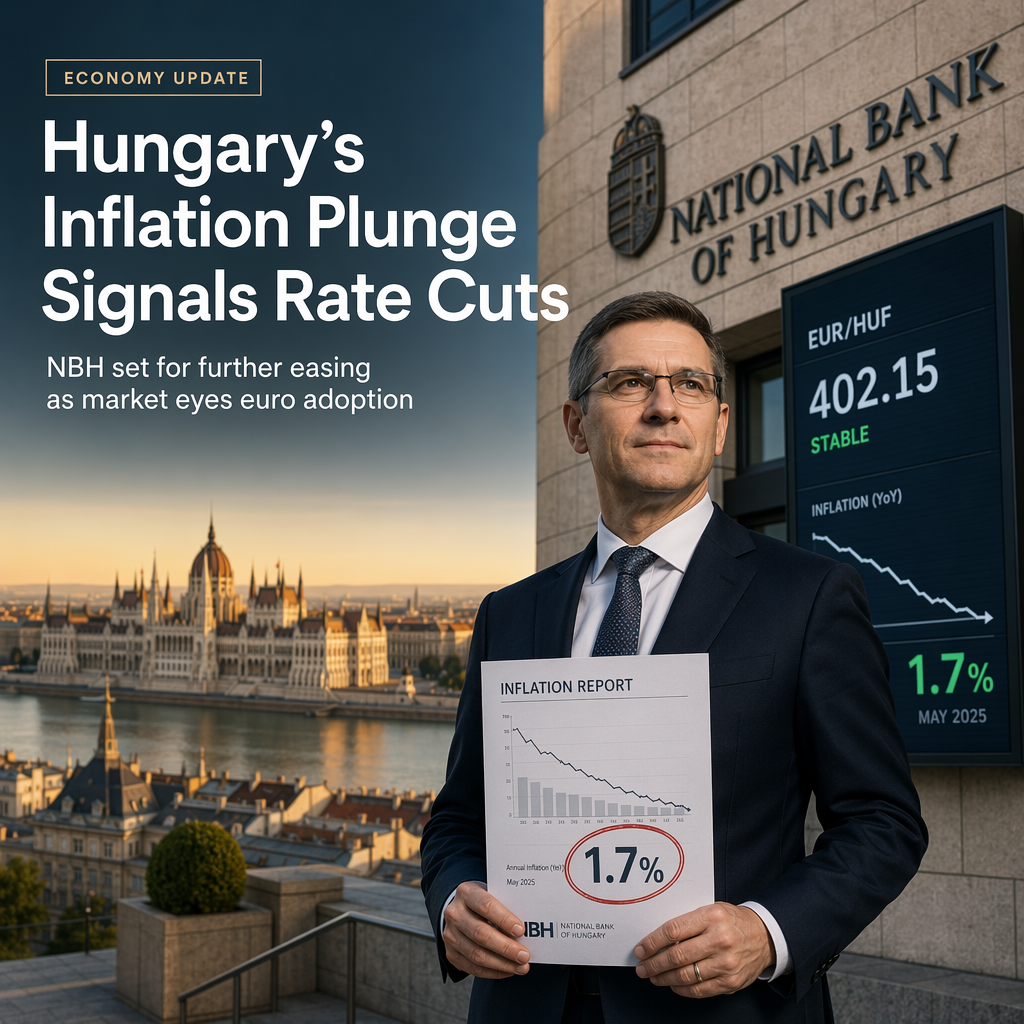

Hungarian inflation has declined further, reaching 1.7%, which is below both market expectations and the National Bank of Hungary's (NBH) June Inflation Report forecast of 2.0% [1]. This lower-than-expected inflation rate is seen as solidifying the likelihood of rate cuts by the NBH in July and August [1]. According to Frantisek Taborsky at ING, market pricing as of yesterday indicated expectations for around 150 basis points of easing and a terminal rate of 4.50%, aligning with ING's forecast, provided that BUBOR remains above the policy rate at the end of the cycle [1].

Taborsky notes that while the anticipated easing is significant in a global context, there remains potential for the market to price in at least one additional rate cut, given the more favorable conditions compared to two years ago [1]. The dovish inflation trajectory is expected to encourage further easing [1].

Despite the mechanical expectation that rate cuts would negatively impact the forint, ING believes that the rate differential currently has only a limited effect on the EUR/HUF exchange rate. Instead, the market is more focused on domestic political developments and the ongoing discussion around euro adoption [1]. In the short term, the forint may experience some pressure as further cuts are anticipated, but over the medium term, ING expects the EUR/HUF to remain stable within the 350–356 range [1]. Additionally, the forint could continue to benefit from summer carry demand [1].

CONCLUSION

Hungarian inflation's drop to 1.7% has reinforced expectations for further NBH rate cuts, with markets pricing in significant easing ahead. While this could put short-term pressure on the forint, ING expects medium-term stability for EUR/HUF and ongoing support from carry demand. The market's focus remains on domestic politics and euro adoption rather than rate differentials.