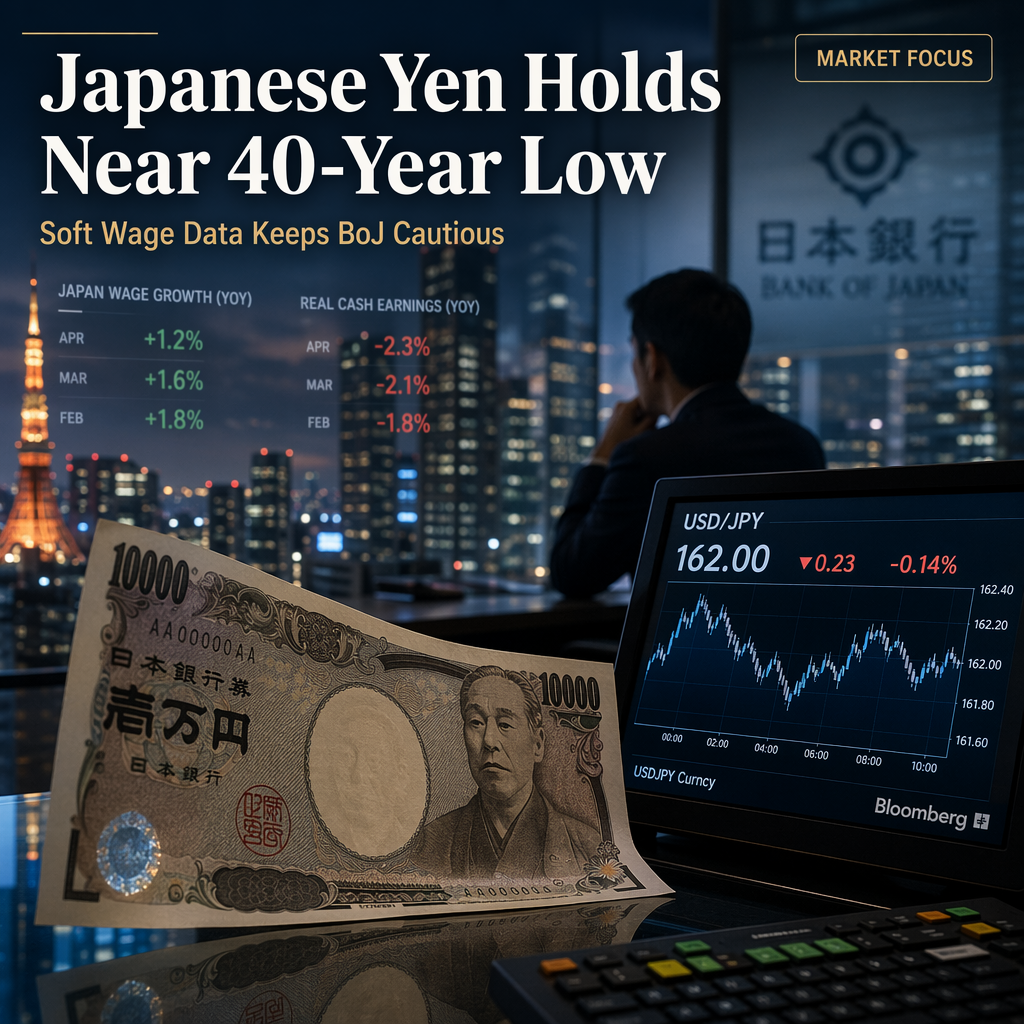

The Japanese Yen is consolidating around 162.00 against the US dollar after previously reaching a 40-year low near 162.84, according to Brown Brothers Harriman’s (BBH) Elias Haddad [1]. This movement follows the release of Japan’s May wage data, which showed a slowdown in total nominal wage growth to 3.2% year-over-year, below the consensus estimate of 3.4% and down from 3.6% in April. Scheduled pay growth for full-time workers also cooled to a five-month low of 2.4% year-over-year, compared to 2.5% in April [1].

The article notes that Japan’s wage growth is not a significant source of inflation pressure, given annual total factor productivity growth of about 1%. Furthermore, most of the Bank of Japan’s (BoJ) underlying Consumer Price Index (CPI) indicators eased further below the 2% target in May, suggesting limited inflationary momentum [1].

In the bond market, 30-year Japanese Government Bond (JGB) yields dropped as much as 10 basis points to 4.00% amid strong investor demand. The latest 30-year bond auction saw an average bid-to-cover ratio of 4.55, up from 2.94 in June and marking the highest level since May 2019 [1].

BBH’s Haddad concludes that the bar for a hawkish repricing by the BoJ remains high, which should cap any relief rallies in the Japanese Yen despite current market expectations. The swaps curve is pricing in nearly 50 basis points of rate hikes to 1.50% over the next twelve months, which is described as broadly appropriate given the current economic data [1].

CONCLUSION

The Japanese Yen remains under pressure as soft wage and inflation data reduce the likelihood of a hawkish shift by the Bank of Japan. Market expectations for rate hikes appear aligned with current fundamentals, suggesting limited upside for the Yen in the near term.