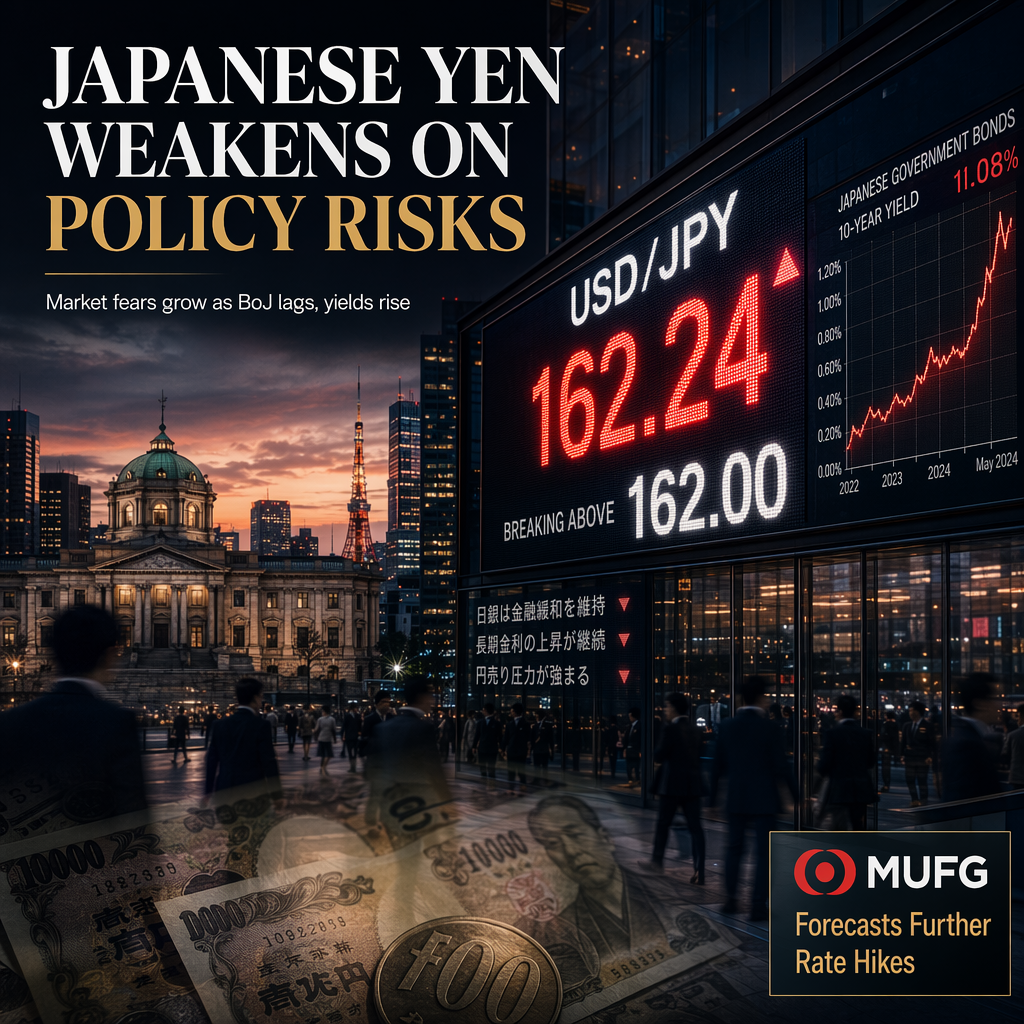

The Japanese Yen (JPY) has experienced renewed weakness, with USD/JPY rising back above 162.00 after reaching a low of 160.49 on Friday, according to MUFG’s Lee Hardman [1]. This move coincided with further selling at the long end of the Japanese Government Bond (JGB) curve, reflecting ongoing fiscal concerns and the perception that the Bank of Japan (BoJ) is lagging in tightening monetary policy [1].

There was speculation at the end of last week that Japanese authorities might intervene to support the yen during the US holiday when trading conditions were less liquid, but no intervention occurred, contributing to the yen giving back some of its recent gains [1]. The steepening of the Japanese yield curve contrasts with flatter curves in the US, UK, and Germany, highlighting renewed fiscal concerns in Japan and the view that the BoJ remains behind the curve [1].

MUFG expects inflation in Japan to accelerate through the second half of this year and into next year, maintaining pressure on the BoJ to further normalize monetary policy [1]. The bank believes the Japanese rate market is underpricing the potential for further BoJ tightening, especially as recent BoJ communications have flagged upside risks to inflation, including a faster pace of rising costs passing through to higher prices [1].

MUFG now projects the BoJ policy rate to reach 1.50% by January 2027, with the next rate hike anticipated in September. Currently, only around 6 basis points of hikes are priced in by September, suggesting room for short-term yields to move higher [1].

CONCLUSION

The Japanese yen's renewed weakness and rising JGB yields reflect market concerns about the BoJ's pace of policy normalization and Japan's fiscal outlook. MUFG anticipates further rate hikes, with the next move expected in September, and sees inflationary pressures persisting into next year. Market pricing may be underestimating the extent of BoJ tightening ahead.