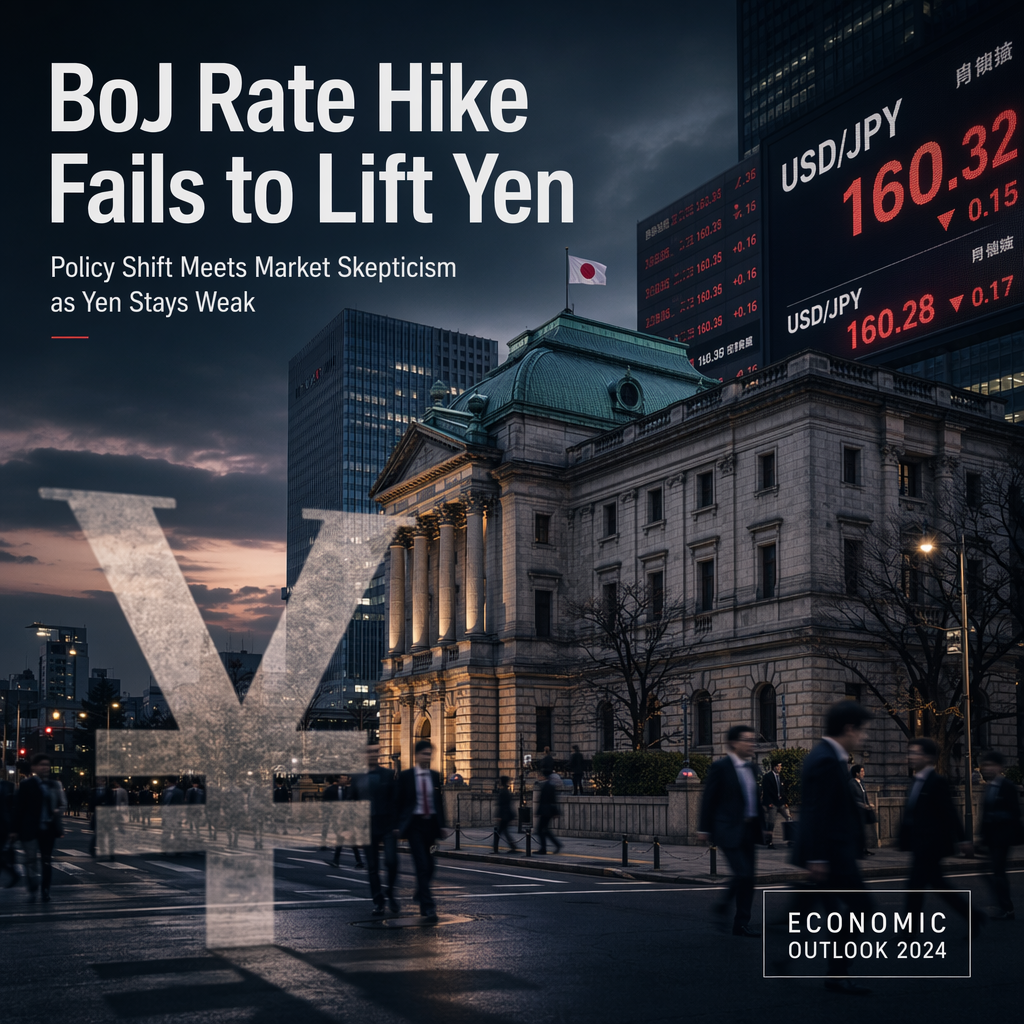

The Bank of Japan (BoJ) implemented a 25 basis point rate hike, raising its policy rate to 1.0%, a level not seen in 30 years, as noted by OCBC strategists Sim Moh Siong and Christopher Wong [1]. Despite this move, the Japanese Yen (JPY) has not experienced significant appreciation, with the USD/JPY exchange rate remaining above 160 [1]. The rate decision included one dovish dissent from Asada, a new appointee by Prime Minister Takaichi [1].

OCBC strategists highlight that, although the BoJ confirmed its plan to end tapering in 2027 and maintains a policy bias toward further hikes, there was no indication of an accelerated rate hike cycle [1]. Japan continues to have one of the lowest real rates among G10 economies, which undermines the Yen's attractiveness [1].

The impact of the Ministry of Finance's foreign exchange intervention in late April has been completely reversed, with the Yen weakening further since then [1]. OCBC analysts argue that the risk of further intervention is high, but without a more hawkish stance from the BoJ, any reversal in Yen weakness is unlikely to be sustained [1].

Overall, the market reaction suggests skepticism about the BoJ's willingness to tighten policy aggressively, and the Yen remains under pressure as a result [1].

CONCLUSION

The Bank of Japan's rate hike to 1.0% has not provided lasting support for the Japanese Yen, which remains weak against the US dollar. Analysts suggest that without a clearer hawkish shift from the BoJ, the Yen is likely to remain a funding currency and intervention risks will persist.