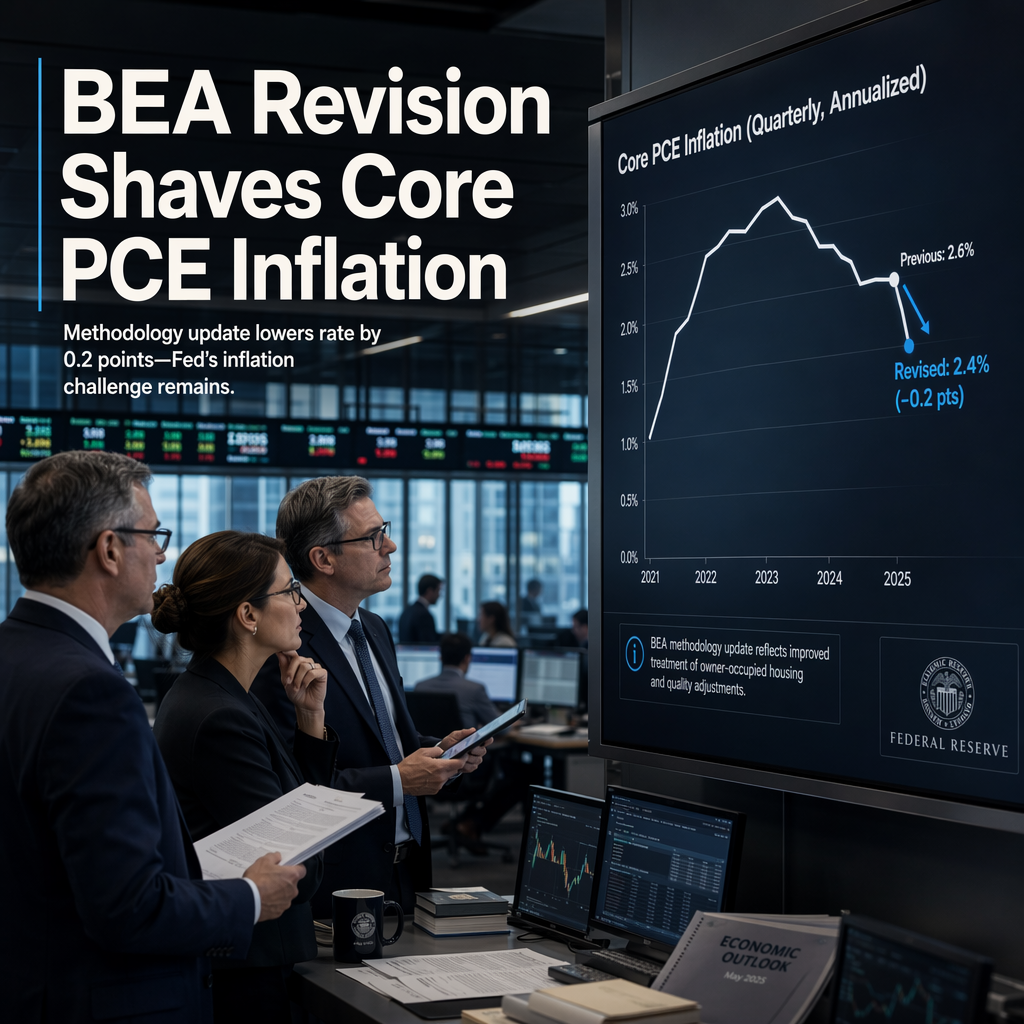

Wells Fargo economists Tom Porcelli and Sarah House have highlighted upcoming changes to the methodology used by the Bureau of Economic Analysis (BEA) for calculating the Personal Consumption Expenditures (PCE) Price Index, the Federal Reserve's preferred measure of inflation. These changes, set to be implemented in the BEA’s annual update on September 30, will affect data from 2021 onward and are expected to modestly lower the reported rate of core PCE inflation [1].

According to Wells Fargo, the new methodology will reduce the current year-over-year run-rate of core PCE by approximately 0.2 percentage points. For example, May’s core PCE inflation rate would be revised to around 3.2%, compared to the previously published 3.4%. Despite this adjustment, core PCE inflation will remain about 1 percentage point above the Federal Reserve’s 2% target, indicating that the changes do not resolve the central bank’s ongoing inflation challenges [1].

The economists emphasized that while the revision is significant relative to typical data adjustments, its overall impact on the inflation outlook is modest. They also noted that the methodology changes are not expected to consistently produce lower inflation readings or introduce a structural downward bias. Additionally, the update may complicate the process of mapping monthly PCE estimates after the release of Consumer Price Index (CPI) and Producer Price Index (PPI) data, as the new BEA composite index weightings will not be published and the price index for portfolio management and investment advice will no longer be observable from the monthly PPI report [1].

CONCLUSION

The BEA’s upcoming methodology changes will modestly lower reported core PCE inflation, but inflation will remain well above the Fed’s target. Market implications are limited, as the adjustment does not alter the broader inflation narrative or the challenges facing monetary policy.