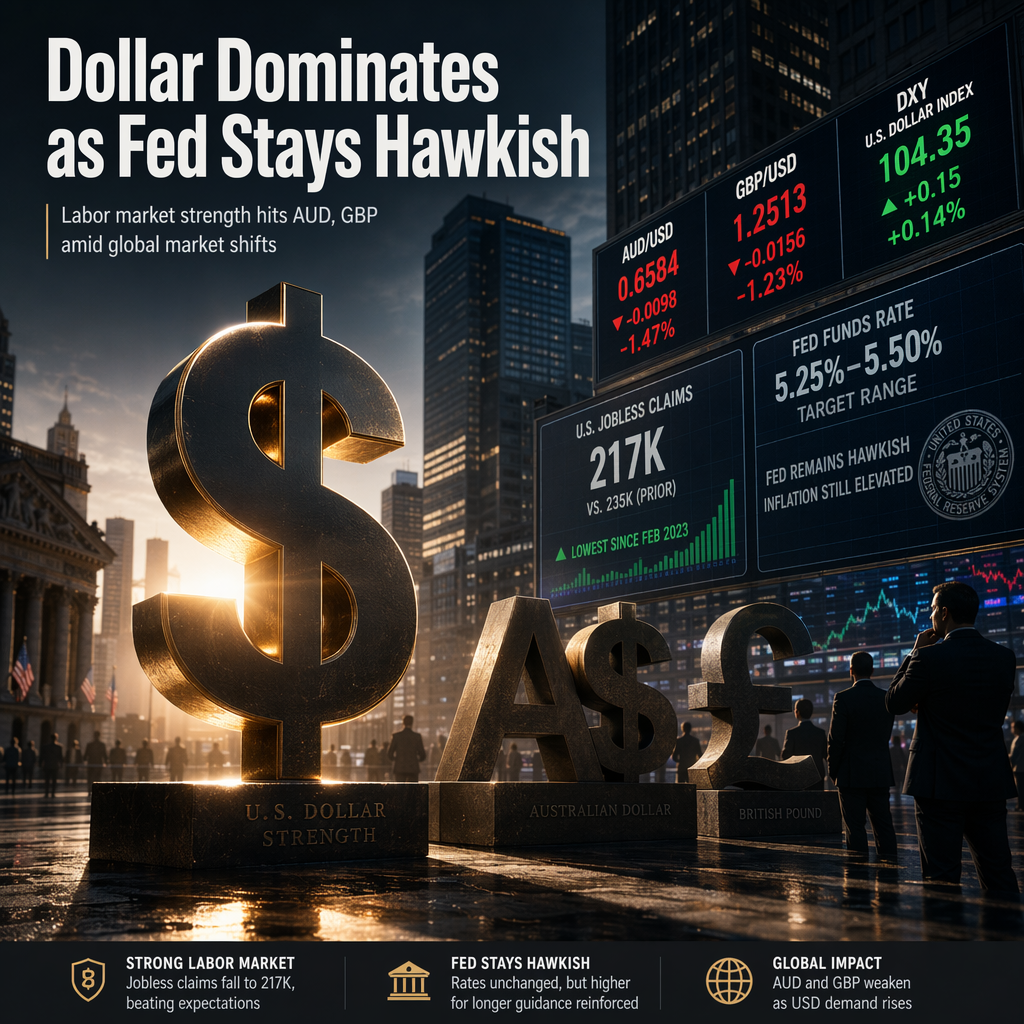

The US Dollar remained firm on Thursday, buoyed by resilient labor market data and a hawkish Federal Reserve policy stance, which impacted both the Australian Dollar (AUD) and the British Pound (GBP) [1][2]. US Initial Jobless Claims fell by 4,000 to 226,000 for the week ending June 13, close to market expectations of 225,000, indicating limited layoffs and ongoing labor market resilience, despite slower hiring momentum [1][2]. Continuing Jobless Claims rose to 1.81 million, slightly above consensus [1].

The Federal Reserve decided to keep interest rates unchanged in the 3.50%-3.75% range, with Chair Kevin Warsh emphasizing the need for greater confidence that inflation is moving toward the 2% target before considering a looser policy stance [1][2]. According to the FOMC's updated projections, 9 out of 19 members expect at least one rate hike in 2026, 7 expect rates to remain steady, and 1 expects a rate cut. The median forecast among policymakers sees inflation ending at 3.6% in 2026 and reaching the 2% goal in 2028, with GDP growth now projected at 2.2% by year-end and the unemployment rate holding steady [2]. Markets are pricing in 36 basis points of tightening by the end of 2026 [2].

The AUD/USD pair traded in a muted range near 0.7030, with the Australian Dollar struggling to extend gains as the US Dollar remained supported by the labor market data and Fed policy [1]. Improved risk sentiment, following a deal between US President Donald Trump and Iran's leader to end the Middle East war and reopen the Strait of Hormuz, provided some support to the Aussie [1]. Technical analysis shows AUD/USD at 0.7031, maintaining a bearish near-term bias below key moving averages, with immediate resistance at 0.7041 and support at 0.7018 [1].

Meanwhile, the GBP/USD pair dropped to 1.3234, down 0.39% and at its lowest level since April 7, as the Fed's hawkish tilt overshadowed the Bank of England's decision to hold rates at 3.75% in a 7-2 vote [2]. The US Dollar Index (DXY) traded at 100.63, just below its year-to-date peak of 100.81, while WTI crude oil fell 2.20% to $73.27 per barrel [2]. In the UK, solid jobs data showed an increase of 100,000 in the workforce and wage growth rising to 3.4% in the three months to April, but political developments and speculation around the UK elections also influenced market sentiment [2].

CONCLUSION

The US Dollar's strength, driven by resilient labor data and a hawkish Fed, weighed on both the Australian Dollar and British Pound, despite supportive risk sentiment and solid UK jobs data. Market participants are closely watching Fed policy signals and upcoming economic data for further direction. The overall market impact is high, with currency pairs reacting to both central bank decisions and geopolitical developments.