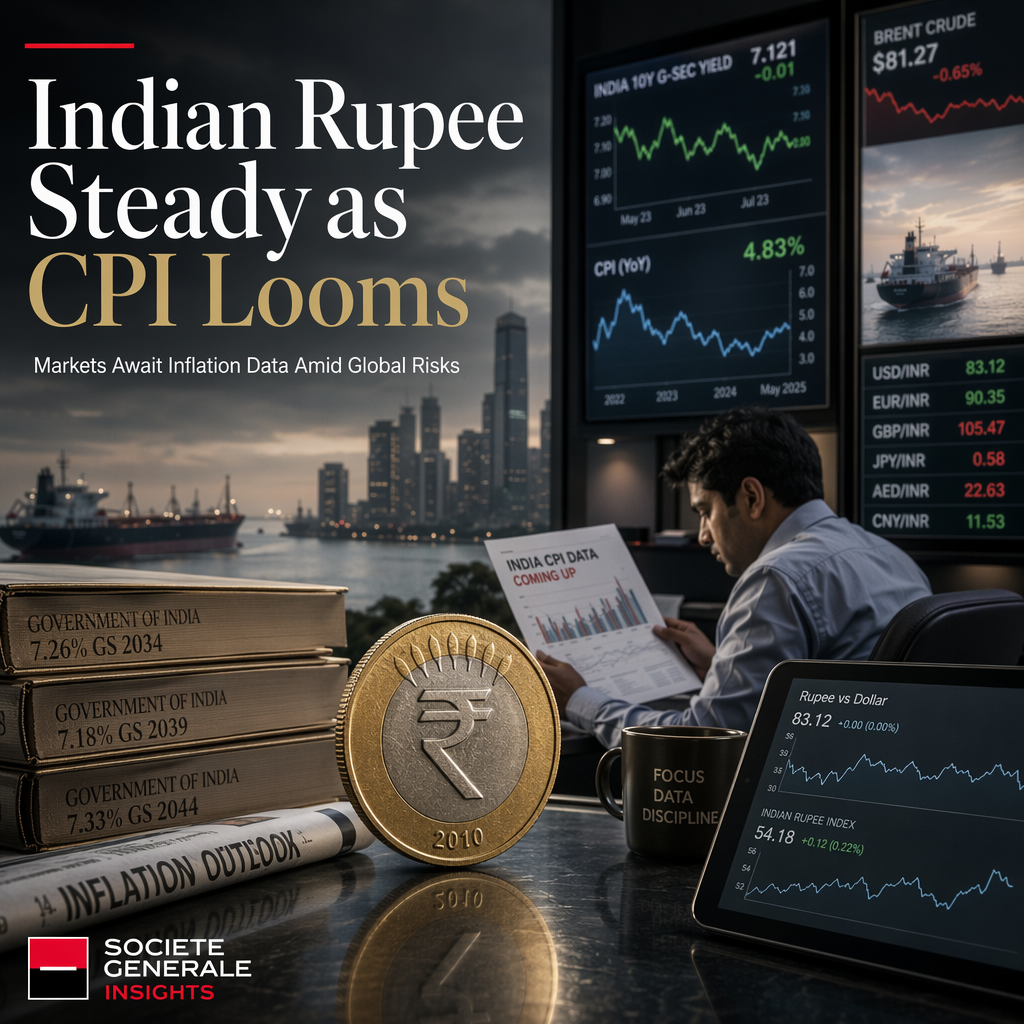

Societe Generale strategists emphasize that India's June Consumer Price Index (CPI) release is a significant event for bond markets, with the 10-year Indian Government Bond (IGB) yield currently anchored near its 200-day moving average at 6.71% [1]. Yields have retraced almost 43 basis points from their peak in May, indicating some stabilization in the bond market ahead of the inflation data [1].

Inflation is forecast to have edged up to 4.2% in June from 3.93% in May, reflecting a modest rise in price pressures [1]. The strategists note that robust Foreign Portfolio Investment (FPI) inflows have continued, supported by investment incentives announced by the Reserve Bank of India (RBI) and the Ministry of Finance in early June [1]. Additionally, the narrowing of India's trade deficit in June is seen as a supportive factor for the Indian Rupee (INR) [1].

Despite these positive factors, Societe Generale cautions that they do not guarantee a sustained move away from the 95.23 level on the 50-day moving average for the INR [1]. The report also highlights that developments in the Middle East and fluctuations in oil prices are expected to exert a greater influence on the INR in the near term [1].

Overall, while the INR is supported by strong FPI inflows and a narrower trade deficit, the currency remains range-bound, with market participants closely watching the upcoming CPI data and external geopolitical risks [1].

CONCLUSION

The Indian Rupee remains supported by robust FPI inflows and a narrowing trade deficit, but is constrained by external risks and awaits direction from the June CPI release. Market participants are expected to monitor inflation data and geopolitical developments closely for further cues.