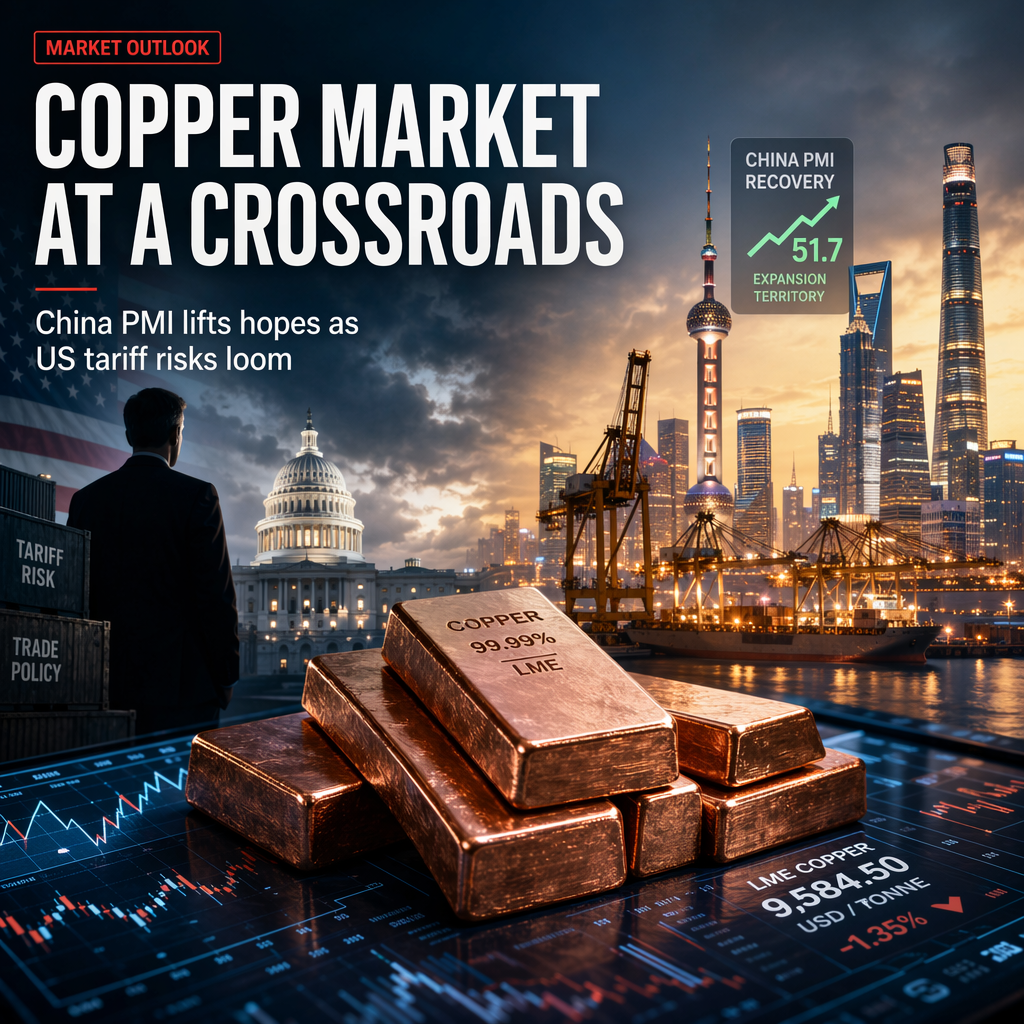

Commerzbank’s Barbara Lambrecht reports that the London Metal Exchange (LMEX) index continues to face downward pressure, despite a positive development in China’s manufacturing sector. The official Purchasing Managers’ Index (PMI) for China rose to 50.3 in June, marking a positive surprise and indicating expansion. This improvement is attributed to export-driven industrial activities, particularly those boosted by the rapidly growing artificial intelligence segment worldwide [1].

A key event highlighted is the deadline for the US Secretary of Commerce Lutnick’s report on the possible introduction of a 15% tariff on refined copper. If the tariff is recommended and US President Trump announces its implementation starting January 1, 2027, it could trigger a surge in US copper demand in the second half of the year, as buyers seek to stockpile ahead of the tariff. The tariff rate could potentially increase to 30% in 2028, further intensifying market activity [1].

Alternatively, if President Trump decides to forgo or postpone the tariffs, citing concerns about the scarcity of US copper supply raised by domestic companies, material could be drawn from COMEX stocks, providing some initial relief to the market. However, a postponement of the decision is expected to have minimal impact on market dynamics [1].

Overall, the copper market is navigating a complex landscape shaped by improving Chinese demand and looming US tariff risks. The outcome of the tariff decision will play a crucial role in determining near-term market movements, with potential for increased volatility depending on the policy direction [1].

CONCLUSION

The copper market is currently influenced by a recovering Chinese manufacturing sector and uncertainty surrounding potential US tariffs. While positive PMI data from China offers support, the US tariff decision remains a pivotal factor for future demand and price movements. Market participants are closely watching for policy announcements that could drive significant shifts in copper trading.