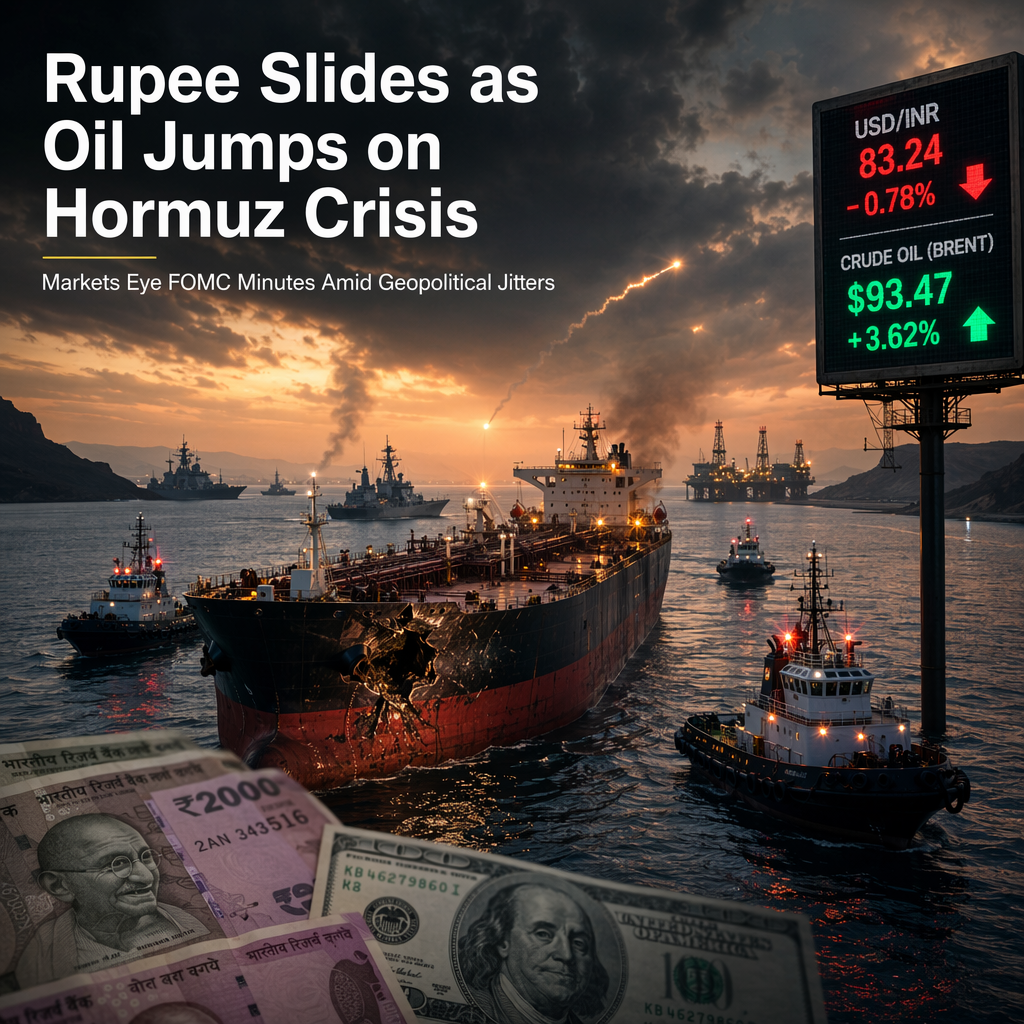

The Indian Rupee (INR) continued to hold onto losses against the US Dollar (USD) in Tuesday's opening session, with the USD/INR pair trading near 95.36. This movement was attributed to renewed fears of energy supply disruption after Iran fired at least two missiles at commercial ships transiting the Strait of Hormuz, a passage critical for nearly 20% of global energy supply. Two ships were hit and suffered significant damage, though no casualties were reported. The MCX Crude Oil contract expiring July 20 rose 0.66% to near 6,600, reflecting the uptick in oil prices that typically weighs on currencies of oil-importing nations like India [1].

The US Dollar Index (DXY) remained below the 101.00 mark, extending its consolidative moves for a third straight day. While the US-Iran standoff and rising tensions in the Strait of Hormuz provided some safe-haven support to the USD, receding Federal Reserve rate hike expectations limited aggressive USD buying. Traders shifted their expectations from one to two Fed rate increases in 2026 to between zero and one hike after a soft US Nonfarm Payrolls report for June. Additionally, the US ISM Services PMI eased to 54.0 in June from 54.5 in May, matching consensus estimates and offering little support to the USD [2].

Foreign Institutional Investors (FIIs) were net buyers in the Indian stock market for the second consecutive day on Monday, investing Rs. 243.03 crore, though this was significantly lower than the Rs. 1,355.33 crore invested on Friday. The return of oil prices to pre-Middle East war levels has improved overseas investor sentiment toward Indian equities. However, future FII flows are expected to be influenced by upcoming corporate earnings, with Tata Consultancy Services (TCS) set to release its Q1FY27 results on Thursday [1].

Both articles highlight that market participants are closely watching the release of the Federal Open Market Committee (FOMC) minutes on Wednesday. The minutes are expected to provide clarity on the Fed's policy outlook, especially after officials refrained from giving forward guidance in the recent meeting. The Fed previously left rates unchanged at 3.50%-3.75%, with nine of 19 policymakers favoring a hike by year-end. The CME FedWatch tool currently shows a 55.2% probability of at least one rate hike by September [1].

CONCLUSION

Geopolitical tensions in the Strait of Hormuz have driven oil prices higher, pressuring the Indian Rupee and supporting the US Dollar, though fading Fed rate hike expectations have capped USD gains. Investors are now focused on the upcoming FOMC minutes for further policy direction, while Indian equities await key earnings releases to guide foreign investment flows.