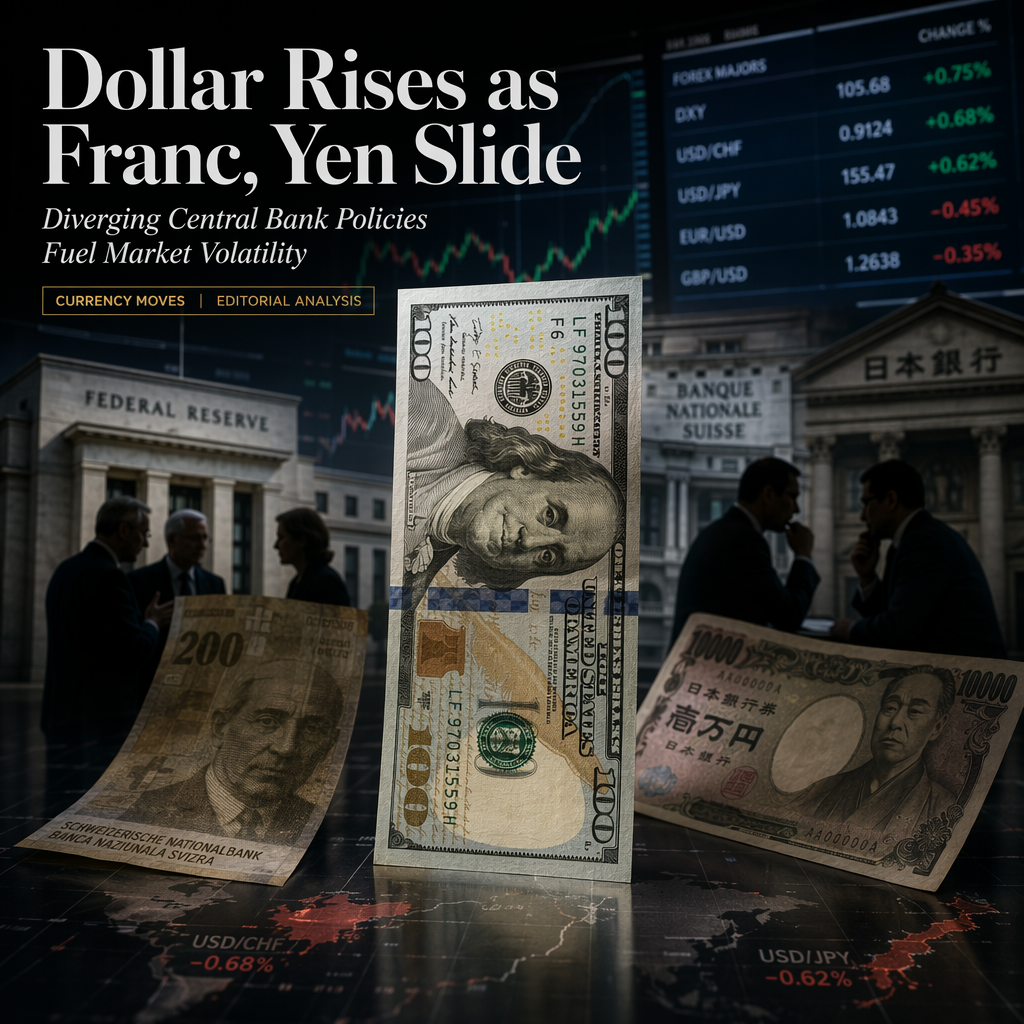

The US Dollar (USD) strengthened against both the Swiss Franc (CHF) and the Japanese Yen (JPY) on Monday, driven by renewed demand for the Greenback despite last week's weaker-than-expected US Nonfarm Payrolls (NFP) report [1][2]. The USD/CHF pair gained 0.37%, trading around 0.8060, as the Swiss Franc dipped following an unexpected rise in Switzerland's unemployment rate to 3.1% in June, up from 3% in May and above market expectations of 3% [1]. This deterioration in Swiss labor market conditions added further pressure on the CHF, supporting the USD/CHF pair [1].

Meanwhile, the USD/JPY pair rose 0.58% to trade around 162.30, moving back toward the nearly 40-year high of 162.84 reached the previous Wednesday [2]. The Japanese Yen remains under pressure due to the wide interest rate differential between the US and Japan, which continues to fuel carry trades at the expense of the JPY [2]. Although the Bank of Japan (BoJ) is gradually normalizing its monetary policy, its rates remain well below those of other major central banks, limiting support for the Yen [2].

Market participants are closely watching for potential intervention by Japanese authorities, as officials have reiterated their readiness to act against excessive foreign exchange moves, though no intervention has occurred so far [2]. MUFG analysts suggest that markets may be underestimating the BoJ's tightening potential, projecting the policy rate could reach 1.5% by January 2027, with the next rate hike expected in September [2]. HSBC, on the other hand, anticipates USD/JPY could remain elevated as long as the US-Japan rate differential persists, but expects selective intervention by Japan's Ministry of Finance to prevent excessive JPY depreciation [2].

On the US side, the ISM Services PMI eased slightly to 54 in June from 54.5 in May, matching market expectations, with softer New Orders and lower Prices Paid, while the Employment Index improved [1]. According to the CME FedWatch tool, markets are pricing in a 76.9% chance of additional Federal Reserve interest rate hikes by year-end, and investors are awaiting the release of the FOMC Minutes from the June policy meeting for further guidance [1].

Currency heat maps from both sources confirm that the Swiss Franc was weakest against the Japanese Yen, while the Japanese Yen was strongest against the Swiss Franc on the day [1][2].

CONCLUSION

The US Dollar's broad-based strength, supported by expectations of further Fed tightening and geopolitical tensions, has led to declines in both the Swiss Franc and Japanese Yen. Diverging central bank policies and labor market data are key drivers, with markets closely monitoring potential interventions and upcoming policy signals. The market impact is high, with continued volatility expected in USD/CHF and USD/JPY.