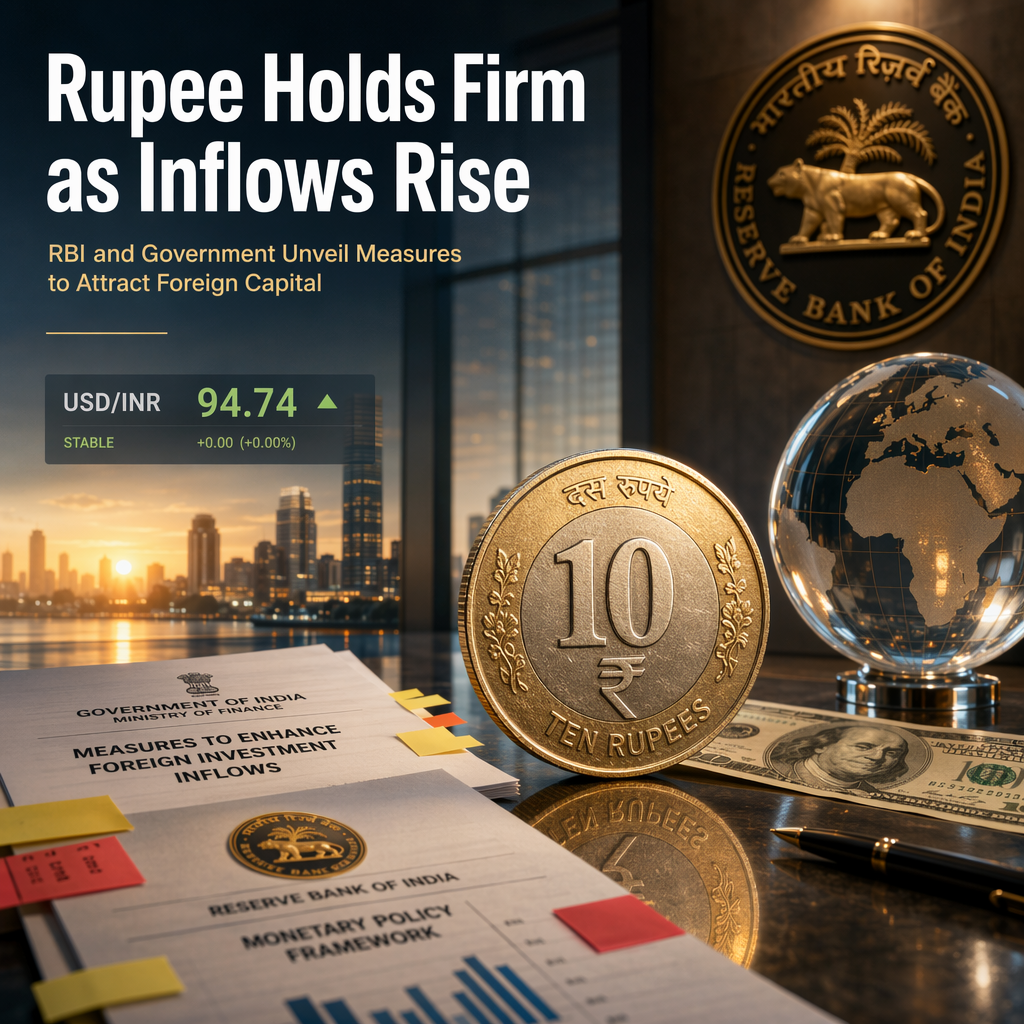

The Indian Rupee (INR) has shown stability against the US Dollar, with the USD/INR pair trading in a narrow range between 94.00 and 95.00 since mid-June, most recently quoted at approximately 94.74 [1]. This stabilization follows a coordinated package of measures announced by the Indian government and the Reserve Bank of India (RBI) aimed at attracting foreign capital inflows [1].

Key policy actions include the expansion of the Fully Accessible Route (FAR) to cover long-term government bond issuance, exemptions from capital gains and withholding taxes for foreign investors, a subsidised FX swap facility for external commercial borrowings, and full hedge support for FCNR(B) deposits [1]. The RBI has also clarified that FX hedges associated with FCNR(B) deposits will be exempt from the USD100 million net open INR position limit, and banks are now permitted to extend loans using these deposits, further enhancing their appeal [1]. Estimates suggest these initiatives could attract between USD30 billion and USD50 billion in foreign inflows [1].

On the macroeconomic front, the June flash PMI indicates a moderation in growth rather than a sharp downturn. Manufacturing continues to face weaker domestic and external demand and ongoing supply chain disruptions, while the services sector remains relatively resilient, supported by stronger international demand [1]. The easing of Middle East-related supply bottlenecks could support a rebound in activity in the coming months, contingent on the durability of the current ceasefire [1].

Market reaction has been muted, with USD/INR remaining little changed, reflecting investor confidence in the effectiveness of the announced measures to support INR stability [1].

CONCLUSION

The Indian Rupee's stability is being underpinned by a comprehensive set of government and RBI measures designed to attract substantial foreign inflows. While growth momentum has moderated, the policy package is expected to bolster capital inflows and support INR resilience in the near term.