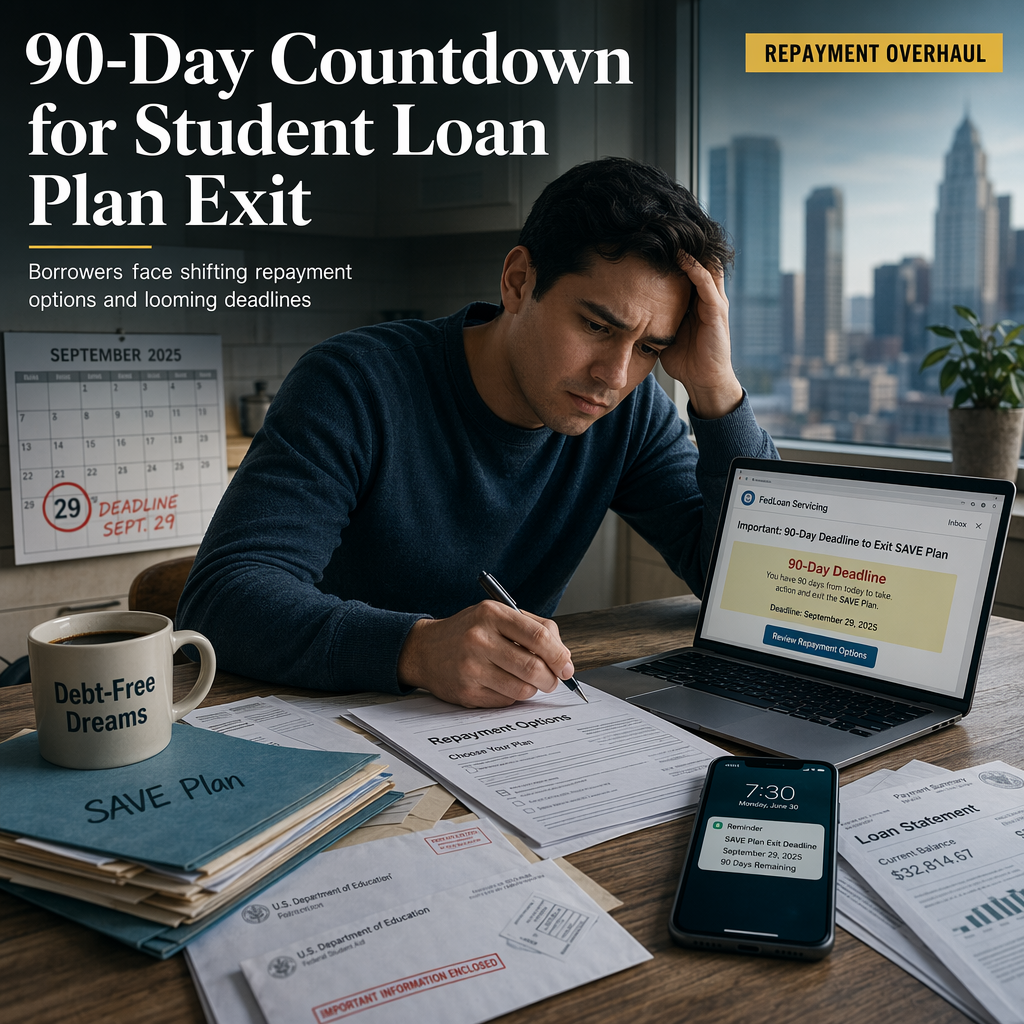

Federal student loan servicers have started notifying borrowers enrolled in the Biden-era SAVE plan that they have 90 days to exit the program, following significant changes to federal student loan repayment options that took effect on July 1 under President Donald Trump's 'one big beautiful bill act' [1]. As of March, more than 6.9 million borrowers remained in the SAVE plan, each carrying an average debt of nearly $55,000, according to higher education expert Mark Kantrowitz [1]. This marks a decrease from approximately 7.7 million borrowers a year ago, indicating a slow transition out of the plan [1].

The U.S. Department of Education stated in a June 25 court filing that the earliest deadline to exit SAVE is September 29, but most borrowers will have more time, with notifications being sent in waves between July 2026 and March 2027 [1]. Loan servicers will inform borrowers of their specific deadlines, and there is no universal exit date, which has caused confusion among borrowers after years of policy changes, according to Will Sealy, CEO of Summer [1]. Borrowers are encouraged to proactively switch plans without waiting for official notices, as emphasized by Nancy Nierman of the Education Debt Consumer Assistance Program [1].

If borrowers do not select a new repayment plan within 90 days of notification, they will be automatically placed in either the Standard Repayment Plan or the new Tiered Standard Plan, both of which began on July 1 [1]. Sealy warns that the Standard Plan is typically the most expensive option, and urges borrowers to assess their options and enroll in a new plan before their exit deadline [1]. However, borrowers who miss the deadline can still apply for an income-driven repayment (IDR) plan later, which caps monthly payments based on income [1].

The transition represents a significant shift in federal student loan policy, with the potential for increased financial strain on borrowers who do not act promptly. The lack of a universal deadline and the complexity of the new repayment landscape may lead to confusion and possible negative financial outcomes for some borrowers [1].

CONCLUSION

The mandated exit from the SAVE plan and the introduction of new repayment options mark a major change for millions of federal student loan borrowers. With deadlines varying and the risk of being placed in more expensive plans, timely action is crucial. The market impact is medium, as the changes could affect consumer spending and financial stability for a significant borrower segment.