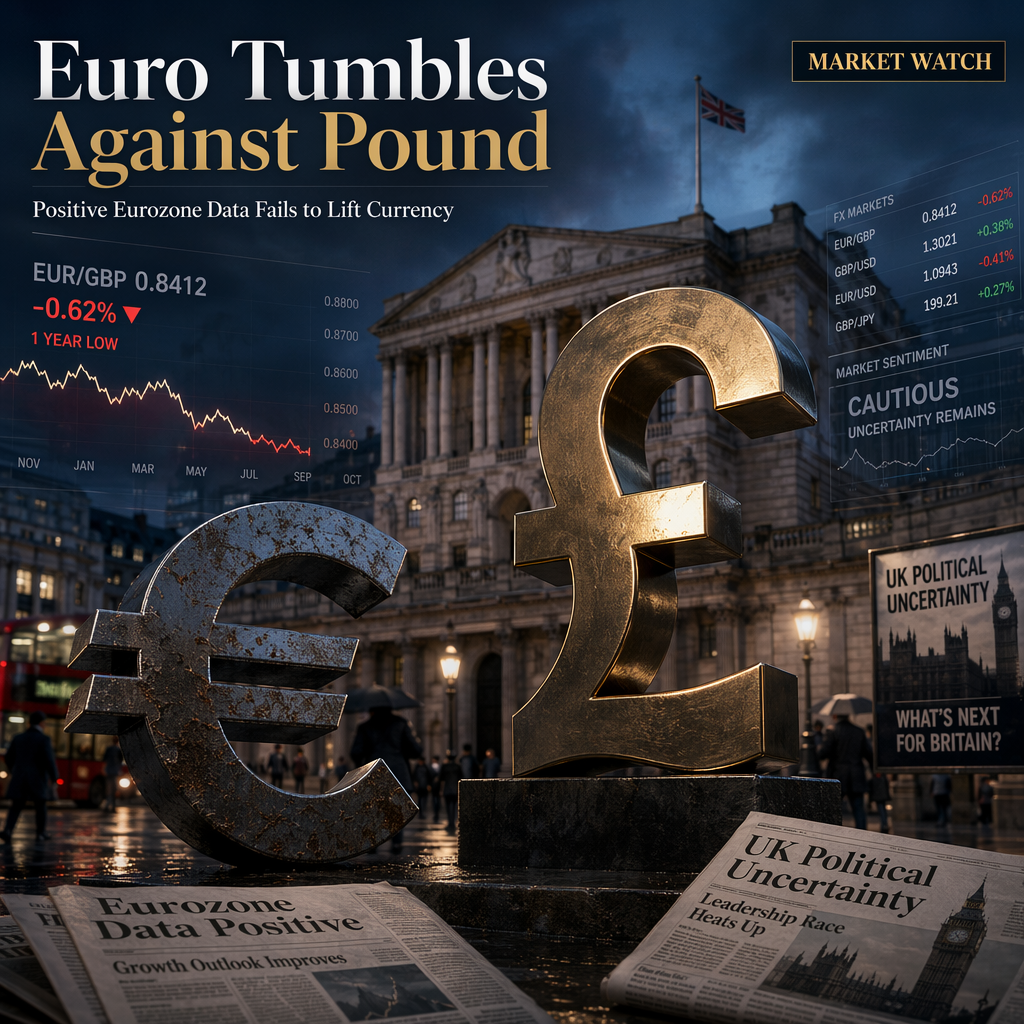

The Euro (EUR) continued to trade near one-year lows against the British Pound (GBP) on Monday, falling below 0.8560 after retreating from Friday’s highs at 0.8575. This decline occurred despite a series of positive economic data releases from the Eurozone, which failed to provide meaningful support for the currency [1].

Eurozone Retail Sales increased by 0.2% in May, slightly missing the 0.3% market consensus but improving from a 0.3% contraction in April. On a year-over-year basis, retail sales growth accelerated to 1.6%, in line with expectations and up from April’s 1% reading [1]. Additionally, German Factory Orders rose by 1.9% in May, surpassing the 1.2% consensus and partially reversing the 3.2% contraction seen in April. The Sentix Investors’ Confidence Index for July also improved significantly, rising to -3.1 from -13.4 in June, marking its best level in four months [1].

In contrast, the British Pound remained moderately bid, even as UK economic data showed weakness. The S&P Global Construction Purchasing Managers Index (PMI) for May improved slightly to 38.4 from 38.2 in the previous month, but remained well below the 40.0 expected by market consensus, indicating ongoing weakness in the sector [1].

Political uncertainty in the UK persists as the country prepares for its seventh prime minister in ten years. Andy Burnham, the Mayor of Manchester and the leading candidate to replace outgoing Prime Minister Keith Starmer, has pledged to respect fiscal rules, which has helped to stabilize the Pound and limit bearish sentiment for now [1].

CONCLUSION

Despite positive economic data from the Eurozone, the Euro remains under pressure against the Pound, which is holding steady amid weak UK construction data and ongoing political uncertainty. Market participants appear to be focusing more on relative political stability and fiscal commitments in the UK than on recent Eurozone economic improvements.