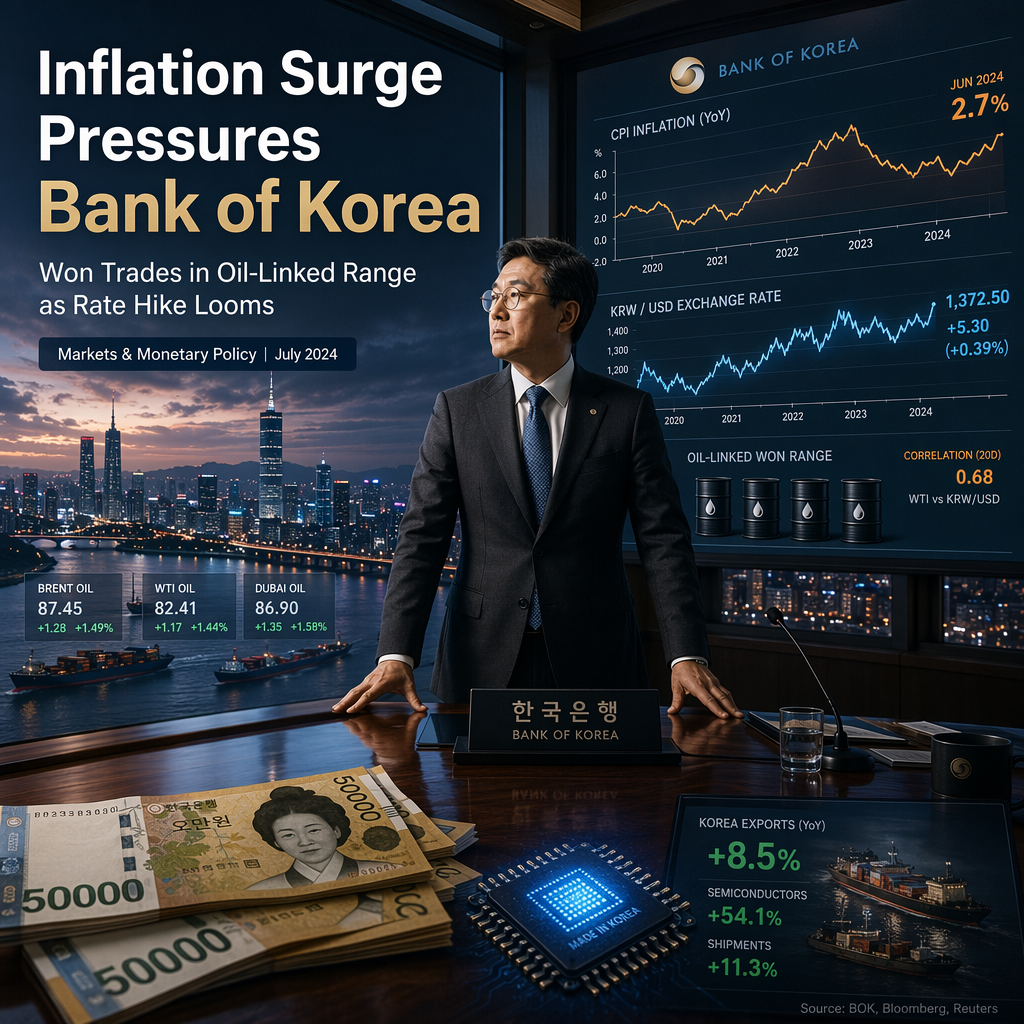

Commerzbank’s Charlie Lay highlights that South Korea's inflation remained elevated in June, with headline CPI inflation rising to 3.2% year-over-year from 3.1% in May, marking the highest level since December 2023 and staying well above the Bank of Korea’s (BoK) 2% target [1]. This persistent inflation, driven by factors such as a weak won and robust wage growth linked to the AI-driven semiconductor boom, strengthens the case for a 25 basis point BoK rate hike to 2.75% at the upcoming meeting on 16 July [1].

The South Korean won has been pressured by both inflation and oil prices. The USD/KRW exchange rate has declined from 1560 to 1506 over the past two weeks, largely due to a pullback in oil prices [1]. However, Commerzbank expects the pair to trade in a 1500–1520 range going forward, with oil prices and global risk sentiment remaining key drivers [1]. A rebound in oil prices could limit any further decline in USD/KRW in the near term [1].

Exports continue to surprise on the upside, supported by booming semiconductor demand, which is also contributing to inflationary pressures [1]. External factors such as the US dollar, global risk sentiment, and geopolitical developments are expected to remain significant influences on the won’s performance [1].

CONCLUSION

Persistent inflation and strong export performance are reinforcing expectations for a Bank of Korea rate hike at the next meeting. The won is likely to remain sensitive to oil prices and global risk sentiment, with the USD/KRW pair expected to trade in a defined range in the near term.