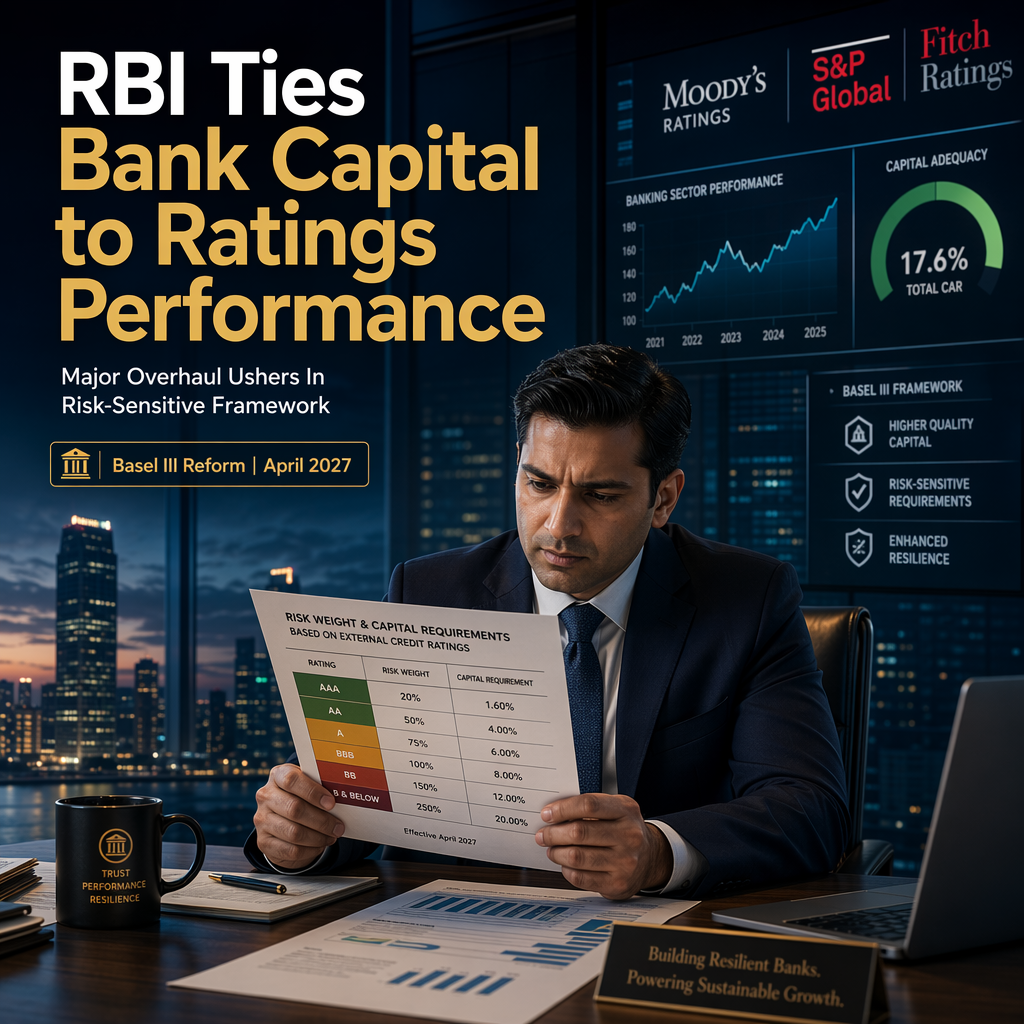

The Reserve Bank of India (RBI) has announced a significant overhaul of its credit-risk capital framework, as explained by Societe Generale economist Kunal Kundu. Starting from April 2027, the revised Standardised Approach will link regulatory risk weights not only to the borrower's rating grade but also to the historical default performance of the rating agency that assigned the rating [1]. This reform is designed to enhance the risk sensitivity of capital requirements, making them more robust and comparable, while also reducing mechanical reliance on external ratings [1].

The new framework aims to align India's credit-risk capital rules with the Basel III final reforms, addressing a broad range of exposures including corporates, MSMEs, real estate, retail, off-balance-sheet items, and external credit assessments [1]. Previously, rating grades such as AA, A, or BBB were treated as broadly equivalent across eligible agencies, but the new system introduces differentiation based on the track record of each rating agency [1].

According to Kundu, this is a major reform in India's credit-risk capital architecture. The changes are expected to curb rating shopping and force banks to upgrade their internal credit assessment and capital management practices [1]. No specific market reactions or analyst forecasts are provided in the source article.

CONCLUSION

The RBI's overhaul of credit-risk capital rules marks a major shift towards a more risk-sensitive and robust framework. By tying capital requirements to both borrower ratings and rating agency performance, the reform is expected to improve credit assessment practices and align India with global standards.