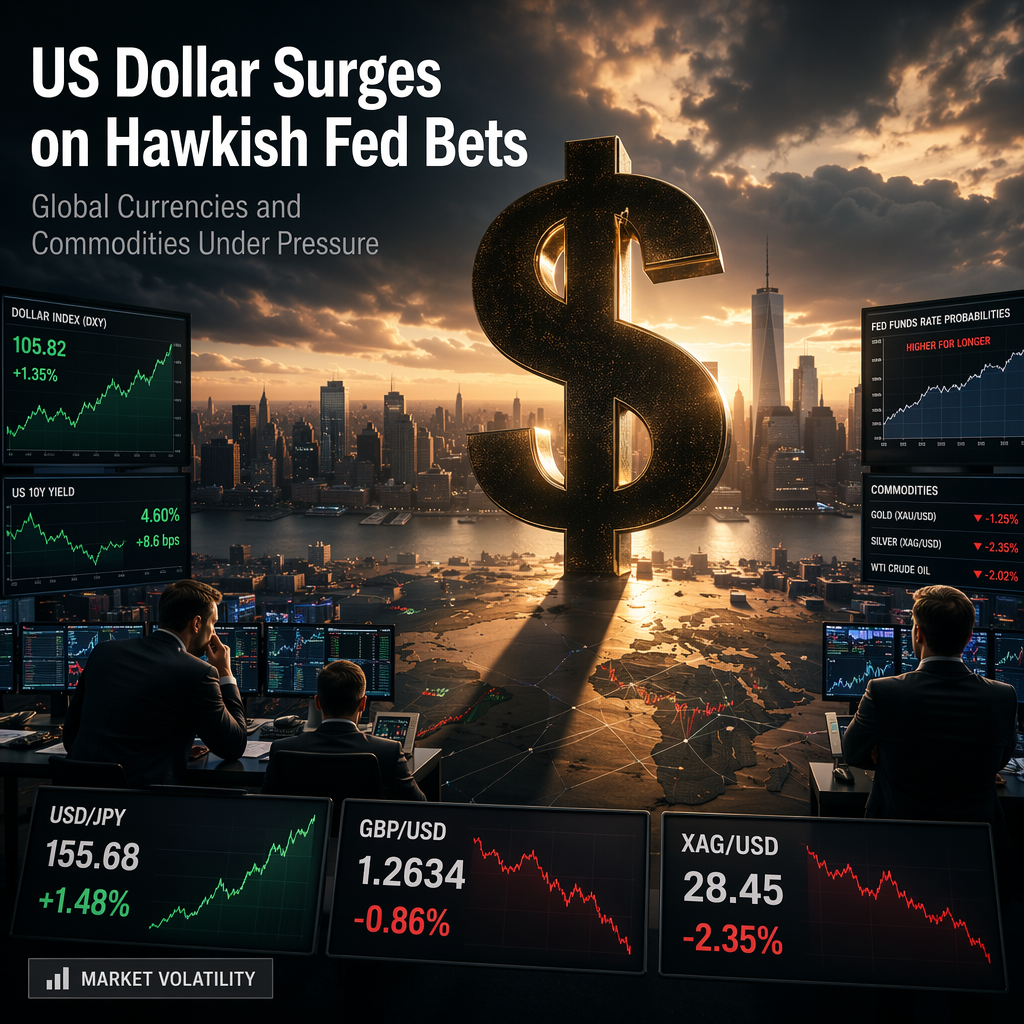

The US Dollar Index (DXY) reached its highest level in over a year, trading 0.1% higher near 101.50 during Wednesday's European session, as market participants priced in a more hawkish Federal Reserve stance across global markets [1][2][3][5]. According to the CME FedWatch tool, the probability of a Fed rate hike this year stands at nearly 86%, with a 48.3% chance of at least two hikes, a sharp reversal from earlier expectations of cuts before the Middle East conflict increased inflationary pressures [2][3][5]. The latest US Consumer Price Index (CPI) showed core inflation accelerating to 2.9% in May, the highest in seven months, while the upcoming US Personal Consumption Expenditure (PCE) Price Index for May is expected to show core inflation at 3.4% year-on-year, up from 3.3% previously [2][3][5].

This hawkish Fed outlook has had significant repercussions across major currency pairs and commodities. The USD/JPY pair consolidated in a tight range around 161.60, supported by hawkish Bank of Japan (BoJ) sentiment, as the BoJ's June Summary of Opinions revealed most officials favor further rate hikes to counter inflation risks. The BoJ recently raised rates by 25 basis points to 1%, and a Reuters report suggests another hike is likely in December. However, new board member Toichiro Asada voted against the hike, citing downside risks from the Middle East crisis [1]. Technical analysis indicates USD/JPY maintains a bullish bias above key support levels, with upside momentum intact [1].

The Indian Rupee (INR) weakened against the US Dollar, with USD/INR rising to near 94.85, as the strong dollar and hawkish Fed bets outweighed the positive impact of lower oil prices. Oil prices fell to a three-month low, with the MCX Crude Oil contract down 0.7% to near 6,900, as traffic through the Strait of Hormuz normalized. Despite this, foreign institutional investor flows into Indian equities remained subdued, with only Rs. 17.86 crore in net buying on Tuesday compared to Rs. 635.91 crore in net selling on Monday [2].

Silver (XAG/USD) posted a fresh six-month low at $60.74, pressured by the stronger dollar and expectations of higher US rates. Technicals show persistent downside momentum, with the price well below the 20-day EMA and the RSI near oversold territory. Further declines toward $56.47 or even $50.00 are possible if support levels break [3].

Elsewhere, the AUD/JPY cross weakened below 112.00 amid intervention fears from Japanese authorities and a softer-than-expected Australian CPI print (4.0% YoY in May vs. 4.2% prior and 4.4% expected). Technicals point to a bearish bias as the pair trades below the 100-day SMA, with momentum edging toward oversold [4].

The British Pound (GBP/USD) extended its decline below 1.3200, pressured by UK political instability following Keir Starmer's resignation as Prime Minister and weak economic data. The UK flash Composite PMI fell to a 14-month low of 49.4 in June, indicating contraction. Market focus remains on the new Labour leadership and potential changes to fiscal policy, with analysts warning that any relaxation of fiscal rules could further weigh on the pound. The dollar's strength is attributed to the high probability of a Fed hike, with traders now pricing in an 86.1% chance of a December increase, up from 61% before the last FOMC meeting [5].

CONCLUSION

A surge in hawkish Fed expectations has propelled the US Dollar to new highs, pressuring major currencies and commodities globally. Market sentiment remains risk-off, with investors awaiting key US inflation data for further direction. The strong dollar and shifting central bank policies are likely to drive continued volatility across FX and commodity markets.