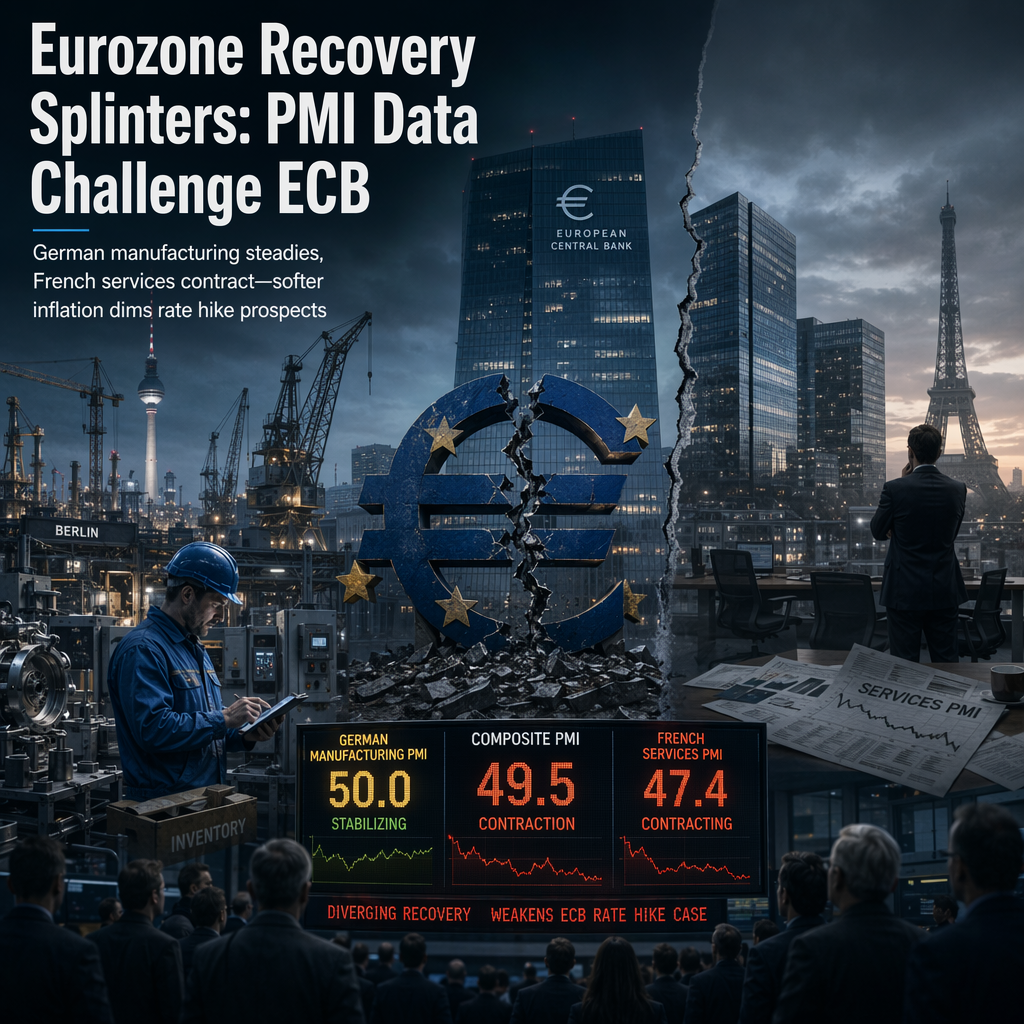

June Eurozone Purchasing Managers' Index (PMI) data indicate a two-speed recovery across the region, with German manufacturing stabilizing while French services continue to contract, according to TD Securities and BNY [1][2]. German manufacturing PMI held steady at 50.0 (TDS: 50.0; market: 50.2; prior: 50.1), signaling stabilization and improving sentiment, although employment remains cautious as firms await a more durable demand recovery [1][2]. Meanwhile, French services PMI was reported at 47.4 (TDS: 45.5; market: 46.0; prior: 44.3), reflecting ongoing contraction due to declining new orders and weak client appetite, forcing firms to rely on discounting despite cost pressures [1]. Employment in French services only stabilizes, and confidence is tentatively recovering, partly attributed to the resolution of Middle East conflicts [1].

BNY notes that the composite Eurozone PMI was slightly better than expected at 49.5 (consensus: 49.2), with manufacturing showing some expansion at 51.3 (consensus: 51.6) [2]. However, core economies like Germany and France continue to underperform, with German services falling to a 43-month low of 46.8 [2]. The weak performance in core sectors and reports of softer inflation pressures challenge the European Central Bank's (ECB) assessment of demand and raise questions about the necessity of further rate hikes, weighing on the Euro [2].

TD Securities emphasizes the divergence between manufacturing and services, noting that German manufacturing is supported by bottoming new orders, while French services remain demand-constrained and reliant on discounting to stimulate activity [1]. BNY adds that the softer inflation pressures observed in the PMI data further undermine the case for ECB tightening, suggesting that the figures will prompt reassessment of Eurozone demand conditions [2].

No specific forward-looking statements or analyst opinions regarding future ECB actions are provided, but both sources highlight the implications of weak PMIs and easing price pressures for monetary policy decisions [1][2].

CONCLUSION

Eurozone PMI data for June underscore a diverging recovery, with German manufacturing stabilizing and French services still contracting. Softer inflation pressures and weak core sector performance challenge the ECB's justification for further rate hikes, suggesting a cautious outlook for the Euro. The market impact is medium, as investors await clearer signals on demand and monetary policy direction.