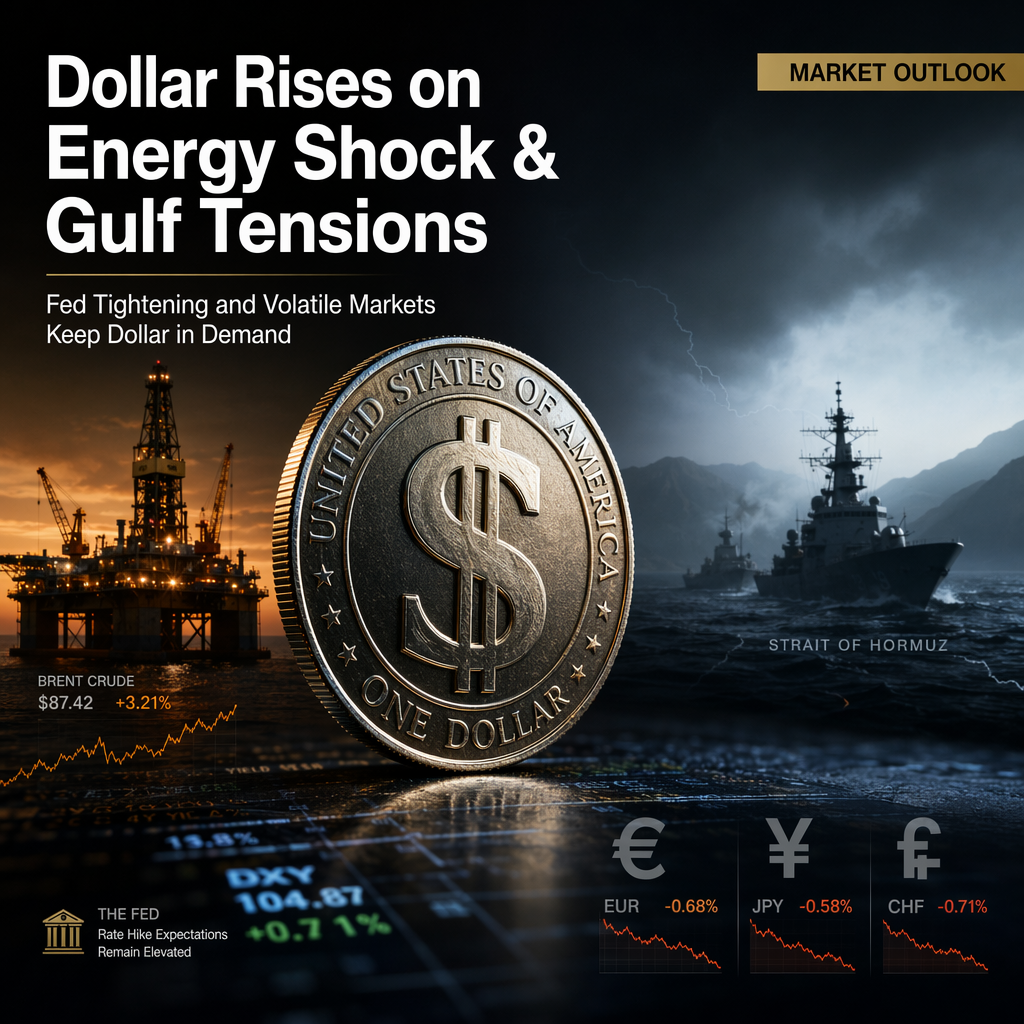

According to ING analysts Chris Turner, Frantisek Taborsky, and Francesco Pesole, higher energy prices and escalating tensions in the Gulf region are currently supporting the US Dollar against low-yielding currencies such as the Euro, Japanese Yen, and Swiss Franc [1]. The analysts highlight that US energy independence and the renewed prospects of Federal Reserve tightening are key factors underpinning the Dollar's strength [1].

ING expects the Dollar to remain in demand, particularly versus the Euro, Yen, and Swiss Franc, with the DXY index projected to grind higher [1]. The analysts note that if Iran is effective in re-closing the Strait of Hormuz, US energy independence will become even more significant, and US interest rates are likely to rise alongside overseas rates due to the live prospects of Fed tightening [1].

Looking ahead, the June Consumer Price Index (CPI) is set to be released, with headline inflation expected to drop month-on-month. However, with energy prices rising again and core inflation likely to increase at 2.8% to 2.9% year-on-year, ING believes it is too early for the market to price out a Fed rate hike this year [1]. The analysts suggest that the Dollar should maintain its gains, especially against low-yielding energy importers, and that the Swiss Franc may lag in a higher interest rate environment [1].

Specific targets mentioned include the possibility of USD/CHF retesting last month's high at 0.8140 and the DXY index grinding to 101.50 [1]. ING also points out that the deteriorating situation in the Gulf and rising energy prices are particularly concerning for Europe, as natural gas prices are increasing at a time of low inventories [1]. In the absence of clear direction from the Fed, higher energy prices are expected to keep tightening fears alive and the Dollar in demand [1].

CONCLUSION

ING analysts attribute the US Dollar's current strength to rising energy prices, Gulf tensions, and ongoing Fed tightening prospects. With inflation data pending and energy markets volatile, the Dollar is expected to remain favored against low-yielding currencies, while the Swiss Franc and Euro may underperform. Market participants are advised to monitor energy developments and upcoming inflation data for further direction.