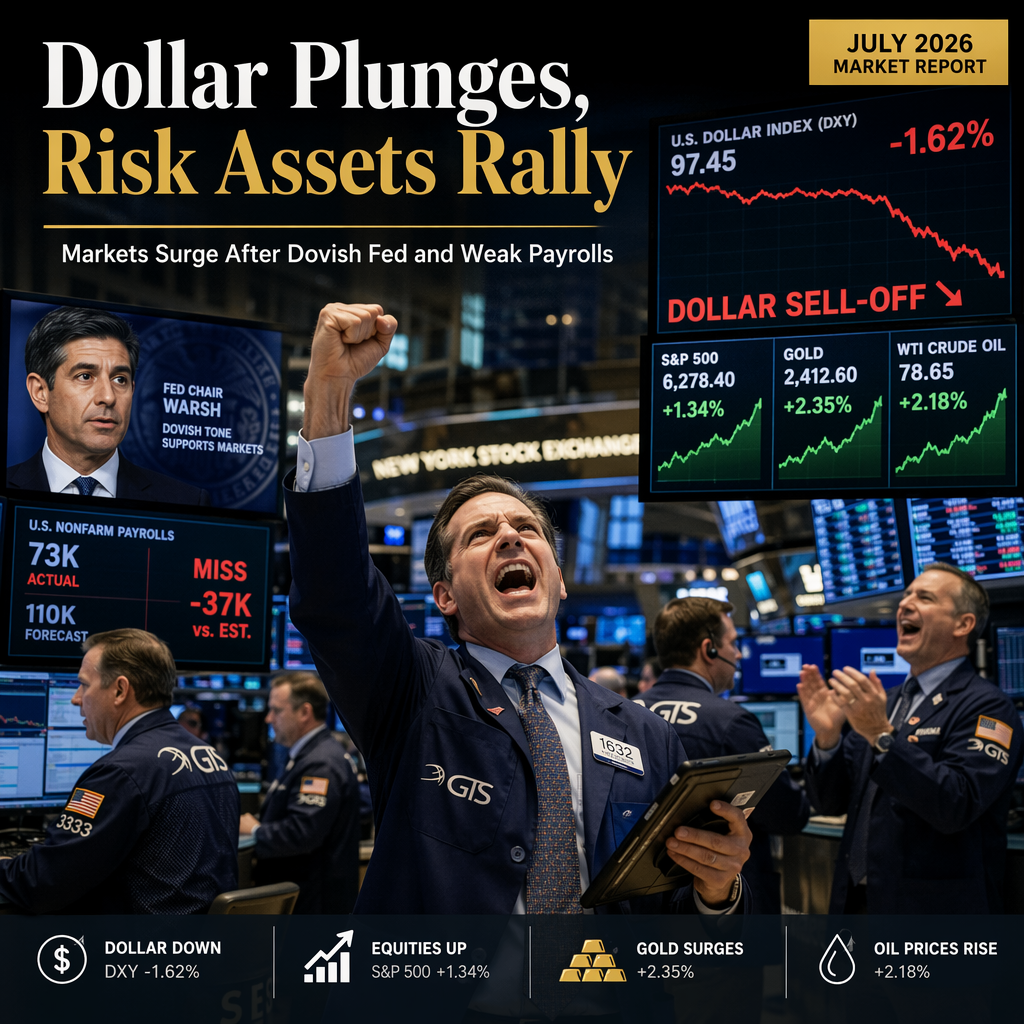

The week of June 29 to July 3, 2026, was marked by a significant market-moving event: the U.S. payrolls report released on Thursday, which showed a substantial miss in job creation. This disappointing data point led to a sharp and broad-based decline in the U.S. dollar against major currency pairs, as investors reacted to the weaker-than-expected labor market figures [1].

The risk-on sentiment in markets was set in motion a day earlier, when Federal Reserve Chair Warsh adopted a dovish tone during remarks on Wednesday. This unexpected shift in central bank communication primed markets for a rally in risk assets, which was then confirmed and accelerated by the poor payrolls data [1].

As a result, equities and high-beta assets experienced a strong recovery after several weeks of sideways movement, reflecting renewed risk appetite among investors. Commodities, including gold and oil, also benefited from the weaker dollar, posting gains as the currency depreciated [1]. Key technical levels were breached in major currency pairs such as EUR/USD, GBP/USD, and USD/JPY, underscoring the magnitude of the dollar's decline [1].

Looking ahead, the article advises that continued dollar weakness is likely if payroll trends remain soft and the Federal Reserve maintains its dovish stance. Risk assets could see further gains if upcoming economic data continues to disappoint relative to expectations. Traders are encouraged to monitor support and resistance levels and consider trailing stops to protect profits in the event of a market reversal [1].

CONCLUSION

A weaker-than-expected U.S. payrolls report, combined with dovish signals from Fed Chair Warsh, triggered a broad sell-off in the dollar and a rally in risk assets and commodities. The market's reaction underscores the importance of central bank communication and economic data in driving asset prices. Investors are now watching for further data to confirm or challenge the current risk-on trend.