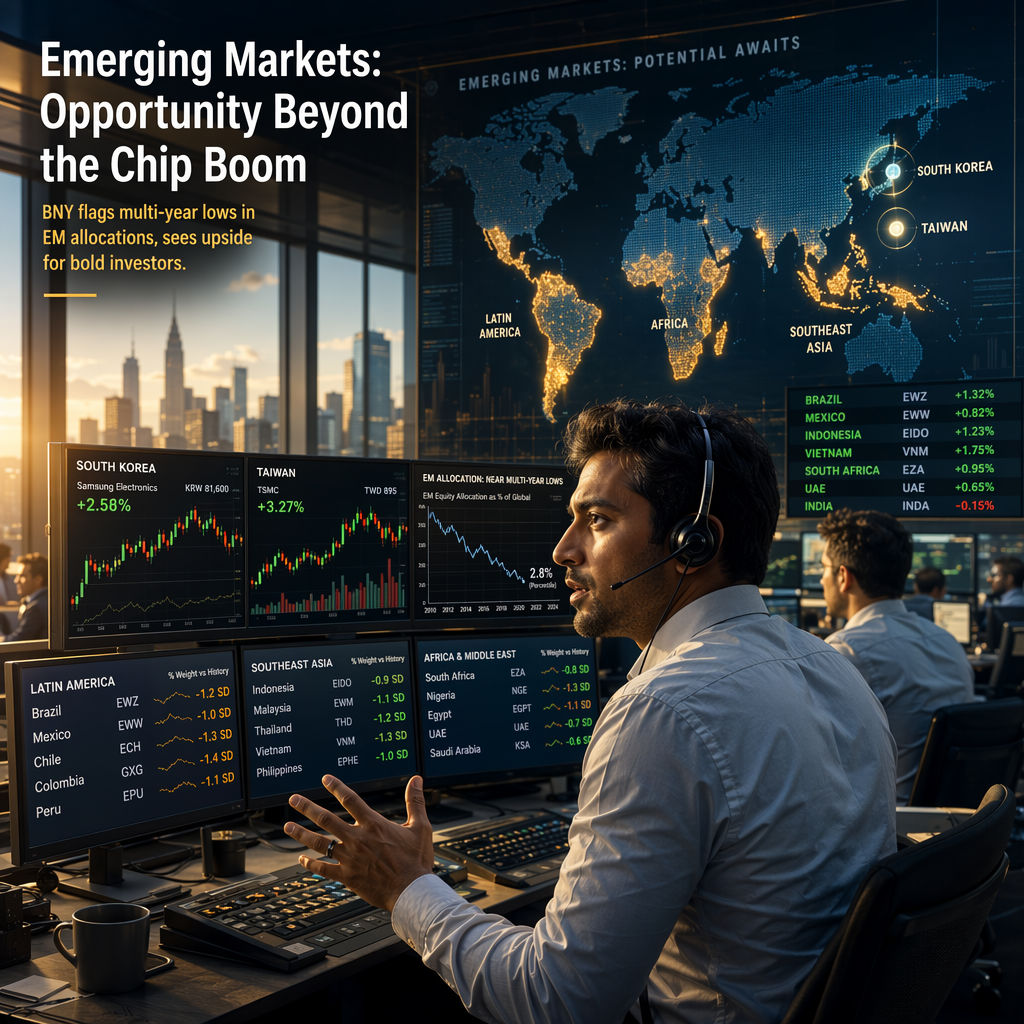

According to BNY’s Geoff Yu, current positioning in Emerging Markets (EM) equities is heavily concentrated in South Korea and Taiwan, particularly among semiconductor-related stocks, while the rest of the EM universe is experiencing historically low allocations [1]. Yu notes that excluding South Korea and Taiwan, the EM equity share of global positioning is just above 4%, marking the lowest level in three years and representing a decline of nearly 20% over that period [1].

Recent market action saw semiconductor stocks in South Korea fall significantly, with Taiwanese peers also struggling to capitalize on strong earnings reports [1]. This trend has led to a pronounced rotation away from EM chip leaders, which Yu identifies as an increasingly influential allocation theme [1].

Despite ongoing weakness in China and poor data across much of the EM space, Yu argues that current valuations already reflect expectations of strong disinflation, weak growth, and limited earnings momentum [1]. He suggests that adding EM exposure ahead of any potential recovery could offer a more attractive risk-reward profile than current market positioning implies, regardless of whether the catalyst is cyclical improvement or policy stimulus [1].

Yu concludes that market positioning currently assumes no earnings growth in EM outside of the semiconductor sector, a view he considers overly pessimistic if any recovery impetus emerges [1].

CONCLUSION

BNY’s analysis indicates that EM equity allocations are at multi-year lows outside of South Korea and Taiwan, with market sentiment reflecting pessimism about earnings growth. However, the report suggests that this positioning may present an attractive entry point if recovery catalysts materialize, offering potential upside for investors willing to add EM exposure.